The Grid Surge Loophole: Home Insurance & Smart Appliances

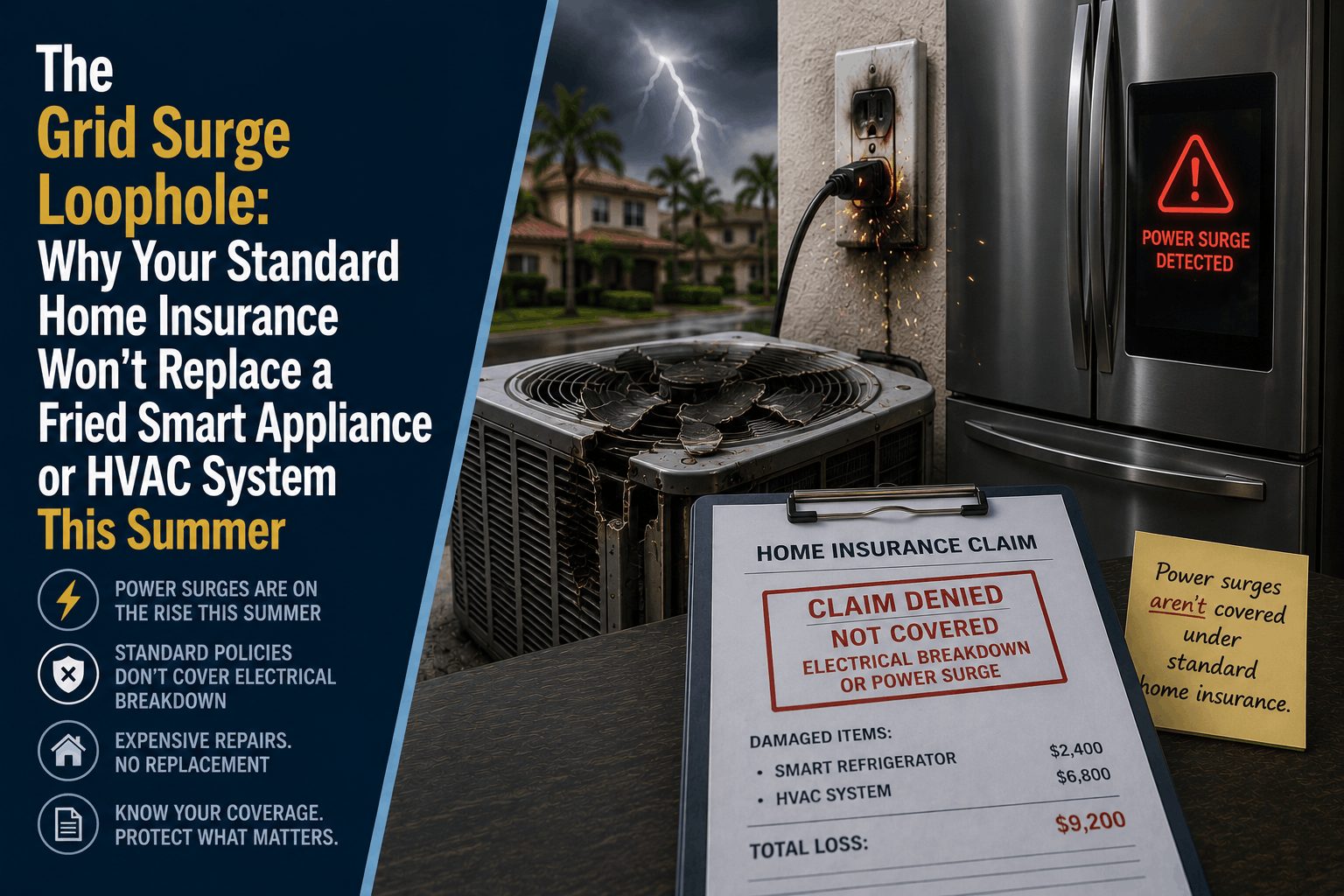

The Grid Surge Loophole: Why Your Standard Home Insurance Won't Replace a Fried Smart Appliance or HVAC System This Summer

The Direct Answer: If a summer heatwave triggers a rolling blackout and the resulting power grid surge (grid surge) fries the computer circuit boards inside your smart refrigerator or the compressor of your central HVAC system, your standard home insurance policy will completely deny the claim. There is a critical contractual loophole in traditional policies that separates a lightning strike from a municipal utility grid fluctuation.

Standard homeowners insurance policies (HO-3 contracts) are written to cover structural damage caused by "artificially generated electrical current" only if a physical bolt of lightning directly strikes your property or adjacent utility poles on your land.

