The Summer Playground Trap: How Undeclared Trampolines Void Insurance

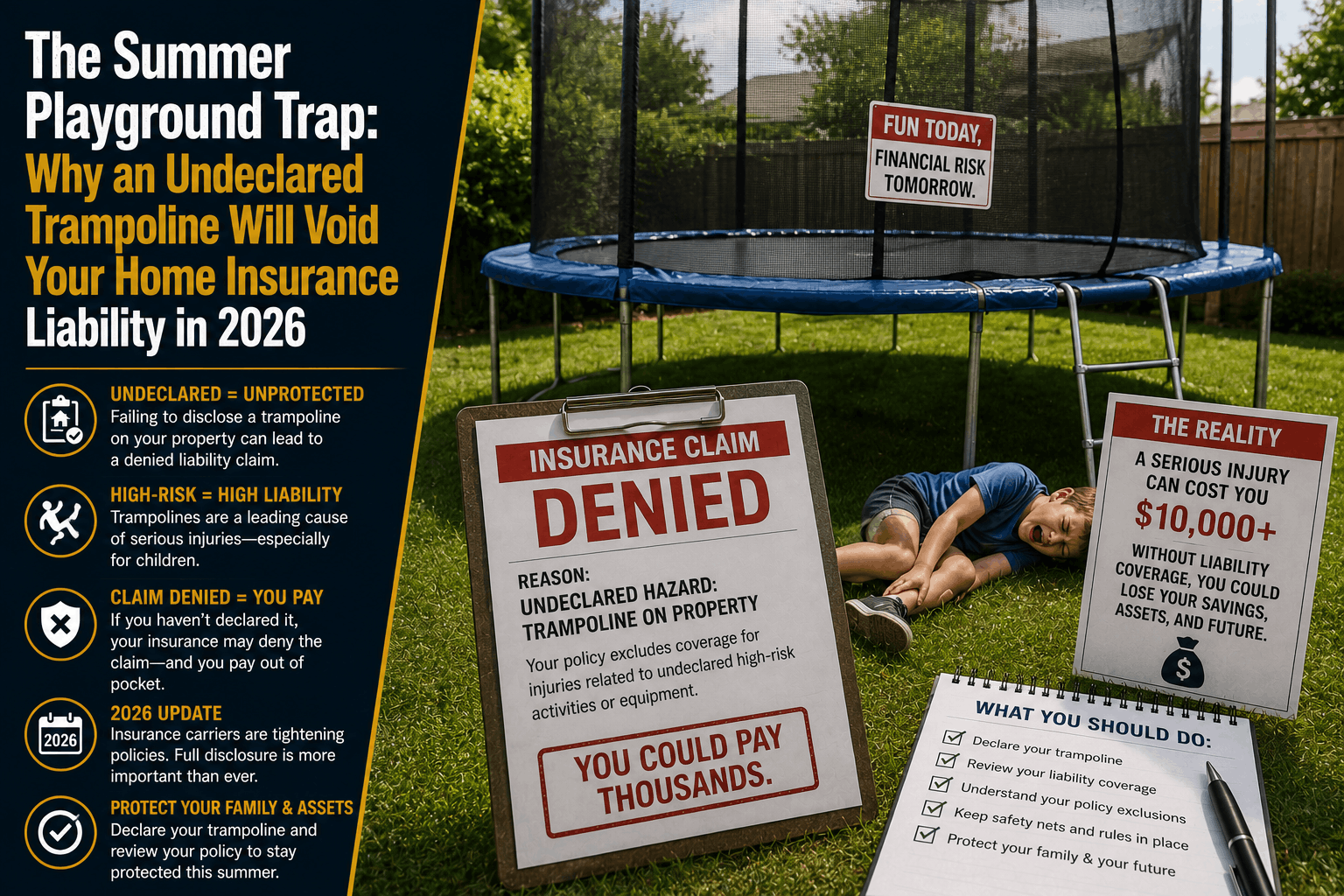

The Summer Playground Trap: Why an Undeclared Trampoline Will Void Your Home Insurance Liability in 2026

The Direct Answer: Buying and setting up a backyard trampoline without explicitly notifying your homeowners insurance carrier is a massive risk. In the insurance industry, trampolines are classified under the legal doctrine of an "Attractive Nuisance"—a dangerous piece of property that naturally entices children who may not understand the risk of injury.

