Does Home Insurance Cover a Collapsed Water Line in the Yard? (2026 Rules)

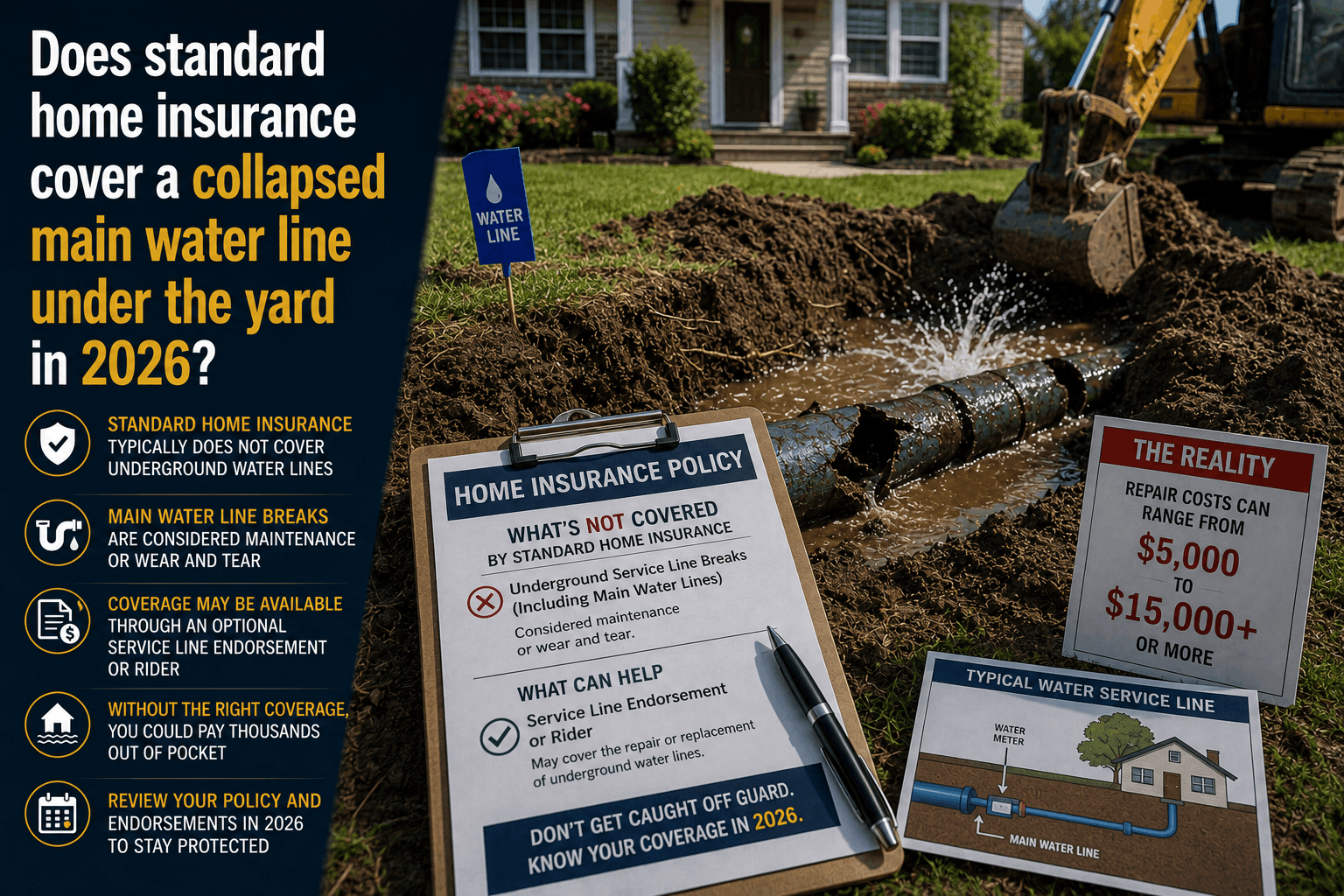

"Does Standard Home Insurance Cover a Collapsed Main Water Line Under the Yard in 2026?"

The Direct Answer: No, a standard homeowners insurance policy will completely deny a claim for a collapsed main water line under your yard. While your policy is contractually designed to pay for the massive water damage inside your home if an interior pipe bursts suddenly, its protection stops at the outer perimeter of your house.

In the structural framework of 2026 insurance underwriting, policies apply a strict "slab-up" boundary rule.

The main water line running underneath your front grass to the city street connection is legally considered your private maintenance responsibility. If it collapses due to soil shifting, age-related rust, or aggressive tree root intrusion, a standard policy will not pay for the excavation, the new piping, or the ruined landscaping. To cover this deep-earth disaster, you must add an optional rider known as an Underground Service Line Endorsement.

