Does Homeowners Insurance Cover Trampoline Injuries? (2026 Rules)

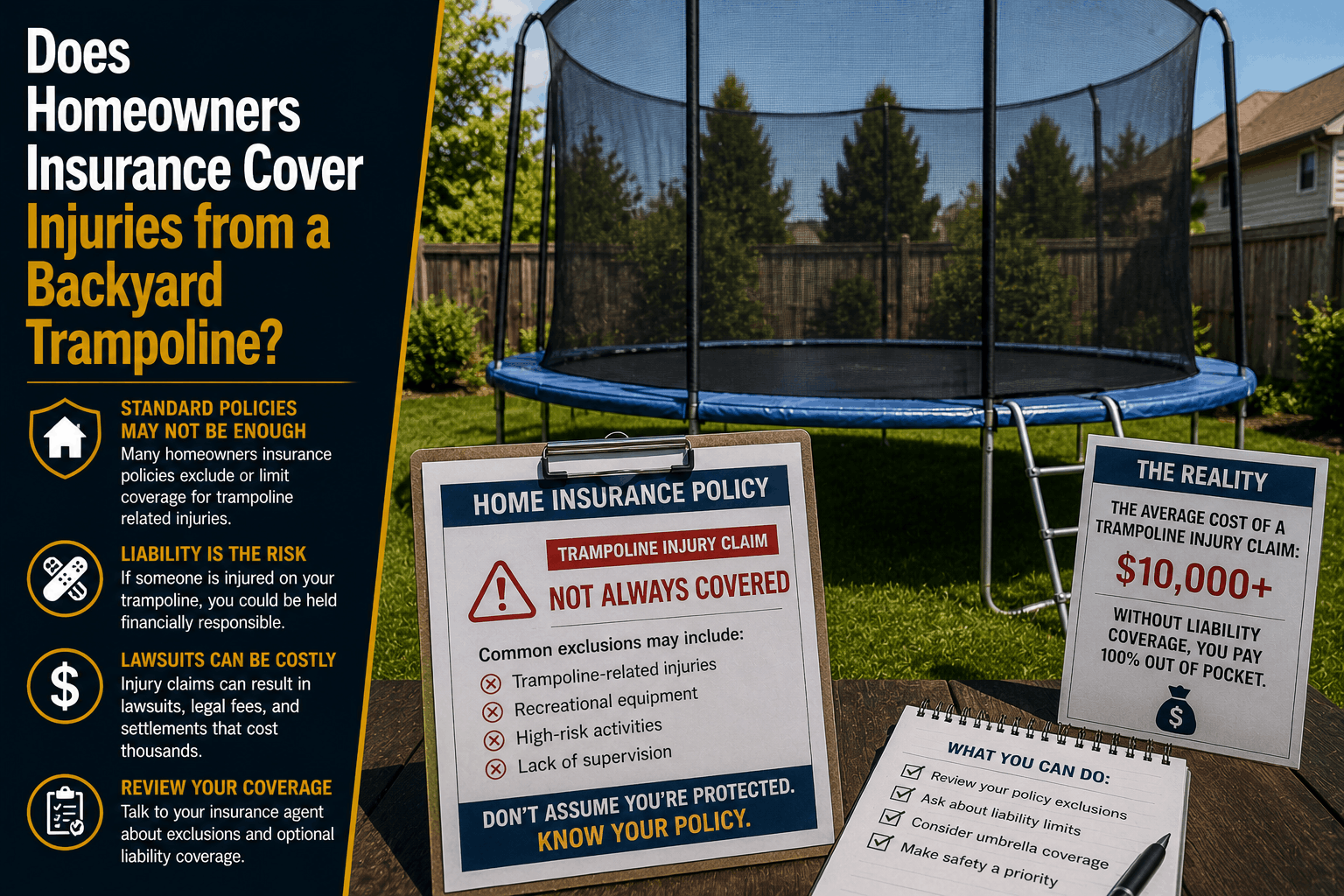

Does Homeowners Insurance Cover Injuries from a Backyard Trampoline?

