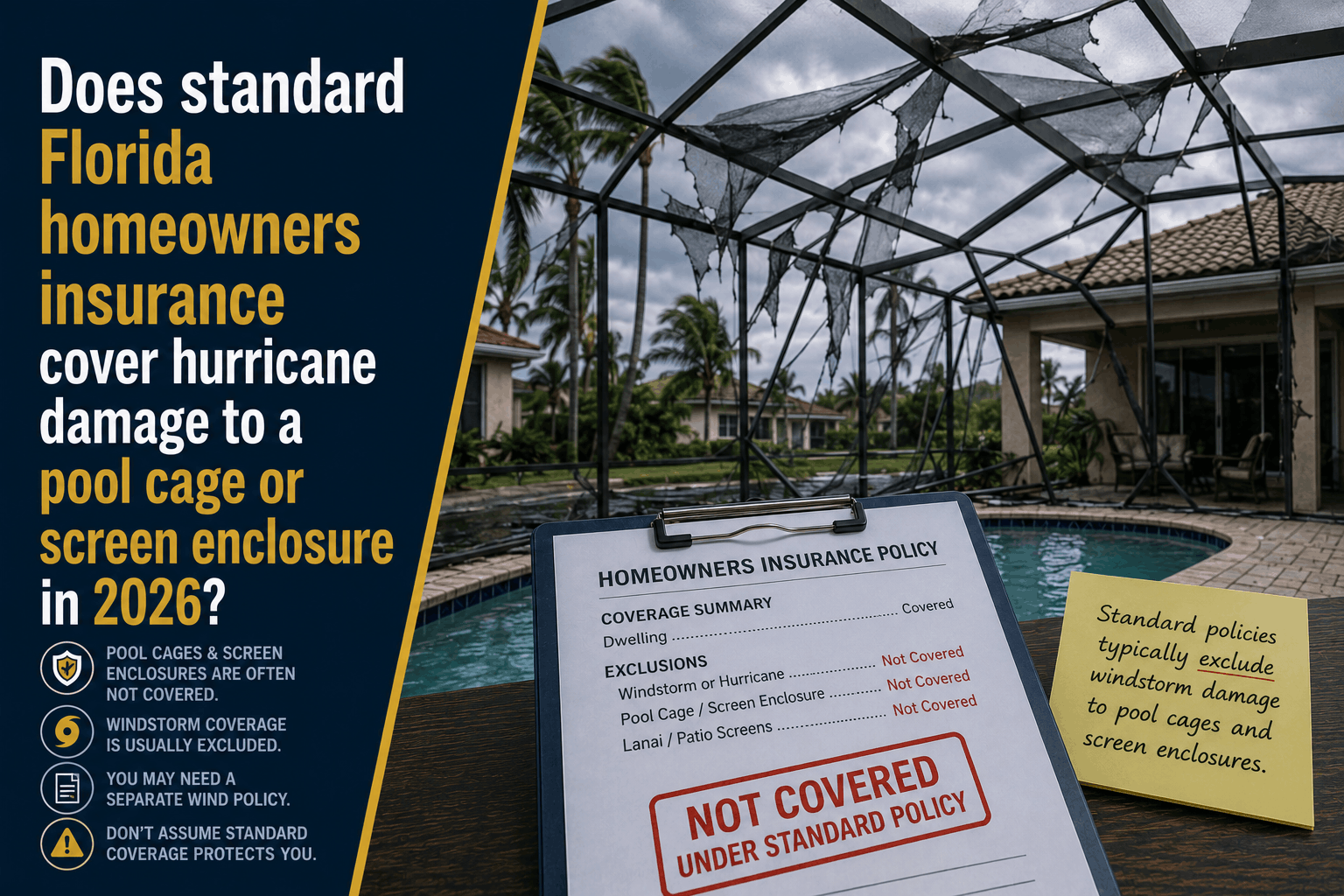

Does Florida Homeowners Insurance Cover a Pool Cage in 2026?