1. The Anatomy of a Front Yard Denial

When a main water line breaks beneath your lawn, it usually manifests as a mysterious marshy puddle in your grass, a sudden drop in household water pressure, or a catastrophic spike in your monthly utility bill.

If you contact your insurance company's claims hotline, the adjuster will separate the incident into two distinct zones:

[Zone 1: Interior Plumbing Leaks] ──> COVERED if sudden and accidental.

[Zone 2: Exterior Buried Lines] ──> EXCLUDED entirely by default.

Standard dwelling coverage (Coverage A) is designed to protect the physical house and attached architectural structures. Underground, exterior utility lines are explicitly named in the policy jacket's exclusions under sections detailing "wear and tear," "earth movement," and "underground pipes."

Even though the municipal water company dictates that you own the pipe all the way from your foundation to the street curb meter, your base insurance contract simply treats it as uninsured outdoor property.

2. The 2026 Calibration: Why Excavation Bills Are Soaring

Ignoring this massive gap in your property insurance is incredibly risky. Across the country—and specifically in aging Florida suburban corridors like Stuart—underground pipe failures are reaching an all-time high.

Macroeconomic data highlights why a broken water main is a significant household budget killer:

- The Labor Squeeze: Fixing a buried main line requires specialized, heavy excavation machinery, state-mandated utility tracking permits, and trench safety logistics. Contractor labor inflation has driven baseline repair bills to an average of $7,000 to $12,000 per incident.

- The Environmental Calibration Trap: Modern local zoning codes dictate that contractors cannot simply fill a trench with loose dirt and walk away. If the line runs underneath your paved driveway, sidewalk, or custom landscaping, you must pay out of pocket for full structural backfilling, asphalt repaving, and cosmetic turf restoration.

3. The One Extreme Peril Exception

There is only one rare scenario where a standard, un-endorsed homeowners policy will pay for an underground line failure, and it requires a catastrophic external trigger:

The Rule: If a third-party construction crew, commercial vehicle, or utility worker accidentally strikes your buried main water line while operating heavy equipment on your property (such as digging a trench for a neighbor's pool), your policy’s Vandalism or Malicious Mischief / Accidental Third-Party Damage clauses can be triggered.

Even in this scenario, your insurance company will usually require you to file a claim directly against the at-fault contractor’s commercial liability bond rather than paying out the funds from your own policy contract.

How to Close the Buried Line Loophole Safely

If your property asset is currently resting on a basic, off-the-shelf homeowners policy, your cash reserves are entirely exposed to a single subterranean root.

At Walker Insurance Agency, we unbundle this vulnerability and secure your yard using a highly cost-effective policy adjustment:

Step 1: Conduct a Comprehensive Review of Active Property Riders

Step 2: Bind a Specialty Service Line Endorsement with a $10,000+ Limit

========================================================================

= Total Coverage for Excavation, New Piping, Hardscaping, and Hotel Stays

Adding a dedicated Underground Service Line Endorsement to your homeowners policy is one of the highest-value plays available, typically costing a mere $20 to $50 per year.

This specialized rider completely overrides the standard exclusions. If your incoming water main, sewer lateral, buried electrical conduit, or fiber-optic internet line ruptures, the rider steps in to pay for the heavy equipment digging, the brand-new replacement infrastructure, and the full restoration of your ruined lawn, trees, and concrete walkways. Most riders carry a predictable, flat $500 deductible, converting a potential $10,000 financial emergency into a simple administrative claim.

Why Working with an Independent Agency is Vital

Attempting to manage a complex property asset through a generic smartphone application or automated online broker ensures you will miss the critical riders needed to survive infrastructure aging. At Walker Insurance Agency, we provide the personalized, data-driven visibility you need to insulate your family wealth.

The Walker Advantage:

- Rider Scope Optimization: We audit your home's age and pipeline composition to ensure your service line limits accurately mirror local Stuart excavation rates.

- Water Backup Synchronization: We seamlessly bridge your buried utility coverage with your internal Water Backup Riders, ensuring you have 100% comprehensive wastewater protection from the street curb to your kitchen sink.

- Market Stabilization Evaluation: As the private market stabilizes with 20 brand-new property carriers entering Florida, we continually shop your profile to secure the highest-limit property riders at the absolute lowest available premium floors.

FAQ

1. Does a service line endorsement cover an on-site well water pump failure?

While the endorsement will pay to excavate and replace the physical buried line running from your house to the private well, it will never pay to replace the mechanical well pump machinery itself or the internal water storage pressure tank. Those complex mechanical components require a separate Equipment Breakdown Endorsement.