The Direct Answer: Legally, standard homeowners insurance can cover third-party injuries caused by a backyard trampoline under your policy's Personal Liability (Coverage E) or Medical Payments (Coverage F) sections—but only if your specific insurance carrier allows trampolines and you have explicitly declared it on your policy.

In 2026, the insurance market has become incredibly restrictive regarding recreational backyard equipment. Due to high injury litigation costs, the insurance industry treats trampolines under a strict legal principle known as an "Attractive Nuisance" (a dangerous object that naturally entices curious children who are too young to understand the risk).

ARTA

Because of this high-risk classification, many top-tier insurance carriers now write absolute Trampoline Exclusion Endorsements into their standard contracts. If your policy features this exclusion, or if you failed to notify your carrier that you bought a trampoline, 100% of any resulting medical bills or personal injury lawsuits will be completely denied, leaving your personal savings and home equity completely exposed.

1. The 3 Ways Carriers Handle Trampolines

You cannot assume your home insurance automatically blankets your backyard setup. In the current property market, insurance companies manage the financial liability of a trampoline in one of three ways:

Kin Insurance+ 1

- 1. Absolute Exclusion (The Blacklist): Popular carriers like Lemonade, Allstate, and Progressive often apply standard exclusions to high-risk items like trampolines, bounce houses, and pool slides. If a neighbor’s child breaks a bone on the apparatus, the carrier will refuse to pay the claim. Furthermore, if an underwriter discovers an unlisted trampoline via routine satellite or aerial drone imagery sweeps, they may immediately cancel or non-renew your entire homeowners policy.

Lemonade Insurance - 2. Conditional Coverage (Safety Restrictions): Some carriers will agree to protect the exposure, but only if you strictly implement structural safety measures. This contractually requires the trampoline to feature an integrated safety net enclosure and your backyard to be fully enclosed by a locked, 4-to-6-foot perimeter fence.

Kin Insurance - 3. Standard Coverage with Surcharge: A few flexible carriers allow trampolines without restrictive endorsements, but they require you to formally log the item as a scheduled hazard and pay a minor premium surcharge on your annual bill.