With the electrical grid operating at maximum capacity due to heavy air conditioning demands, utility voltage fluctuations are constant. To achieve total visibility over your property protection, you must realize that if a power surge originates out on the street due to municipal grid stress, your insurance carrier will classify the loss as an uncovered commercial utility risk.

1. The Anatomy of the Summer Electrical Loophole

During peak summer months, heavy residential power consumption saturates local sub-stations. When the grid bottlenecks and brownouts occur, the subsequent restoration of power sends a massive, sudden spike of voltage traveling down residential service lines.

Claims adjusters categorize these destructive voltage spikes using an unyielding contractual framework:

[ Cause: Direct Lightning Strike to Your Roof ] ───> 100% COVERED (Named Peril).

[ Cause: Power Grid Surge from Street Mains ] ───> 100% DENIED by default HO-3 loophole.

The Smart Technology Crisis: Modern appliances and inverter-driven HVAC systems are no longer basic mechanical motors; they are advanced computers on wheels. They feature intricate printed circuit boards (PCBs), solid-state microprocessors, and Wi-Fi modules that are hypersensitive to micro-changes in voltage. What used to be a harmless power flicker for an analog appliance built in 1990 means instant death for the main motherboard of a $4,000 modern smart appliance.

2. The Financial Reality: High Cost of Fried HVAC Units

Relying on standard home insurance to protect your internal electrical infrastructure leaves you entirely exposed to modern contractor repair inflation. If a grid surge fries your home electronics this summer, these are the real numbers you face out of pocket:

- HVAC Control Inverter Boards: Replacing fried control modules, variable-speed fan components, and main circuit relays inside a modern high-efficiency air conditioning system averages $1,200 to $2,800.

- Burned Compressor Windings: If a voltage spike shorts out the electrical windings inside your AC compressor, the entire refrigerant system is contaminated. Replacing the compressor or swapping out the entire exterior condensing unit runs between $3,500 and $6,000.

3. How to Safely Close the Electrical Loophole

If you want to protect your household from a utility grid failure, you must reinforce your asset portfolio using a precise, two-layer strategy:

Layer 1: Equipment Breakdown Coverage (The Contractual Shield)

To fix this contractual vulnerability, you must request that your independent agent formally append an Equipment Breakdown Endorsement to your active homeowners policy.

- What it covers: This specific rider overrides the artificially generated current exclusion. It explicitly covers mechanical breakdown, electrical shorts, and grid surge failures for all central household infrastructure (HVAC systems, water heaters, built-in solar arrays) and large smart appliances.

- The cost benefit: For a minor premium addition (usually $25 to $50 per year), you secure up to $50,000 in dedicated protection with a flat $500 deductible, completely eliminating the need to buy overpriced individual product warranties.

Layer 2: Whole-House Surge Protective Devices (The Physical Shield)

Insurance contracts demand risk mitigation. Installing a certified Type 2 Surge Protective Device (SPD) directly onto your main electrical panel acts as a physical dam, blocking high-voltage grid spikes coming from the street before they ever reach your interior drywall circuits. Many independent carriers in Stuart offer premium discounts or require these installations to bind coverage on homes filled with smart technology.

Why Working with an Independent Agency is Vital

Allowing your property insurance to auto-renew via an online portal leaves your household completely exposed to the fine-print exclusions of the utility grid. At Walker Insurance Agency, we provide the personalized visibility you need to stay ahead of infrastructure failures.

The Walker Advantage:

- Rider Integration Audits: We analyze your current policy structure to see if you possess an active equipment breakdown rider or if your smart appliances are completely exposed.

- Mitigation Credit Structuring: We ensure that installing professional panel surge suppressors legally triggers safety credits to lower your annual insurance costs.

- Florida Market Navigation: As the domestic insurance market stabilizes with 20 new private property companies entering the state, we place your home with carriers that provide the highest equipment breakdown limits at the lowest rate floors in Stuart.

FAQ

1. If a power grid surge fries my personal laptop or television, does an equipment breakdown rider cover it? Yes. Modern, high-tier equipment breakdown endorsements cover both permanent household systems (like your HVAC) and standard personal electronics—including computers, smart TVs, and home theater systems—provided they were actively plugged into a residential circuit when the surge event occurred.

2. What happens if my AC fails because the utility company shuts off power for routine maintenance? A standard home policy will not respond to a scheduled utility maintenance outage. If your equipment is damaged by the subsequent power surge when the grid re-energizes, a standard HO-3 policy will still deny the claim because the cause originated off-premises. An Equipment Breakdown Endorsement, however, bypasses the cause completely and pays for the repair regardless of why the power dropped.

