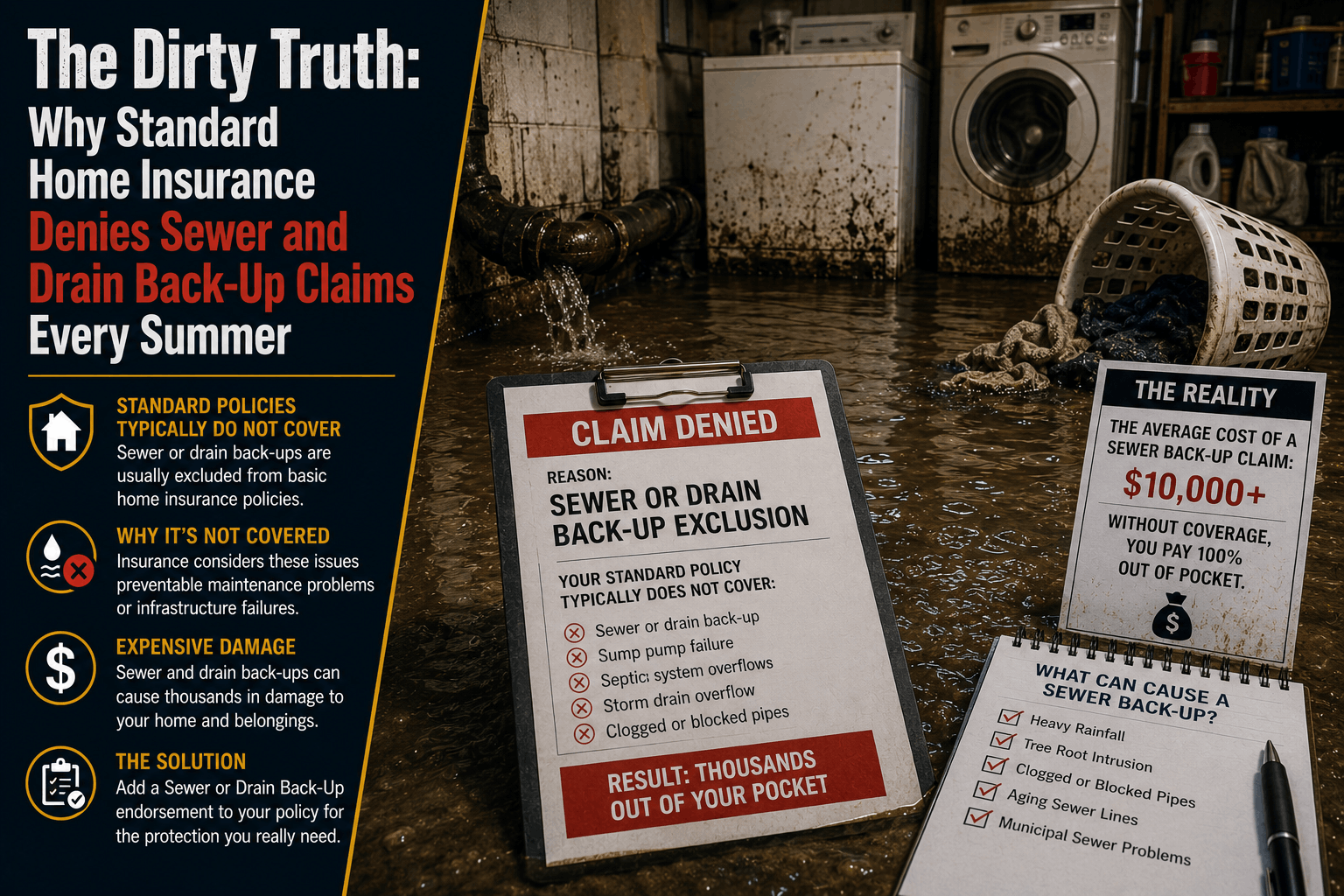

The Dirty Truth: Why Standard Home Insurance Denies Sewer Back-Up Claims Every Summer

The Dirty Truth: Why Standard Home Insurance Denies Sewer and Drain Back-Up Claims Every Summer

The Direct Answer: The devastating reason your insurance company will completely deny a raw sewage or drain backup claim this summer is simple: standard homeowners insurance policies explicitly exclude it. There is a massive structural difference between a pipe bursting inside your walls (which standard policies cover as a sudden, accidental discharge) and water backing up through an interior drain, toilet, or sump pump.