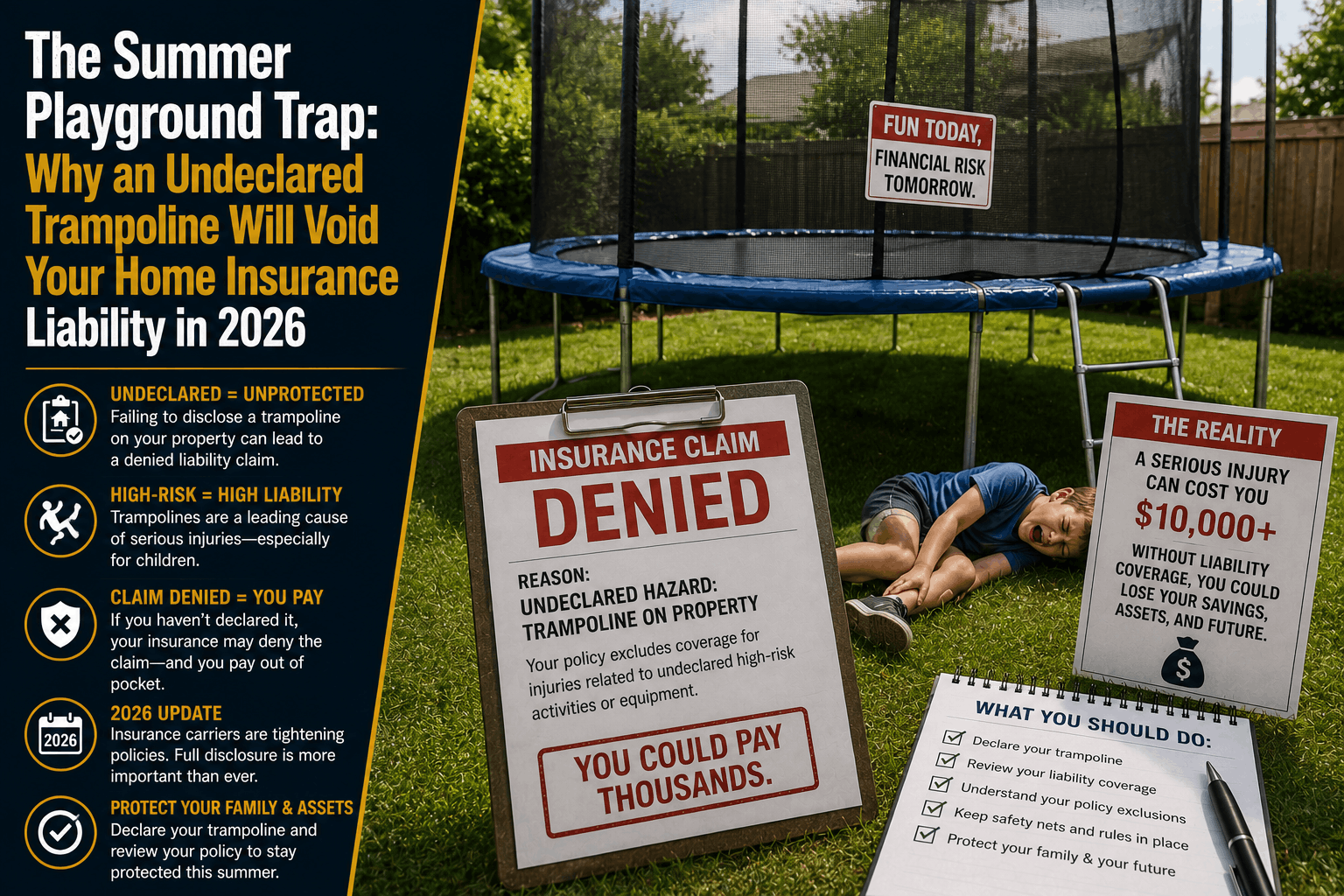

2. The Trap: The Attractive Nuisance Doctrine

The most dangerous mistake a property owner can make is assuming they aren't liable if a child uses their trampoline without explicit permission.

Allstate

[Uninvited Minor Trespasses] ──> [Enters Open Backyard] ──> [Injured on Trampoline]

===================================================================================

= Under "Attractive Nuisance" Laws, YOU Are Legally Liable For Their Medical Bills.

The Trespassing Exception: Under standard premises liability law, you owe a very low duty of care to adult trespassers. However, the Attractive Nuisance Doctrine completely removes this defense when minors are involved. Because young children lack the cognitive ability to accurately calculate physical risk, the law shifts the entire burden of safety to the homeowner. If your yard is unfenced and an uninvited neighborhood child wanders onto your property and gets hurt on your trampoline, you can be held entirely liable for their damages.

Ilabaca Law+ 1

3. Third-Party Payouts vs. Household Injuries

If your policy does fully cover your trampoline and a medical event occurs, the claim is processed across two distinct financial lines depending entirely on who was hurt:

| Who Was Injured? | Applicable Insurance Line | How It Settles the Claim |

|---|---|---|

| A Guest, Neighbor, or Visitor | Personal Liability (Coverage E) | Handles third-party surgical bills, rehabilitation, legal defense fees, and court judgments up to your policy limit (typically $100,000 to $300,000). |

| A Guest (Minor Injury) | Medical Payments (Coverage F) | Pays out smaller, immediate hospital bills (stitches, X-rays) up to a small cap ($1,000 to $5,000) regardless of who was at fault. |

| You, Your Spouse, or Your Kids | EXCLUDED (No Coverage Available) | Home insurance never covers bodily injury to residents of the household. Your family must rely entirely on your private health insurance policy. |

How to Safely Build a Backyard Protection Shield

If you want to protect your children's summer fun without putting your family's financial future at risk, you must transition your property out of the undeclared liability trap using a precise framework:

- Step 1: Execute an Agency Audit Before You Buy: Before purchasing a trampoline, call your independent agent to verify your carrier’s exact underwriting guidelines. If your current provider maintains a strict trampoline blacklist, your agent can begin shopping your profile to a more flexible market before the box ever lands on your doorstep.