3. How do I prove to my claims adjuster that my HVAC was fried by a grid surge and not old age? When an event happens, hire a licensed HVAC technician to write a diagnostic report. The technician must open the system and document the unmistakable physical evidence of a voltage surge—such as arc marks on the circuit boards, melted capacitors, or a distinct burned plastic odor. This certified diagnostic invoice provides the exact proof your independent agent needs to open a successful claim.

Protect Your Smart Home Tech Before the Next Blackout

Your modern home functions like a giant computer, but your insurance policy might still be written under the analog rules of the 1980s. Leaving your expensive climate-control systems and smart appliances vulnerable to an unstable summer power grid is a gamble that can cost your family thousands of dollars in a single second.

Secure your electronic systems today. Contact Walker Insurance Agency for a comprehensive property policy audit. We provide the visibility you need to erase hidden coverage gaps, secure your HVAC system correctly, and protect your long-term financial security with the best coverage options in Stuart.

[GET A FREE QUOTE TODAY]

Call us at +1-407-977-7100 or visit our office in Stuart, FL. Let us protect your property investments today.

Related Articles

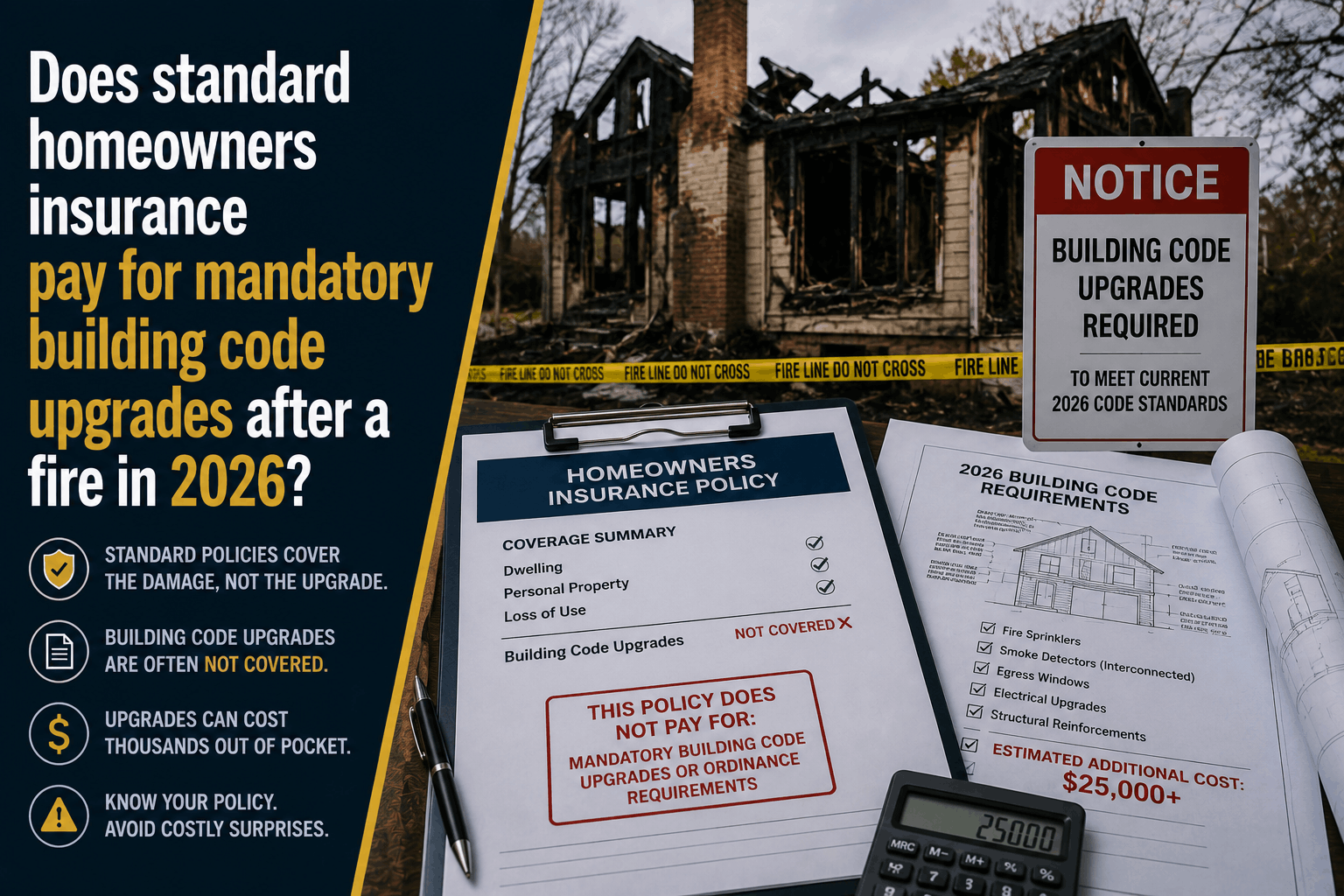

Does Homeowners Insurance Pay for Code Upgrades After a Fire?

A standard home insurance policy won't cover mandatory building code upgrades after a fire. Learn about the Ordinance or Law trap and how to protect your home.

Read More →

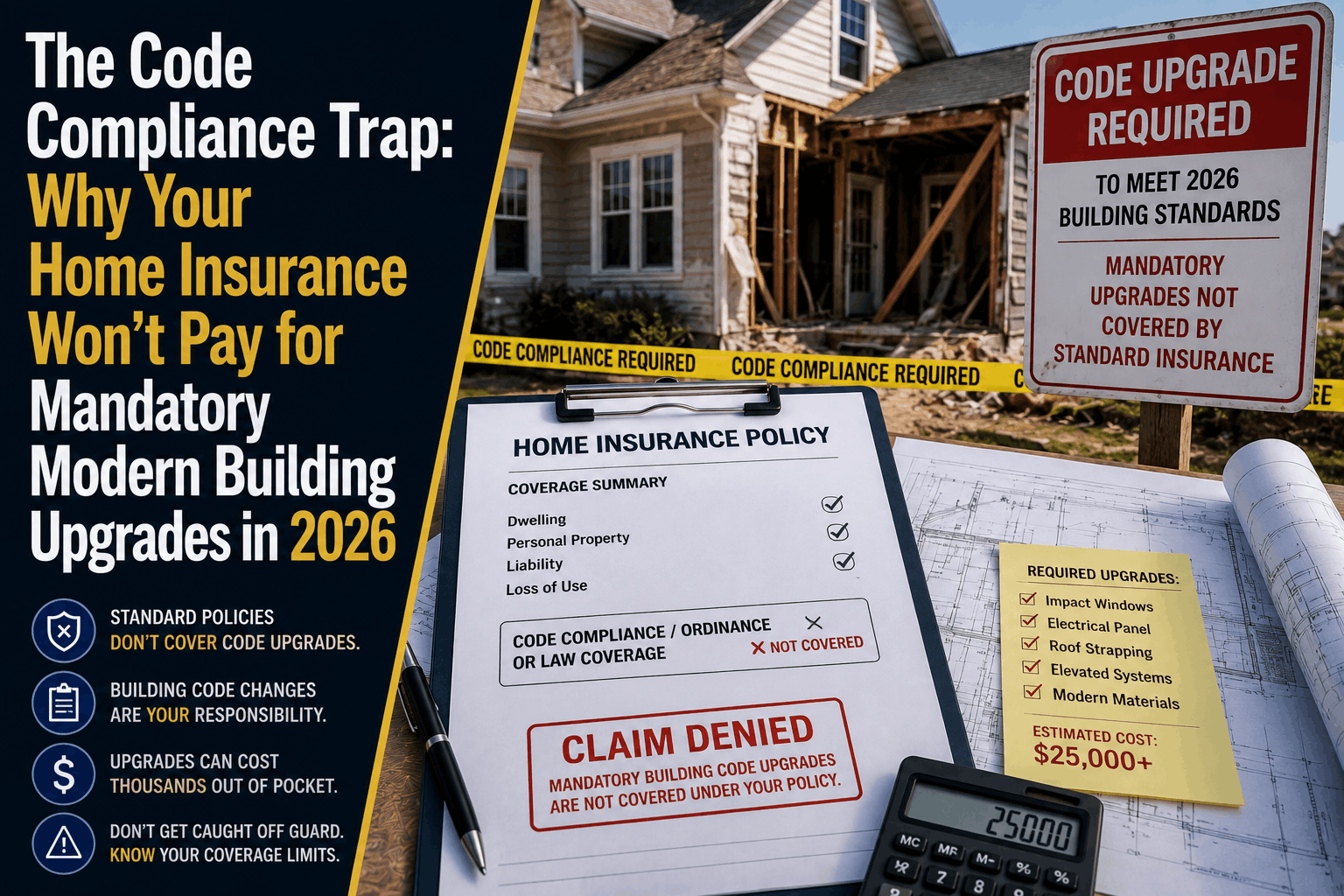

The Code Compliance Trap: Why Home Insurance Won't Pay for Upgrades

Discovered a massive gap in your property insurance after a disaster? Learn why standard home insurance completely denies mandatory building code upgrades in 2026.

