Does Homeowners Insurance Cover Sewer Backup or Toilet Overflow? (2026 Guide)

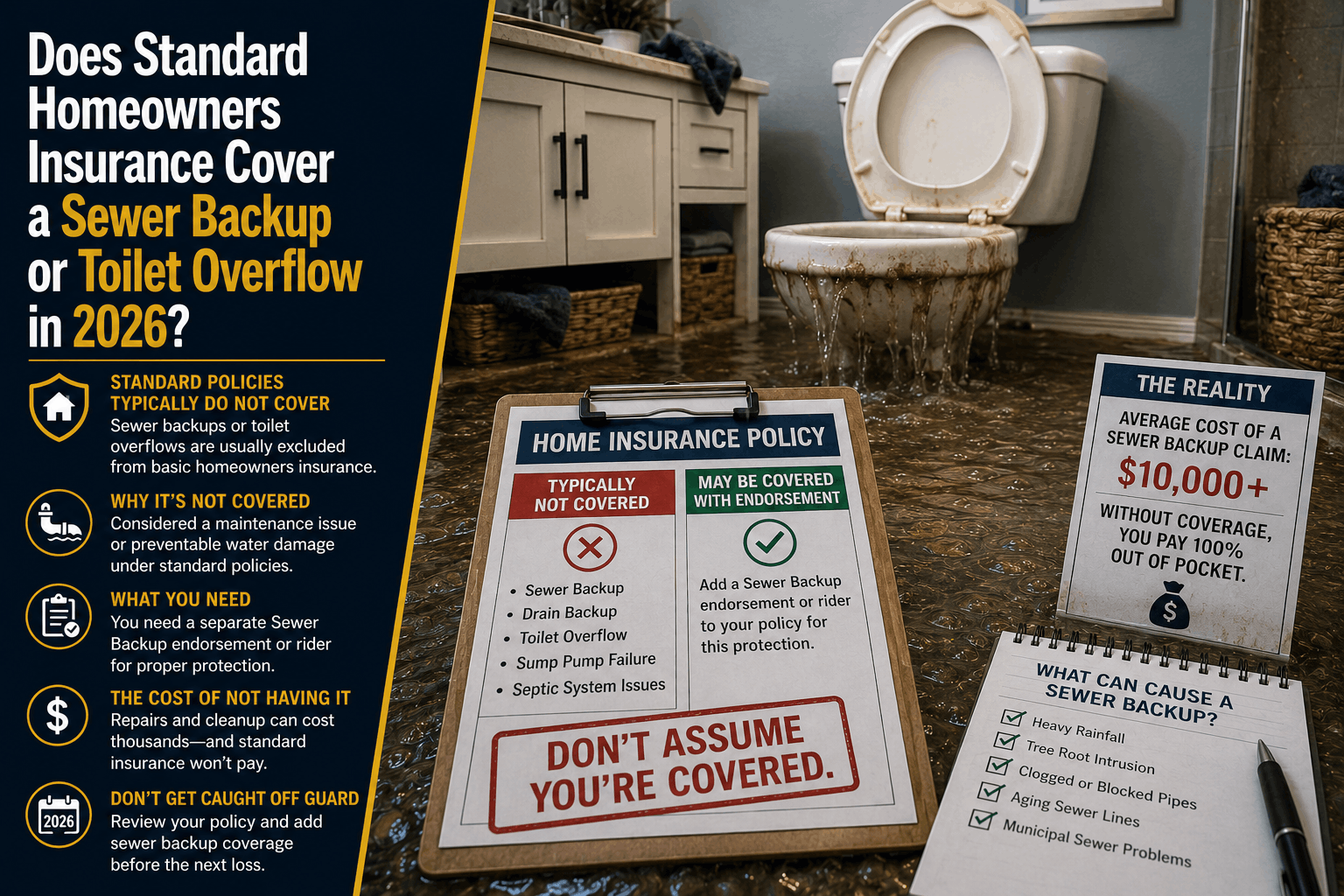

Does Standard Homeowners Insurance Cover a Sewer Backup or Toilet Overflow in 2026?

The Direct Answer: It depends entirely on where the blockage originates. A standard homeowners insurance policy will cover a toilet overflow if the incident is caused by a sudden, accidental clog inside your home’s immediate plumbing line (such as a child flushing a toy). However, a standard policy will completely deny a sewer backup if the raw sewage or water flows backward into your home from the municipal sewer system, an off-premises drain, or a failed sump pump.

In 2026, this distinction is incredibly high-stakes. Driven by severe seasonal storms and aging municipal infrastructure, sewer lines routinely experience reverse-pressure surges.

To achieve total visibility over your property defenses, you must realize that if dirty water backs up into your home from outside your property line, your carrier will legally deny 100% of the cleanup, bio-sanitation, and flooring bills unless you have explicitly paid for an optional add-on endorsement known as a Water Backup and Sump Pump Overflow Rider.

1. The Covered Scenario: The Internal Toilet Overflow

If you walk into your bathroom and find clean water pouring over the porcelain rim of your toilet, your standard policy is contractually designed to assist you, provided the disaster clears the "Sudden and Accidental" hurdle:

- The Internal Clog: If a drain line inside your home becomes blocked unexpectedly, the ensuing water damage to your drywall, baseboards, and subflooring falls under your primary Dwelling Coverage (Coverage A).

- Belongings Protection: Ruined bathroom rugs, towels, or adjacent bedroom furniture are covered under your Personal Property Coverage (Coverage C), minus your standard policy deductible.

- The Catch: While your policy covers the consequential property damage caused by the water, it will never pay for the plumber to snakes the line or repair the faulty mechanical components of the toilet itself.