In 2026, this exclusion catches thousands of property owners completely off guard during the summer months. When severe tropical storms, afternoon downpours, or localized flash floods overwhelm an aging municipal infrastructure, sewage flows backward through your home's main lateral line.

To achieve total visibility over your property defenses, you must accept that unless you have explicitly paid for an optional, add-on endorsement known as a Water Backup and Sump Pump Overflow Rider, your carrier will legally deny 100% of the cleanup, mold mitigation, and structural repair bills.

1. The Summer Convergence: The Anatomy of a Backup

Sewer and drain backups peak during the summer season due to a perfect storm of environmental, structural, and behavioral factors that happen all at once:

- The Inundation Squeeze: Intense summer thunderstorms dump several inches of water in a matter of minutes. When this massive volume hits an aging municipal storm sewer system, the grid reaches peak capacity. The water looks for the path of least resistance—which frequently means shooting backward through the lowest plumbing drains of private residential homes.

- The Tree Root Infiltration: During the hot summer months, large subterranean tree roots actively seek out moisture. They naturally target underground clay or cast-iron sewer lines, cracking the pipes and creating tight, structural blockages that trap solid materials until the system backs up into your shower pan or utility sink.

- The F.O.G. Factor: Summer means backyard barbecues, which leads to a dramatic spike in Fats, Oils, and Grease (F.O.G.) being rinsed down kitchen sinks. Grease solidifies inside cool subterranean pipes, creating massive chemical blocks (often called "fatbergs") that completely choke residential drainage paths.

2. Why the Standard "Sudden and Accidental" Rule Fails

When raw sewage ruins your baseboards, carpets, and drywall, standard policy logic assumes the damage should be covered because the incident happened suddenly. However, claims adjusters utilize a strict diagnostic framework to separate covered water from excluded water:

[Source: Pipe Burst Inside Your Wall] ──> COVERED under standard policy lines.

[Source: Reverse Flow Through a Drain] ──> EXCLUDED entirely by default.

The Source Rule: Standard dwelling coverage (Coverage A) is built to cover water moving in its intended direction that suddenly escapes from a broken appliance or broken copper line. The moment water or sewage moves in a reverse direction—originating from outside your property lines or backing out of an architectural drain—the contract treats it as a non-covered event.

3. The 3 Technical Loopholes Insurers Use Every Summer

Even if you purchased a baseline water backup endorsement, claims adjusters use advanced diagnostic software to search for three specific technical exclusions to throw out your claim:

Exclusion 1: The Maintenance Negligence Trap

Insurance contracts mandate that homeowners maintain their personal property infrastructure. If an adjuster lowers a camera down your lateral sewer line and discovers that the backup was caused by years of slow, gradual tree root intrusion or disintegrated, rusted pipes that you ignored, they will deny the claim. The contract requires the backup to be triggered by a sudden, external municipal system failure—not chronic homeowner neglect.

Exclusion 2: The 14-Day Gradual Seepage Rule

Sewage backups aren't always a sudden geyser; sometimes they manifest as a slow, quiet bubble in a hidden guest bathroom or basement utility closet while your family is away on a summer vacation. Standard policies state that any water or moisture damage occurring over a period of 14 days or longer is automatically classified as a maintenance issue and is completely barred from reimbursement.

Exclusion 3: The General Surface Water (Flood) Exclusion

This is the ultimate loophole. If a massive summer storm dumps rain that floods your yard, and that surface water enters your home from the ground at the same time your sewer backs up, the carrier will invoke the Concurrent Causation Clause. If an excluded peril (a surface flood) occurs simultaneously with a covered peril (a drain backup), the entire claim is discarded. To survive this event, you must carry a standalone Flood Insurance Policy alongside your backup rider.