Read More →

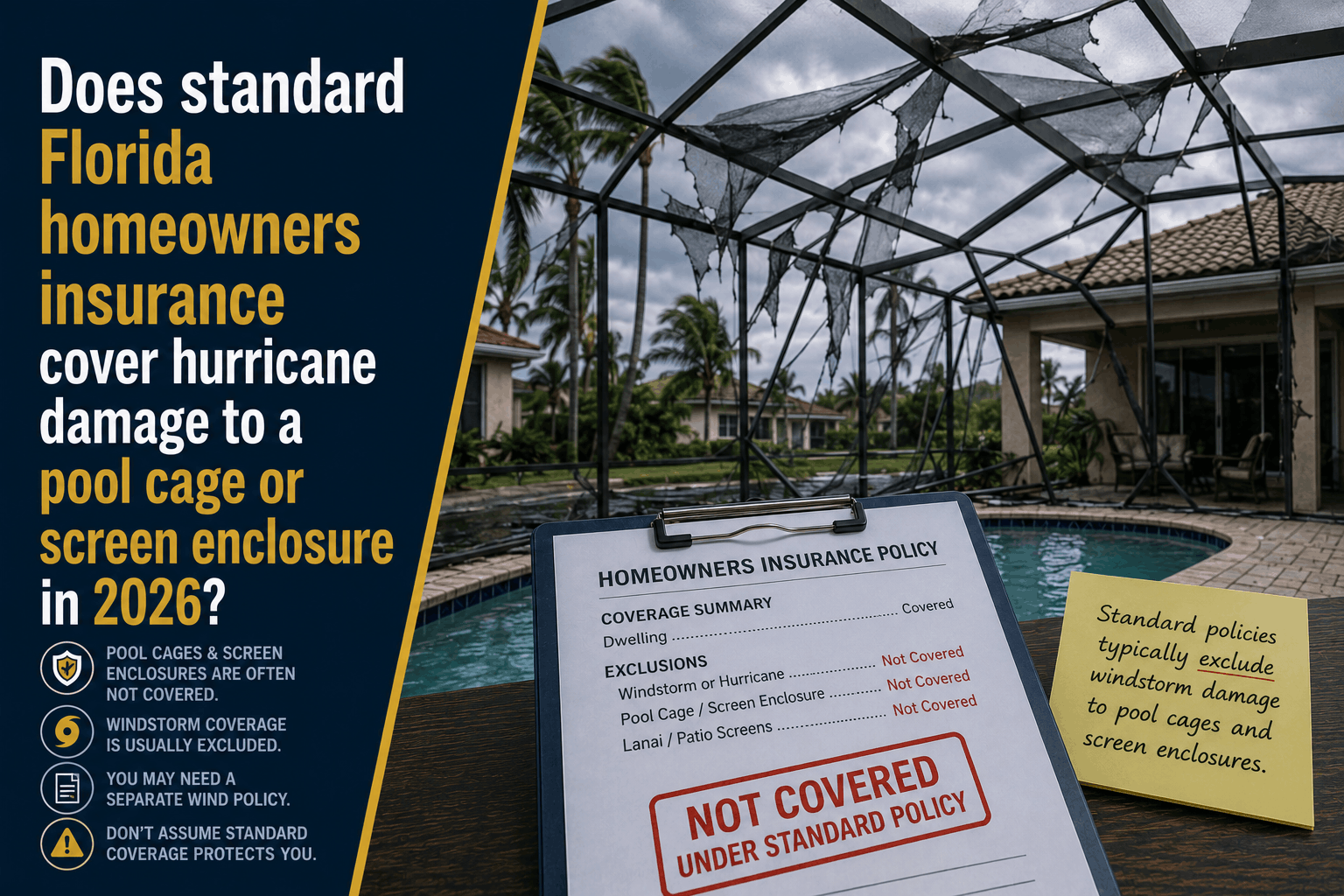

Does Florida Homeowners Insurance Cover a Pool Cage in 2026?

Learn about the "Lanai Loophole" in Florida. Discover why standard homeowners insurance excludes or limits hurricane damage to pool cages and screen enclosures.

Read More →