2. Can I get this underground coverage if my home has old cast-iron or clay pipes?

Yes. Most top-tier independent insurance companies do not restrict or deny a service line endorsement based strictly on the chronological age or original structural material of your pipes, provided there is no pre-existing, documented ongoing leak or active utility failure at the exact moment you bind the coverage.

3. What should I do immediately if I suspect my main water line has fractured under my lawn?

Do not let a plumbing contractor immediately tear up your yard with a backhoe before contacting your agent. Call a professional leak detection service to perform a non-invasive sonic or digital camera inspection. Secure a copy of the diagnostic video file and a formal quote detailing the exact cause and location of the line fracture. This data serves as the primary verification needed to open a valid, successful claim.

Insulate Your Savings from an Underground Disaster Today

A main water line collapse is destructive, highly disruptive, and incredibly expensive to excavate. Relying on an ordinary, baseline home insurance policy to handle a subterranean emergency is a gamble that can wipe out thousands of dollars from your family's savings account the moment an aging pipe reaches its breaking point.

Secure your yard before an emergency strikes. Contact Walker Insurance Agency today for a comprehensive property coverage audit. We provide the visibility you need to eliminate hidden utility loops, deploy high-limit service line riders, and protect your hard-earned wealth safely in Stuart.

[GET A FREE QUOTE TODAY]

Call us at +1-407-977-7100 or visit our office in Stuart, FL. Let us secure your property boundaries today.