How to Safely Build a Clean Water Shield

If your home is currently sitting on a basic property policy with no custom endorsements, your savings are exposed to a multi-thousand dollar biohazard cleanup risk.

At Walker Insurance Agency, we unbundle this exposure and fortify your policy using a precise, three-tier framework:

Step 1: Unearth and Eradicate Hidden Drain Exclusions

Step 2: Add a Water Backup Rider with a Minimum $10,000 Limit

Step 3: Pair the Rider with an Underground Utility Line Endorsement

=====================================================================

= Total Structural Protection From Internal Bloat to External Pipes

Adding a dedicated Water Backup and Sump Pump Overflow Endorsement is extraordinarily affordable, frequently costing as little as $30 to $100 per year. When binding this rider, you must choose a distinct coverage limit—typically ranging from $5,000 to $25,000. If you have a finished basement or high-end flooring, selecting a basic $5,000 limit will leave you underinsured, as professional hazardous bio-clean teams routinely charge thousands of dollars just to sanitize the structure before structural rebuilding can even begin.

Why Working with an Independent Agency is Vital

Attempting to manage a complex property asset through a faceless online application means your policy is missing the critical endorsements needed to survive local infrastructure failures. At Walker Insurance Agency, we provide the personalized, data-driven visibility you need to defend your home.

The Walker Advantage:

- Endorsement Limit Optimization: We audit your home's architecture to calculate the exact dollar limit required to cover hazardous cleanup and drywall replacement.

- Utility Line Coordination: We help you layer separate Buried Utility Line coverage, which pays to dig up and repair the actual physical sewer pipe running under your lawn—a cost the water backup rider never covers.

- Carrier Stabilization Management: As the 2026 Florida market stabilizes with 20 brand-new private property companies, we match your profile with carriers that offer high-limit backup endorsements at the lowest rate floors in Stuart.

FAQ

1. Does a standard homeowners policy cover a toilet that overflows because it was clogged by a child?

Yes, usually. If a toilet overflows suddenly because a foreign object block inside the immediate internal trap causes water to spill over the porcelain rim, it is typically covered under your standard policy as an accidental discharge from a plumbing fixture. The drain backup exclusion specifically targets water backing up from beyond the fixture or entering from external sewage mains.

2. Does a water backup endorsement pay to replace my broken sump pump?

No. The water backup endorsement is strictly designed to pay for the consequential physical damage caused by the water—such as ruined carpets, warped cabinets, and mold remediation. It will not pay to repair or replace the mechanical sump pump device or hot water heater that failed. To cover the physical machinery, you must add an Equipment Breakdown Endorsement.

3. How do I prove to my insurer that a summer backup was sudden and not a maintenance issue?

If you experience a backup, call a licensed plumber immediately. Have them document the acute cause of the blockage on their formal service invoice (e.g., "municipal main line pressure surge"). Take high-resolution photos of the points of entry, and do not flush or clear the lines until the data-gathering timeline is fully recorded for your independent agent.

Insulate Your Home from a Biohazard Disaster Today

A sewer backup is one of the most toxic, destructive, and expensive claims a homeowner can face. Relying on an ordinary, baseline insurance policy to cover a reverse-drain emergency is an administrative gamble that will destroy your family’s budget the moment a summer storm hits your zip code.

Lock in your protection before the next storm rolls in. Contact Walker Insurance Agency today for a comprehensive 2026 Property Coverage Audit. We provide the visibility you need to erase hidden exclusions, deploy high-limit backup riders, and secure your lifestyle safely in Stuart.

[GET A FREE QUOTE TODAY]

Call us at +1-407-977-7100 or visit our office in Stuart, FL. Let us protect your property today.