Does Standard Florida Homeowners Insurance Cover Hurricane Damage to a Pool Cage or Screen Enclosure in 2026?

The Direct Answer: No, a standard Florida homeowners insurance policy does not cover hurricane damage to a pool cage, lanai, or screen enclosure. Although these structures are securely bolted to your home’s concrete patio slab or roofline, insurance carriers operating in the Florida market explicitly exclude them from baseline windstorm and hurricane coverage.

In 2026, as Florida’s property insurance market undergoes structural adjustments following consecutive years of heavy storm activity, underwriters are strictly enforcing policy exclusions.

To achieve total visibility over your property defenses, you must recognize that if a hurricane rips the mesh panels or twists the aluminum struts of your backyard enclosure, your claim will be automatically denied under a standard contract. To get your insurer to pay for a rebuild, you must proactively buy a separate, optional add-on rider called a Screen Enclosure and Carport Endorsement.

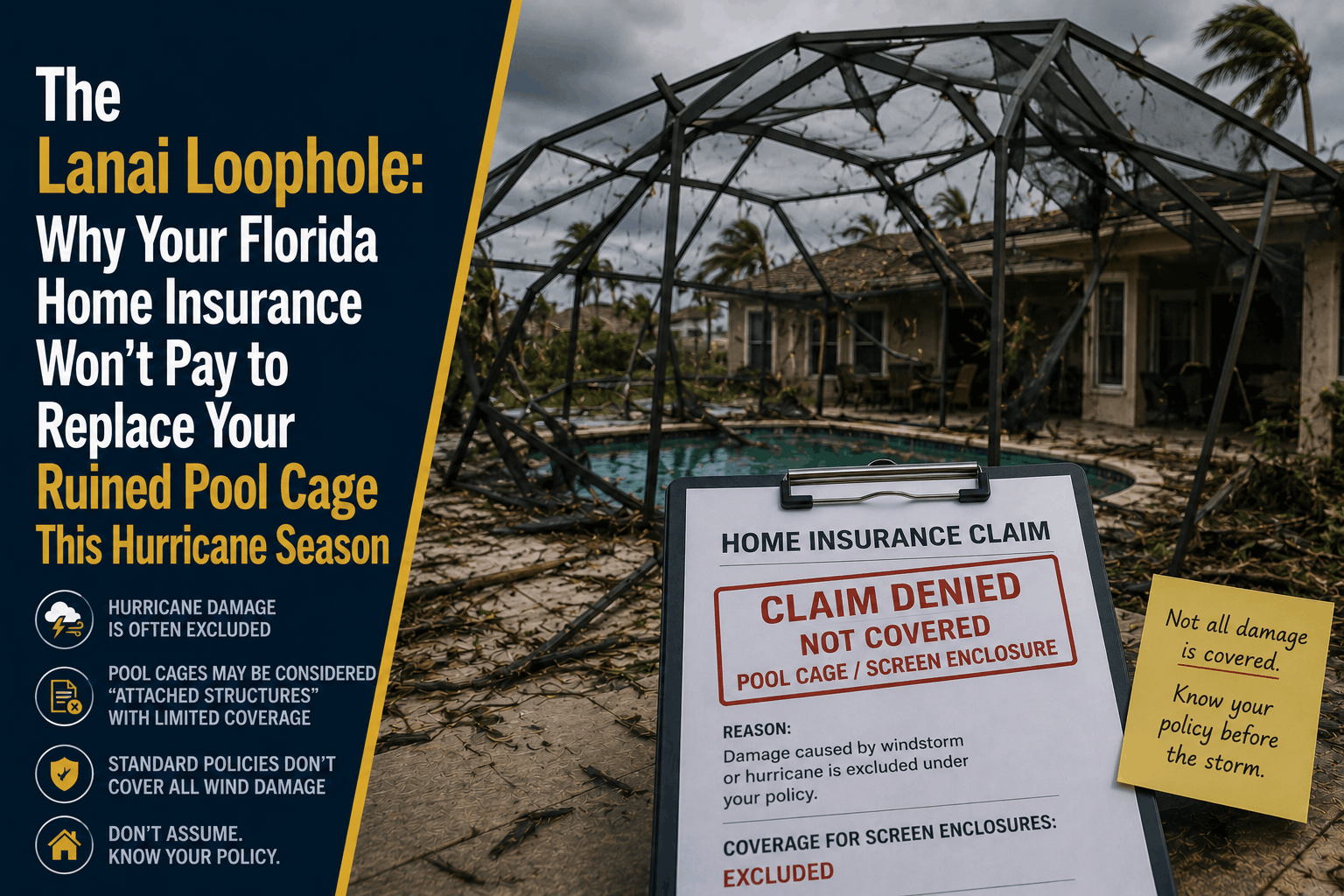

1. The "Lanai Loophole" & Attached Structures

A critical mistake many Florida property owners make is assuming that because a pool cage is physically attached to the house, it is protected under Coverage A (Dwelling) or Coverage B (Other Structures).

The contractual language splits your property into two clear, rigid zones:

[Structure: Main House & Primary Roof] ───> COVERED (Subject to your Hurricane Deductible).

[Structure: Aluminum Pool Cage / Lanai] ───> EXCLUDED by default under the Lanai Loophole.

The Wind Sail Exclusion: Florida insurance policy jackets explicitly state that open-air structures built with aluminum frames and covered by screen mesh, plastic, or fiberglass panels are not covered for windstorm losses. In a hurricane, a pool cage acts like a massive ship sail. The wind pressure builds up against the screens, snapping anchoring bolts and collapsing the metal cage. Because of this nearly 100% failure rate in major storms, carriers removed the exposure from standard policies to keep baseline premiums from skyrocketing.

2. Payout Scenarios: When is a Pool Cage Covered?