Related Articles

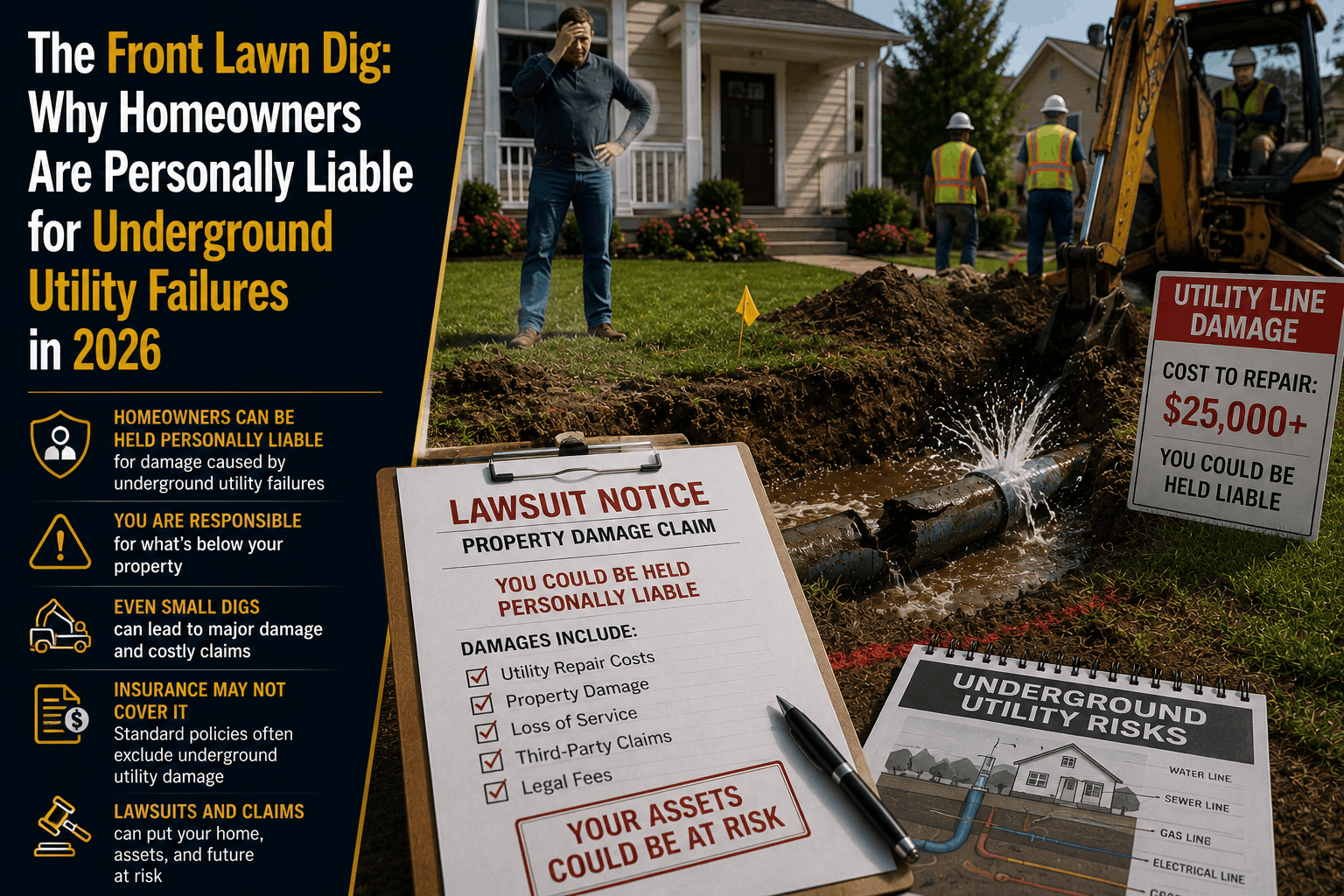

The Front Lawn Dig: Why You Own the Underground Utility Risk in 2026

Think the city pays if an underground pipe bursts under your lawn? Discover why standard Florida home insurance leaves you personally liable for buried utility lines.

Read More →

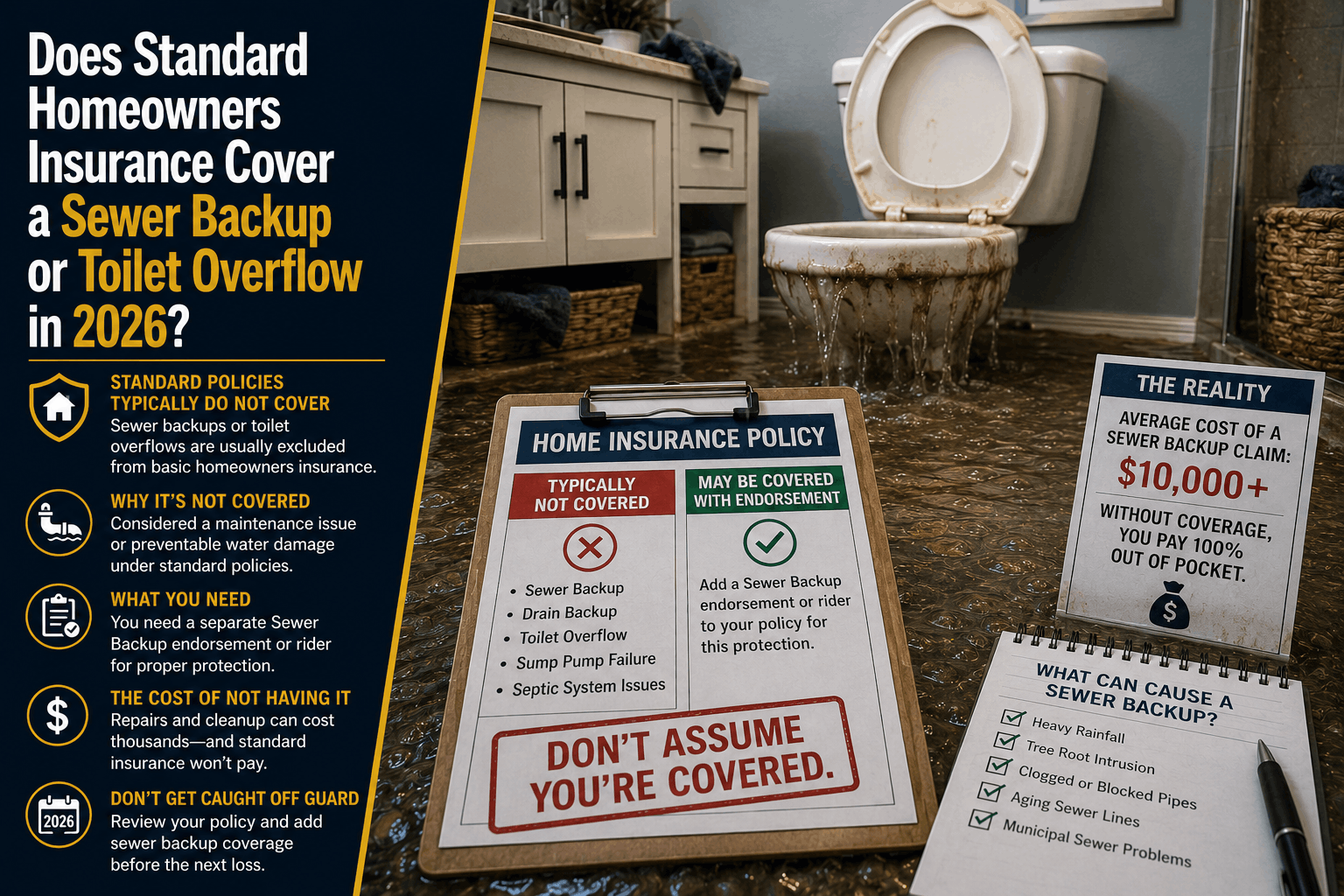

Does Homeowners Insurance Cover Sewer Backup or Toilet Overflow? (2026 Guide)

Discover how standard homeowners insurance handles sewage backups and toilet overflows in 2026\. Learn the strict rules that separate a covered claim from a denial.