- Step 2: Strict Physical Loss Control: Install a high-quality trampoline system featuring a heavy-duty safety enclosure network and durable spring padding. Ensure your backyard is completely enclosed by a sturdy fence equipped with a self-closing, self-latching gate to prevent unsupervised public access.

Bluefield Realty Group - Step 3: Stacking an Umbrella Defense Layer: Because severe trampoline accidents can result in complex fractures or spinal trauma, medical bills can easily blow right past a standard $300,000 home liability cap. Securing a standalone Personal Umbrella Policy (PUP) adds an extra $1 million to $5 million of clean liability protection on top of your primary home and auto lines, completely insulating your wealth from catastrophic civil judgments.

Why Working with an Independent Agency is Vital

Attempting to manage your primary property assets through a generic smartphone application means your contract will lack the specific disclosures and safety riders required to survive a major injury lawsuit. At Walker Insurance Agency, we provide the personalized, data-driven visibility you need to defend your home and lifestyle.

The Walker Advantage:

- Carrier Restriction Matching: We cross-reference your yard assets against the guidelines of Florida's brand-new private property insurance companies, ensuring you land with a stable provider that permits backyard play structures.

- Rider and Endorsement Verification: We audit your policy jacket line-by-line to unearth and eliminate hidden recreational equipment exclusions before a claim ever occurs.

- Unified Multi-Line Structuring: We seamlessly blend your home liability, wind-mitigation credits, and umbrella policies together, keeping your absolute out-of-pocket overhead optimized in Stuart.

FAQ

1. Can my insurance company cancel my policy mid-term if they find out I have a trampoline? Yes. If your insurance company has an absolute corporate ban on trampolines, setting one up constitutes a "material change in risk" that alters the nature of the original insurance contract. If they discover it via property inspections or satellite sweeps, they are legally permitted to issue a 30-to-45-day notice of policy cancellation, forcing you to replace your coverage immediately.

2. Does a trampoline safety net remove the need to notify my insurance carrier? Absolutely not. While a safety net is an essential risk-mitigation tool that satisfies conditional insurance guidelines, it does not override your contractual obligation to declare a high-risk liability exposure. If your carrier has a blanket trampoline exclusion written into their policy fine print, the presence of a net is entirely irrelevant.

Homeowners Insurance Authority

3. What should I do immediately if a guest is injured on my trampoline? First, ensure the injured person receives immediate professional medical attention. Once the health emergency is stabilized, take high-resolution photographs of the trampoline, the safety net, and the surrounding yard fencing to document your active safety measures. Document witness statements and contact your independent agent immediately to report the occurrence before a formal lawsuit is filed.

Bluefield Realty Group

Align Your Protection with Reality Before the Kids Start Jumping

A backyard trampoline can provide years of childhood memories, but keeping it hidden from your insurance underwriter is a gamble that can destroy your household budget in a single afternoon. Real peace of mind requires aligning your written insurance contract with the physical assets in your yard under blue skies.

Lock in your family liability protection today. Contact Walker Insurance Agency for a comprehensive 2026 property risk assessment. We provide the visibility you need to erase hidden liability loopholes, deploy high-limit umbrella shields, and protect your hard-earned wealth safely in Stuart.

[GET A FREE QUOTE TODAY]

Call us at +1-407-977-7100 or visit our office at 789 SW Federal Highway, Suite 201, Stuart, FL 34994. Let us safeguard your home and assets today.

Related Articles

The Summer Playground Trap: How Undeclared Trampolines Void Insurance

Putting up a backyard trampoline this summer? Learn why failing to declare it to your homeowners insurance can lead to total liability claims denial in 2026.