Even if you do not carry the optional hurricane rider, your screen enclosure may receive funding under highly specific, limited scenarios depending entirely on the proximate cause (the original peril) of the damage:

| Cause of the Loss | Covered by a Standard Policy? | How the Claim Settles |

|---|---|---|

| Hurricane / Named Storm Winds | NO | 100% Excluded. You must carry the specialized Screen Enclosure Hurricane Rider. |

| Fallen Tree (Everyday Event) | SOMETIMES | Covered by some carriers, but they will often pay to repair the aluminum frame only while completely excluding the screen mesh. |

| Lightning Strike / Fire | YES | Covered under standard standard "named perils" if a direct strike fries or twists the frame. |

3. The 2026 Rebuild Reality: A Severe Budget Killer

Leaving this coverage gap exposed before hurricane season peaks is a major financial risk. Due to construction labor shortages and material inflation across Florida, excavation and pool cage replacement costs have broken historical records:

- Debris Extraction & Cleanup: If a cage collapses directly into your pool, cutting the twisted metal structure apart, hauling it away, and clearing shredding mesh from your filtration pump costs between $2,500 and $4,500.

- Full Structural Replacement: Rebuilding a standard, single-story aluminum pool cage averages $12,000 to $25,000. Custom two-story designs or modern "panoramic view" enclosures frequently exceed $35,000.

How to Safely Secure Your Screen Enclosure

If you want to protect your outdoor living space and avoid funding a five-figure construction project out of pocket, you must structure your insurance portfolio using an expert blueprint:

Step 1: Formally Add a "Screen Enclosure & Carport Hurricane Endorsement"

Step 2: Select an Accurate Rebuild Limit Portfolio ($10,000 to $50,000)

Step 3: Verify the Deductible Rules (Percentage-Based vs. Flat Deductible)

=============================================================================

= Total Structural Protection for Aluminum Beams, Tension Cables, and Mesh

When you purchase the endorsement, your carrier allows you to establish a designated coverage limit—typically costing around $100 annually for every $10,000 of protection.