In 2026, as carriers struggle with high injury-litigation costs and tighten contract guidelines, failing to declare a trampoline gives your insurer immediate legal grounds to completely deny a third-party liability claim or even cancel your policy altogether for "material change in risk."

If a neighbor's child or a guest breaks a bone or suffers a severe neck injury on an unlisted trampoline, your standard personal liability coverage will not step in to protect you. You will be left completely on your own to cover multi-thousand-dollar medical collections and private personal injury lawsuits.

1. The Underwriting Reality: The 3 Insurance Tiers

Insurance underwriters view trampolines with extreme hesitation due to the sheer volume of emergency room fractures, sprains, and concussions they cause every summer. Across the 2026 property market, carriers split trampoline ownership into three highly strict underwriting brackets:

- Tier 1: Absolute Exclusion (The Blacklist): Carriers like Allstate, Progressive, and several Florida domestic providers maintain a zero-tolerance policy. If their automated aerial drones spot a trampoline on your property, or if a claims adjuster discovers one after an unrelated windstorm, the carrier will refuse to cover any injury related to it and will often issue an immediate notice of policy non-renewal.

- Tier 2: Conditional Coverage (Safety Mandates): Many preferred insurers will agree to cover the risk, but only if you strictly implement structural safety measures. This contractually requires a fully enclosed safety net and a locked, 4-to-6-foot perimeter fence around your yard to keep uninvited children from accessing it.

- Tier 3: The Mandatory Endorsement / Rider: Some carriers require you to purchase a distinct, standalone Trampoline Liability Rider that explicitly adds the exposure back into your policy framework in exchange for a minor premium surcharge.

2. The Legal Mechanics of an "Attractive Nuisance" Denied Claim

The biggest trap for property owners is misunderstanding how civil liability operates when a neighborhood child enters your property without permission.

[Uninvited Child Trespasses] ──> [Enters Open Backyard] ──> [Injured on Trampoline]

===================================================================================

= Under "Attractive Nuisance" Laws, YOU Are Strictly Liable For Medical Damages.

The Trespassing Myth: Under standard tort law, you generally do not owe a high duty of care to adult trespassers. However, the Attractive Nuisance Doctrine completely flips this rule for minors. Because a child is legally deemed incapable of fully understanding the physical danger of a trampoline, you bear absolute responsibility to lock it away. If your yard is unfenced and an uninvited child climbs onto your trampoline and gets hurt, you are fully liable for their medical bills.

3. The Modern Tech Sweep: How Carriers Find Out

Assuming your insurance company will never notice a trampoline hidden in your backyard is an expensive operational gamble. In 2026, claims underwriting has shifted away from manual, multi-year property inspections and relies heavily on automated data aggregation:

- High-Resolution Satellite and Drone Auditing: Carriers utilize routine, AI-driven geographic mapping sweeps. Computer vision models automatically cross-reference your satellite property images against your policy details, flagging undeclared trampolines, pools, and roof decay instantly.

- The Cross-Claim Trigger: If a severe summer windstorm launches your trampoline into your neighbor’s fence or your own home’s vinyl siding, you might file a standard property structural claim. The moment the field adjuster steps into your yard to photograph the roof damage, they will document the twisted metal framing of the undeclared trampoline, triggering an immediate administrative policy review.

How to Safely Build a Backyard Safety Shield

If you want to preserve your family's summer fun without putting your entire life savings and home equity at risk, you must transition your property out of the undeclared trap using a precise, three-tier framework:

**1.Contact Your Independent Agent First:**Action: Consult Before Buying.

Before purchasing a trampoline, call your agent to verify if your current home insurance carrier completely blacklists the item. If they do, your agent can prepare to transition your profile to a more flexible carrier before the box arrives at your house.