Related Articles

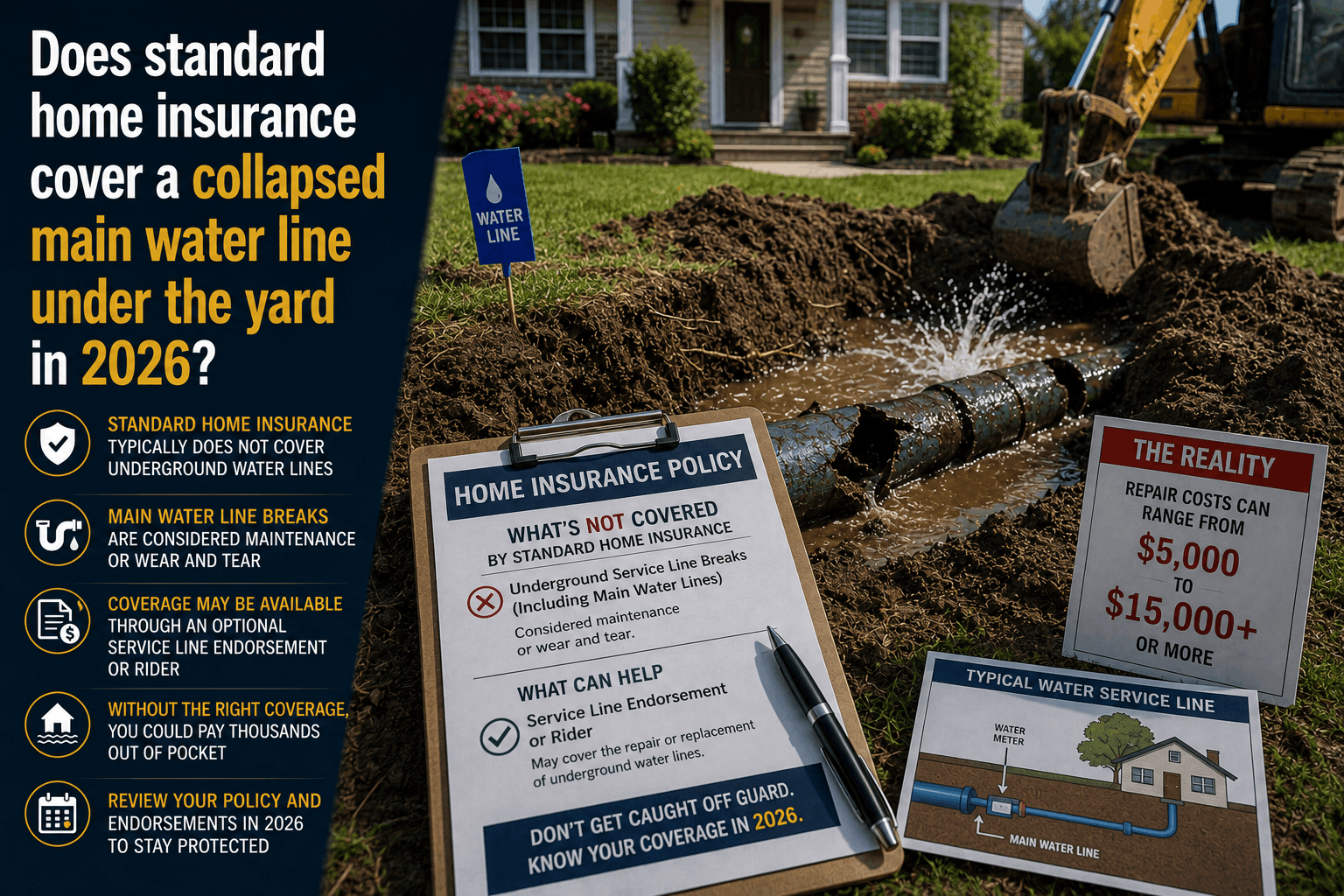

Does Home Insurance Cover a Collapsed Water Line in the Yard? (2026 Rules)

Find out if standard home insurance covers a water line collapse under your yard. Learn about the strict "slab-up" rule and the crucial Service Line Endorsement.