The most important detail to check with your independent agent is the deductible structure. You must confirm whether your pool cage claim will be tied to your main home's heavy Hurricane Deductible (which is calculated as 2% to 10% of your home's total insured value) or if the rider can operate under a clean, separate flat deductible of $500 or $1,000, saving you thousands of dollars upfront.

Why Working with an Independent Agency is Vital

Attempting to manage your coastal property risk through a faceless smartphone application or a generic corporate website leaves you completely vulnerable to the fine-print limitations of the "Lanai Loophole." At Walker Insurance Agency, we provide the data-driven visibility you need to fortify your property line.

The Walker Advantage:

- Endorsement Fine-Print Audits: We dissect your declarations page to confirm whether your screen frame, mesh material, or both are fully protected against tropical-force winds.

- Replacement Cost Accuracy: We match your lanai's cubic volume with actual local Stuart contractor labor rates so you never end up underinsured after a storm.

- Resurgent Market Matching: As the stabilizing Florida market introduces 20 brand-new private insurance carriers, we continuously shop your profile to locate providers offering the highest screen limits with the lowest out-of-pocket deductibles.

FAQ

1. If a hurricane blows my neighbor’s fence into my pool cage and destroys it, does their insurance pay?

No. Under Florida's unique insurance legal structure, hurricane and windstorm damage are classified as "Acts of God." Every property owner must file damages through their own respective policy lines. If you do not carry a specific screen enclosure endorsement, your claim will be denied. You cannot legally sue your neighbor for the damages unless you can prove their fence was structurally rotting, neglected, and documented as an active hazard before the storm arrived.

2. State-backed Citizens Insurance is my carrier. Do they cover my pool cage?

By default, no. Citizens Property Insurance Corporation explicitly excludes aluminum-framed screened enclosures, carports, and lanais from their standard dwelling and other structures lines. However, Citizens does offer an optional, thin endorsement to add a limited amount of screen coverage back into the policy. Because their internal limits are highly restrictive, homeowners with large pool cages are typically better served shopping the private carrier market.

3. What should I do to protect my pool cage if a Category 3 hurricane is tracking toward Stuart?

Never climb onto the aluminum frame during a storm warning. If your screen enclosure features engineered "hurricane release panels" or ground-level pop-out screen boundaries, remove them carefully before the high winds arrive. This allows the intense barometric pressure and wind gusts to flow cleanly through the structure rather than turning your entire pool cage into a giant sail, drastically minimizing the chances of a catastrophic structural collapse.

Insulate Your Coastal Wealth Before the Next Storm Tracker Updates

Your screen enclosure is a central part of your Florida lifestyle, but leaving its structural survival to a basic, un-endorsed homeowners policy is a gamble that can wipe out your emergency cash reserves in a single afternoon. True peace of mind means ensuring your written policy contract matches the physical layout of your backyard.

Don't let the next storm break your household budget. Contact Walker Insurance Agency today for a comprehensive hurricane risk audit. We provide the visibility you need to eliminate hidden exclusions, deploy high-limit screen riders, and protect your family's hard-earned wealth safely in Stuart.

[GET A FREE QUOTE TODAY]

Call us at +1-407-977-7100 or visit our office in Stuart, FL. Let us secure your property boundaries today.

Related Articles

The Lanai Loophole: Why Home Insurance Won't Fix Your Pool Cage

Discover how Florida’s strict "Lanai Loophole" can completely exclude or limit your pool cage and screen enclosure coverage this hurricane season.