Read More →

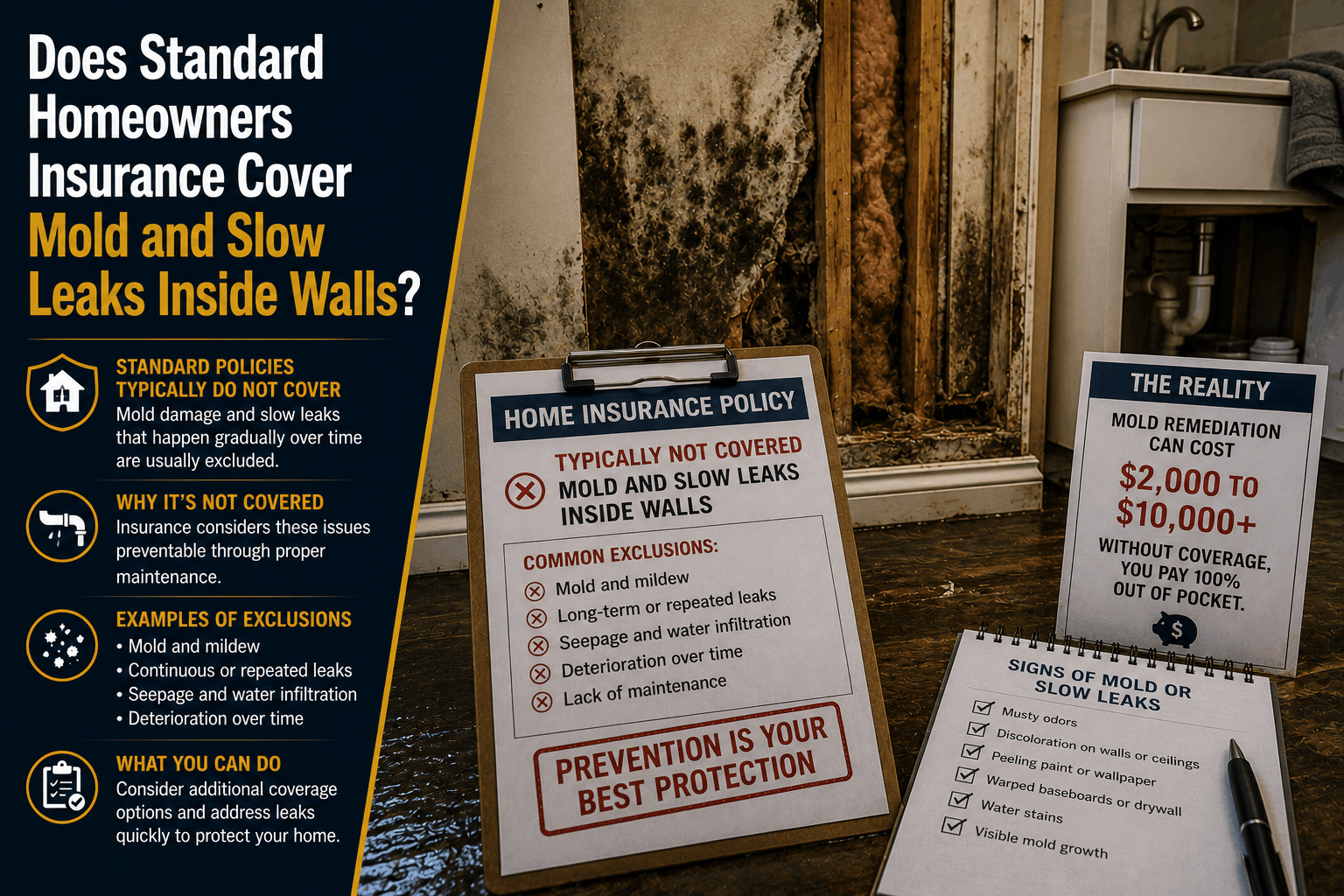

Does Homeowners Insurance Cover Mold & Slow Wall Leaks? (2026 Rules)

Think a hidden pipe drip is covered by insurance? Discover how Florida’s strict 14-day constant seepage rule and mold caps apply to slow leaks inside walls.