Read More →

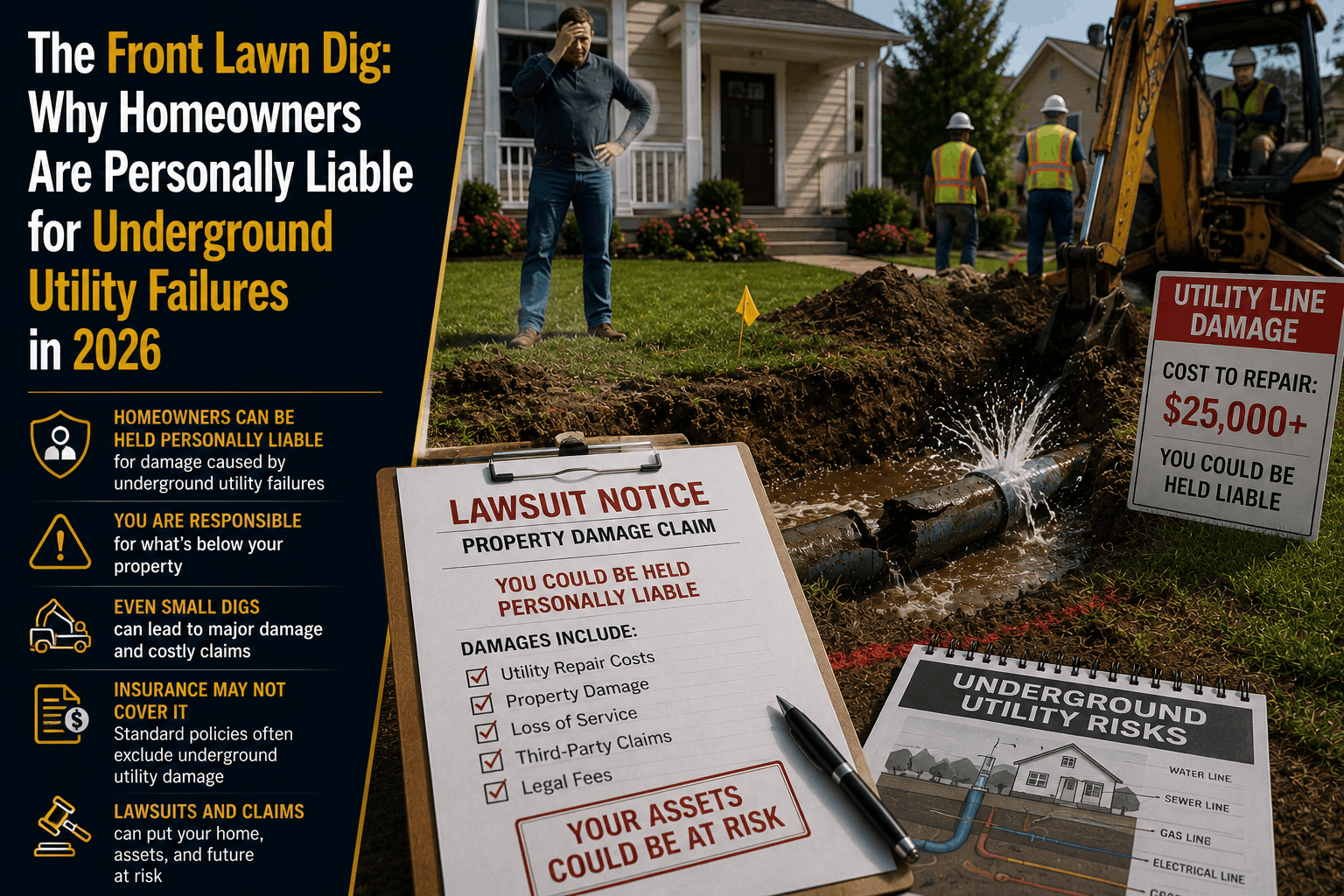

The Front Lawn Dig: Why You Own the Underground Utility Risk in 2026

Think the city pays if an underground pipe bursts under your lawn? Discover why standard Florida home insurance leaves you personally liable for buried utility lines.