2. The Denied Scenario: The External Sewer Backup

The moment water or waste flows in a reverse direction, moving upward through your showers, floor drains, or toilets because of an external issue, your standard insurance framework collapses.

[Blockage Location: Inside Your Walls] ──> COVERED under baseline policies.

[Blockage Location: Municipal Main Line] ──> DENIED entirely by default.

The Off-Premises Exclusion: Standard policy language explicitly excludes any damage originating from the backup of sewers, drains, or septic systems located off your primary premises. If a municipal main line bottlenecks during a heavy downpour and forces waste backward into your home, your carrier views this as an environmental infrastructure failure rather than an accidental internal plumbing leak.

3. The 3 Technical Loopholes Insurers Use Today

Even if you file an internal overflow claim, claims adjusters in the modern property market use advanced diagnostic testing to search for three specific technical exclusions to discard your claim:

- The Maintenance Negligence Trap: Insurance contracts are not maintenance warranties. If an adjuster lowers a camera down your drain and determines the overflow was caused by years of slow, chronic grease buildup or a pre-existing root infiltration that you ignored, they will deny the claim on the grounds of homeowner neglect.

- The 14-Day Seepage Boundary: If a toilet overflows in a guest house or basement while you are away on an extended vacation, and the moisture sits undetected, standard policies state that any water or mold damage occurring over a period of 14 days or longer is automatically excluded from reimbursement.

- The Concurrent Flood Exclusion: If a heavy summer storm floods your lawn, and that surface water enters your home at the same time your municipal sewer backs up, the carrier will invoke the Concurrent Causation Clause. If an excluded peril (surface flooding) happens simultaneously with a backup, the entire claim is discarded. To survive this event, you must carry separate Flood Insurance.

How to Safely Close the Sewer Loophole

If your home is sitting on a baseline property contract with zero endorsements, your savings are exposed to a massive biohazard remediation risk.

At Walker Insurance Agency, we advise property owners to protect their wealth using a precise, two-step structural layout:

Step 1: Add a Water Backup and Sump Pump Overflow Rider (Targets Internal Cleanup)

Step 2: Layer an Underground Service Line Endorsement (Targets External Pipe Digs)

==================================================================================

= 100% Comprehensive Wastewater Protection from the Concrete Slab to the Street

Adding a dedicated Water Backup Rider is highly cost-effective, typically costing between $50 and $100 per year. This rider overrides the standard exclusion, paying for professional hazardous extraction teams to dry, sanitize, and rebuild your home after an external municipal backup. When setting up this rider, do not accept a generic baseline limit—ensure you lock in a minimum of $10,000 to $25,000 in coverage to handle the severe costs associated with hazardous bio-clean processes.

Why Working with an Independent Agency is Vital

Attempting to manage a complex property asset through a faceless smartphone application ensures you will miss the critical riders needed to survive regional infrastructure emergencies. At Walker Insurance Agency, we provide the data-driven visibility you need to insulate your home.

The Walker Advantage:

- Rider Customization Audits: We evaluate your home's layout to determine if your basement, foundation level, or pipeline material requires an enhanced backup limit.

- Service Line Synchronization: We cross-reference your home policy with specialized underground pipe coverage, ensuring you aren't stuck paying $5,000+ out of pocket to excavate a cracked sewer lateral line under your lawn.

- Market Stabilization Shopping: As the stabilizing Florida market introduces 20 brand-new private property companies, we continuous match your profile with carriers offering the highest water backup caps at the lowest available premium floors in Stuart.

FAQ

1. Does my standard home policy cover a septic tank backup? A standard policy will only cover a septic backup if it is directly triggered by an covered, acute peril like a lightning strike or an explosion on your property. If the septic system backs up due to heavy rainfall saturation, tree root intrusion, or lack of regular pumping, it is completely excluded unless you carry a water backup endorsement.

2. If a backup is the city's fault, won't the city pay for my damages? Rarely, and never quickly. Most municipalities carry strict sovereign immunity laws that protect them from liability regarding utility grid overflows during severe storm events. Even if the city acknowledges negligence, navigating the municipal claims process can take months, whereas your private backup endorsement can deploy a remediation crew to your house within hours.

3. What should I do immediately if my toilet overflows or backs up? Turn off the water isolation valve located directly behind the toilet tank immediately. Do not attempt to repeatedly flush the fixture. Take high-resolution photos and videos of the point of overflow, document all contaminated personal property, and contact your independent agent before authorizing permanent, non-emergency structural repairs.

Protect Your Home from a Costly Biohazard Crisis

A sewage backup is one of the most toxic, destructive, and financially draining events a property owner can experience. Relying on an ordinary, unmodified home insurance policy to handle a wastewater emergency is a gamble that can instantly wipe out thousands of dollars from your family's savings account.

Verify your water endorsements before the next big storm. Contact Walker Insurance Agency today for a comprehensive policy audit. We provide the visibility you need to eliminate hidden drain loopholes, secure high-limit backup riders, and protect your family's lifestyle safely in Stuart.

[GET A FREE QUOTE TODAY]

Call us at +1-407-977-7100 or visit our office in Stuart, FL. Let us secure your property today.

Related Articles

Does Collision Cover Hit-and-Run Damage Without a Deductible? (2026)

Had your car struck in a hit-and-run? Learn how collision coverage applies, when deductibles are required, and how UMPD can save you money in 2026.

Read More →

Does Collision Insurance Cover Hail & Tree Damage in 2026?

Did hail or a falling tree branch damage your car? Learn why collision auto insurance won't pay for storm damage and how comprehensive coverage protects you.

Read More →

Why Collision Insurance Pays $0 for Non-Crash Summer Damage (2026)

Did a tree branch, hail storm, or flying road debris hit your car this summer? Discover why collision auto insurance pays $0 and how comprehensive coverage protects you.

Read More →