Read More →

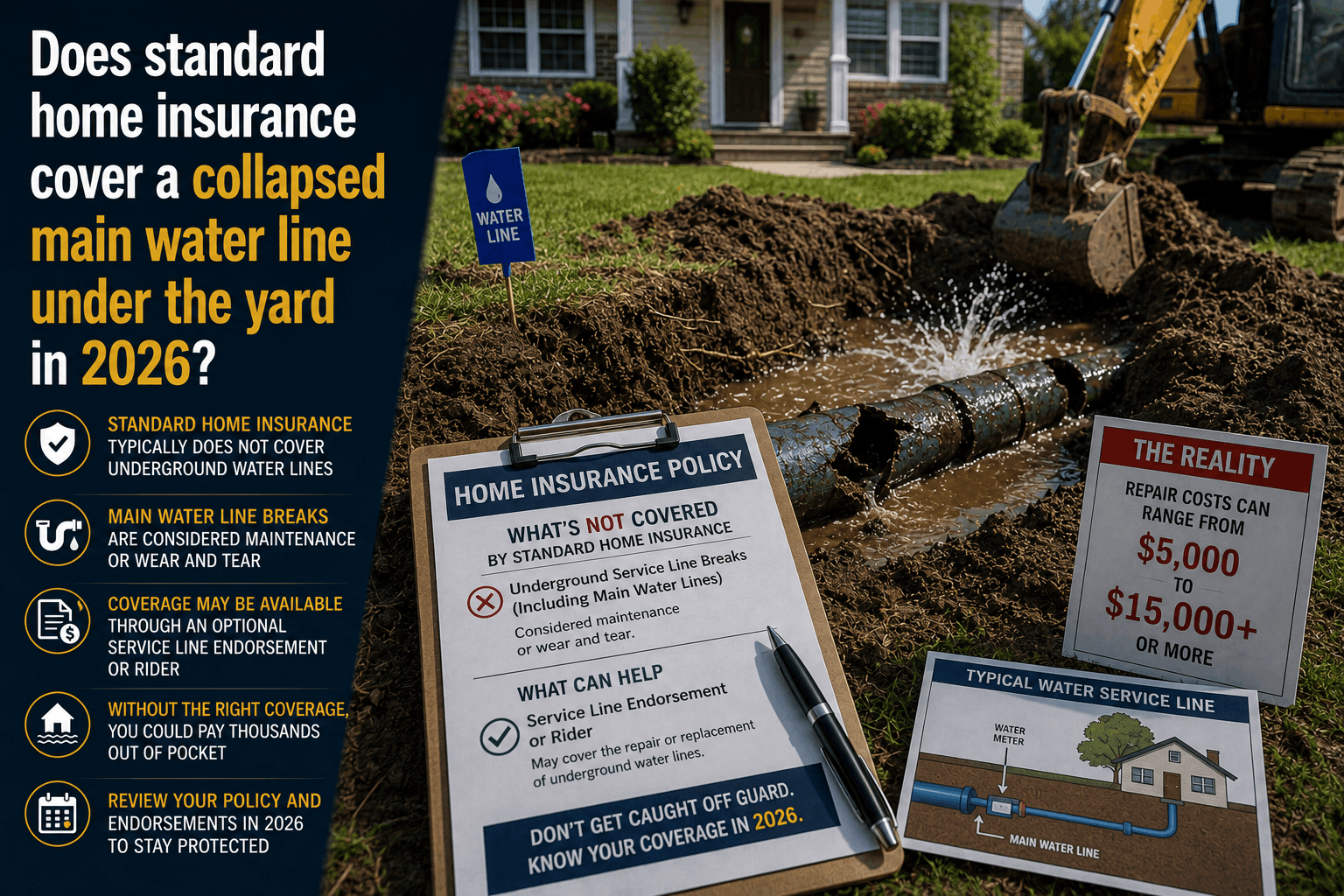

Does Home Insurance Cover a Collapsed Water Line in the Yard? (2026 Rules)

Find out if standard home insurance covers a water line collapse under your yard. Learn about the strict "slab-up" rule and the crucial Service Line Endorsement.

Read More →