Read More →

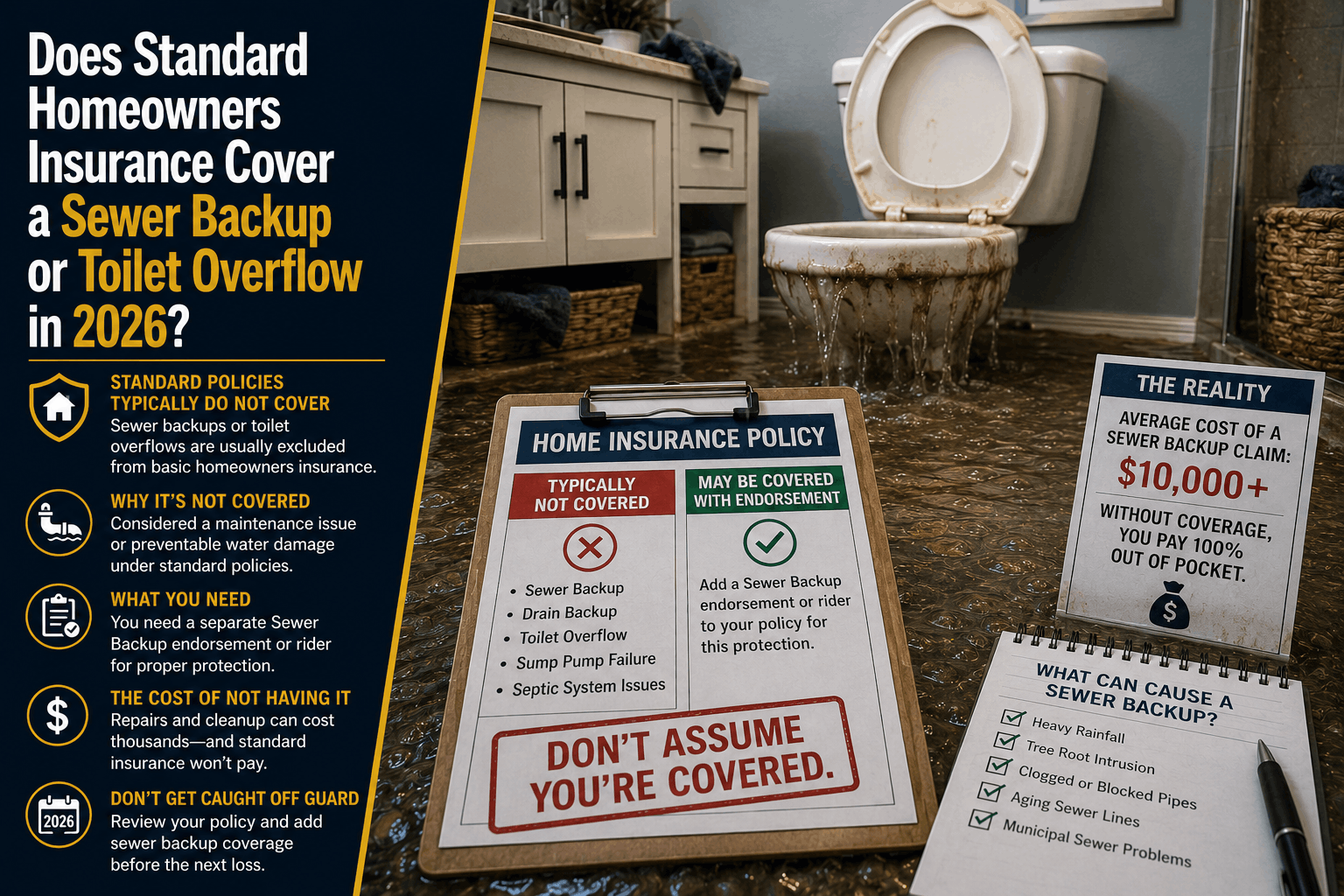

Does Homeowners Insurance Cover Sewer Backup or Toilet Overflow? (2026 Guide)

Discover how standard homeowners insurance handles sewage backups and toilet overflows in 2026\. Learn the strict rules that separate a covered claim from a denial.

Read More →