**2.Install the Safety Framework:**Action: Physical Compliance.

Purchase a model equipped with integrated structural safety netting. Ensure your backyard features a minimum 4-to-6-foot fence with a self-closing, securely locking latch to legally defend against attractive nuisance claims.

**3.Secure a Written Policy Endorsement:**Action: Policy Execution.

Formally add the trampoline to your policy file. Ensure you receive an updated declarations page that does not feature an active Animal or Recreational Equipment Liability Exclusion.

Why Working with an Independent Agency is Vital

Attempting to manage your primary property asset through a generic smartphone application or automated online form means your contract will lack the specific disclosures needed to survive a catastrophic medical lawsuit. At Walker Insurance Agency, we provide the data-driven visibility you need to protect your family and your property lines.

The Walker Advantage:

- Carrier Restriction Matching: We cross-reference your yard assets against the guidelines of Florida's 20 brand-new private property companies, ensuring you land with a stable carrier that permits backyard play structures.

- Umbrella Safety Layering: We design Personal Umbrella Policies (PUP) that sit seamlessly on top of your primary home and auto lines, expanding your liability shield to $1 million or more to defend against catastrophic, life-altering childhood injury lawsuits.

- Comprehensive Risk Auditing: We audit your entire residential footprint in Stuart, linking wind-mitigation credits and liability riders together to keep your absolute out-of-pocket overhead as low as possible.

FAQ

1. Does my homeowners insurance cover injuries if my own children are hurt on the trampoline?

No. Your homeowners personal liability section (Coverage E) and medical payments section (Coverage F) are strictly designed to pay for third-party guests and visitors. If your own children are injured on your property, their recovery costs are handled strictly through your family’s private Health Insurance Policy, minus your standard health deductibles and copays.

2. Can an insurance company cancel my policy mid-term if they discover a trampoline?

Yes. If a carrier’s underwriting guidelines strictly prohibit trampolines, discovering one constitutes a "material change in risk" that was not disclosed when the policy was written. The carrier is legally permitted to issue a 30-to-45-day notice of cancellation, forcing you to secure alternative coverage immediately.

3. Does putting a safety net on the trampoline eliminate the need to notify my insurer?

Absolutely not. While a safety net satisfies the safety requirements of a conditional carrier, it does not override your contractual obligation to disclose a high-risk liability exposure. The presence of a net is irrelevant if the baseline carrier has a blanket trampoline exclusion written into your policy jacket.

Protect Your Wealth Before the Kids Start Jumping

A backyard trampoline provides endless summer entertainment, but leaving it hidden from your insurance underwriter is an administrative gamble that can destroy your household budget in a single afternoon. Real peace of mind requires aligning your insurance contract with the physical reality of your yard under blue skies.

Lock in your liability protection today. Contact Walker Insurance Agency for a comprehensive 2026 Property Risk Review. We provide the visibility you need to eliminate hidden liability loopholes, deploy high-limit umbrella shields, and protect your hard-earned wealth safely in Stuart.

[GET A FREE QUOTE TODAY]

Call us at +1-407-977-7100 or visit our office at 789 SW Federal Highway, Suite 201, Stuart, FL 34994. Let us safeguard your home and assets today.

Related Articles

Does Homeowners Insurance Cover Trampoline Injuries? (2026 Rules)

Putting up a backyard trampoline? Discover how 2026 home insurance policies handle trampoline injuries and why the attractive nuisance rule can trigger a denial.

Read More →

Does Homeowners Insurance Cover Mold & Slow Wall Leaks? (2026 Rules)

Think a hidden pipe drip is covered by insurance? Discover how Florida’s strict 14-day constant seepage rule and mold caps apply to slow leaks inside walls.

Read More →

Does Home Insurance Cover a Collapsed Water Line in the Yard? (2026 Rules)

Find out if standard home insurance covers a water line collapse under your yard. Learn about the strict "slab-up" rule and the crucial Service Line Endorsement.

Read More →