Read More →

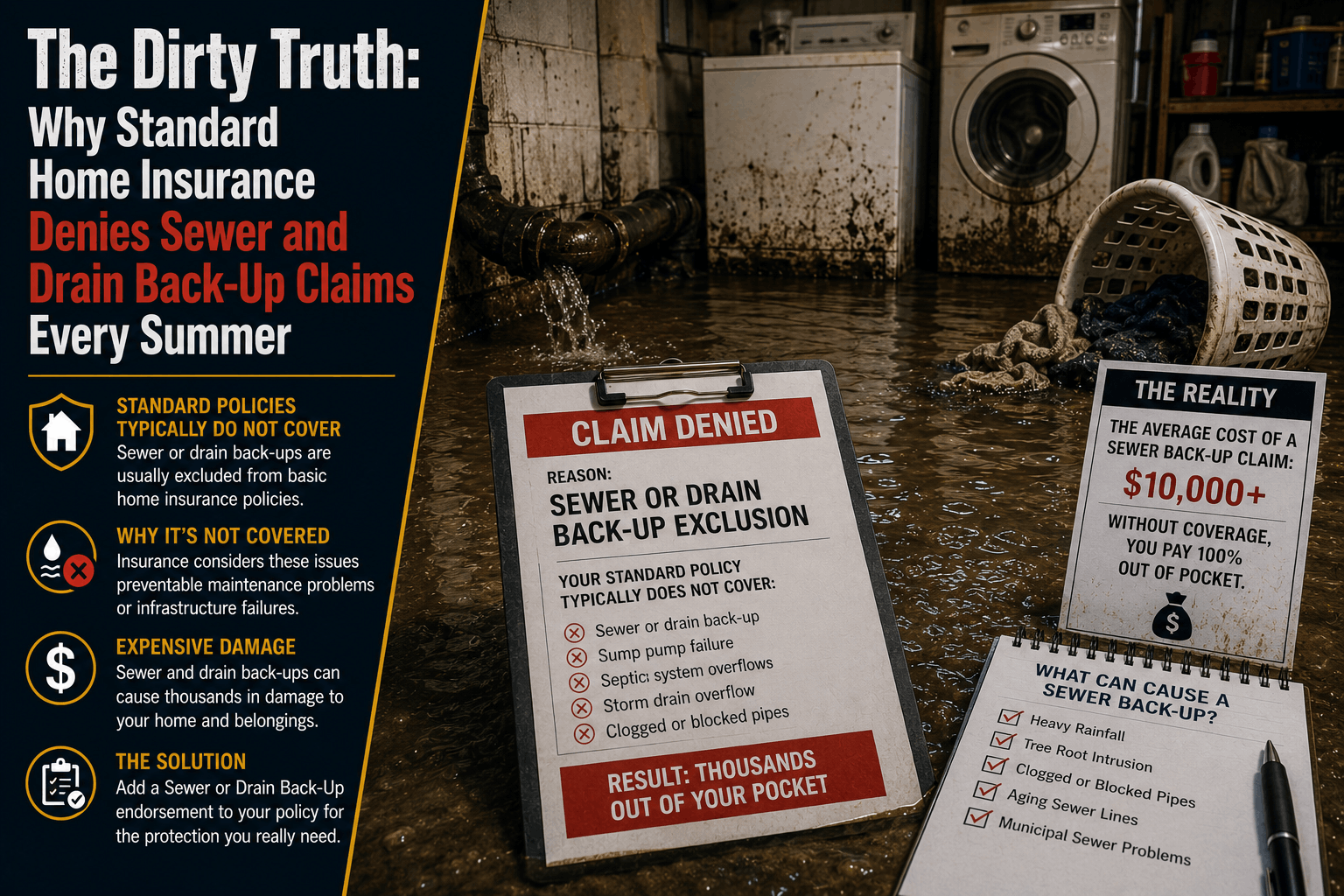

The Dirty Truth: Why Standard Home Insurance Denies Sewer Back-Up Claims Every Summer

Discover why standard home insurance completely denies summer sewage and drain backup claims. Learn about hidden exclusions and the necessary water backup rider.

Read More →