Read More →

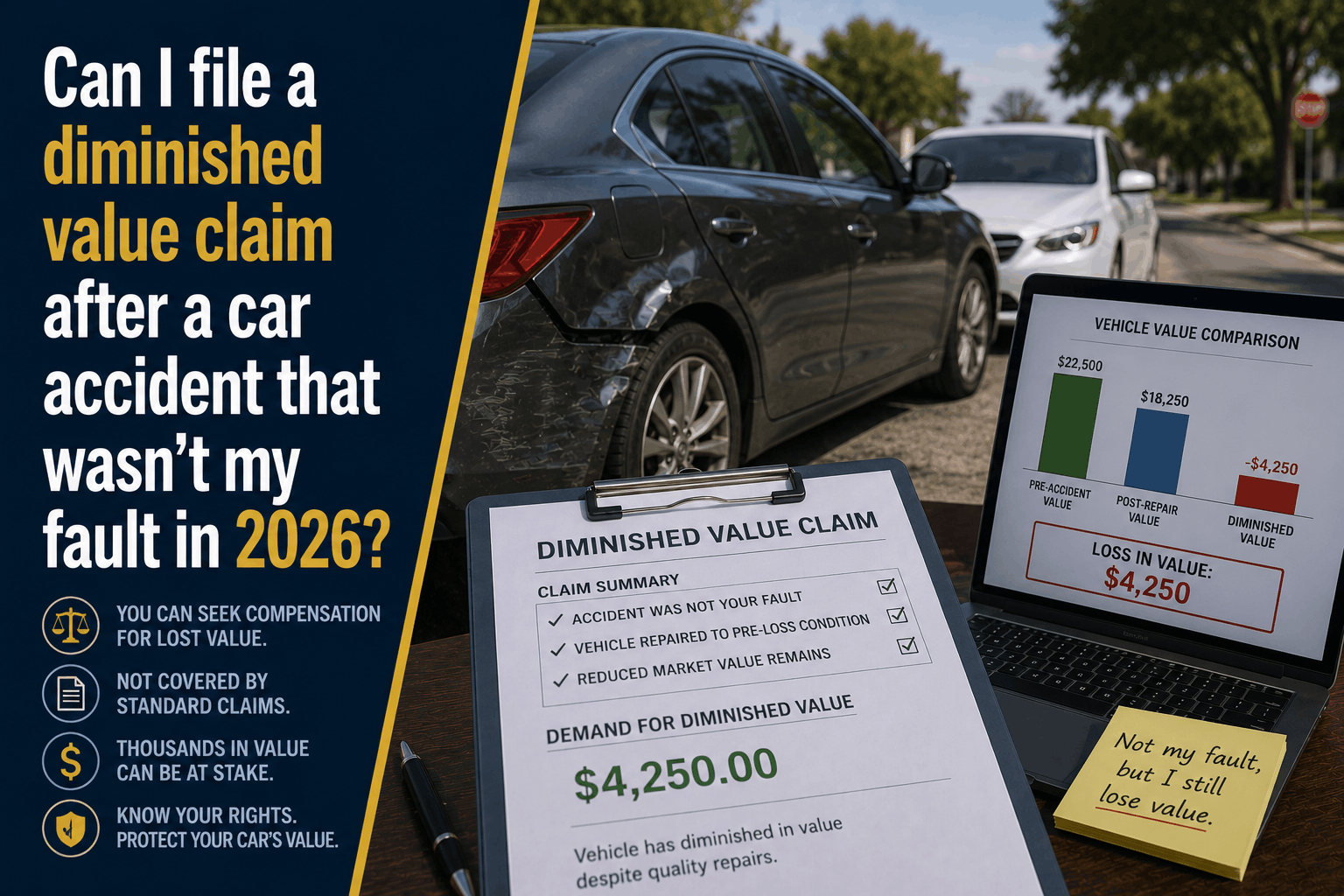

Can I File a Diminished Value Claim in 2026? (Not At-Fault Guide)

If you were involved in a car accident that wasn't your fault, discover how to file a Diminished Value claim to recover your vehicle's lost resale value.

Read More →

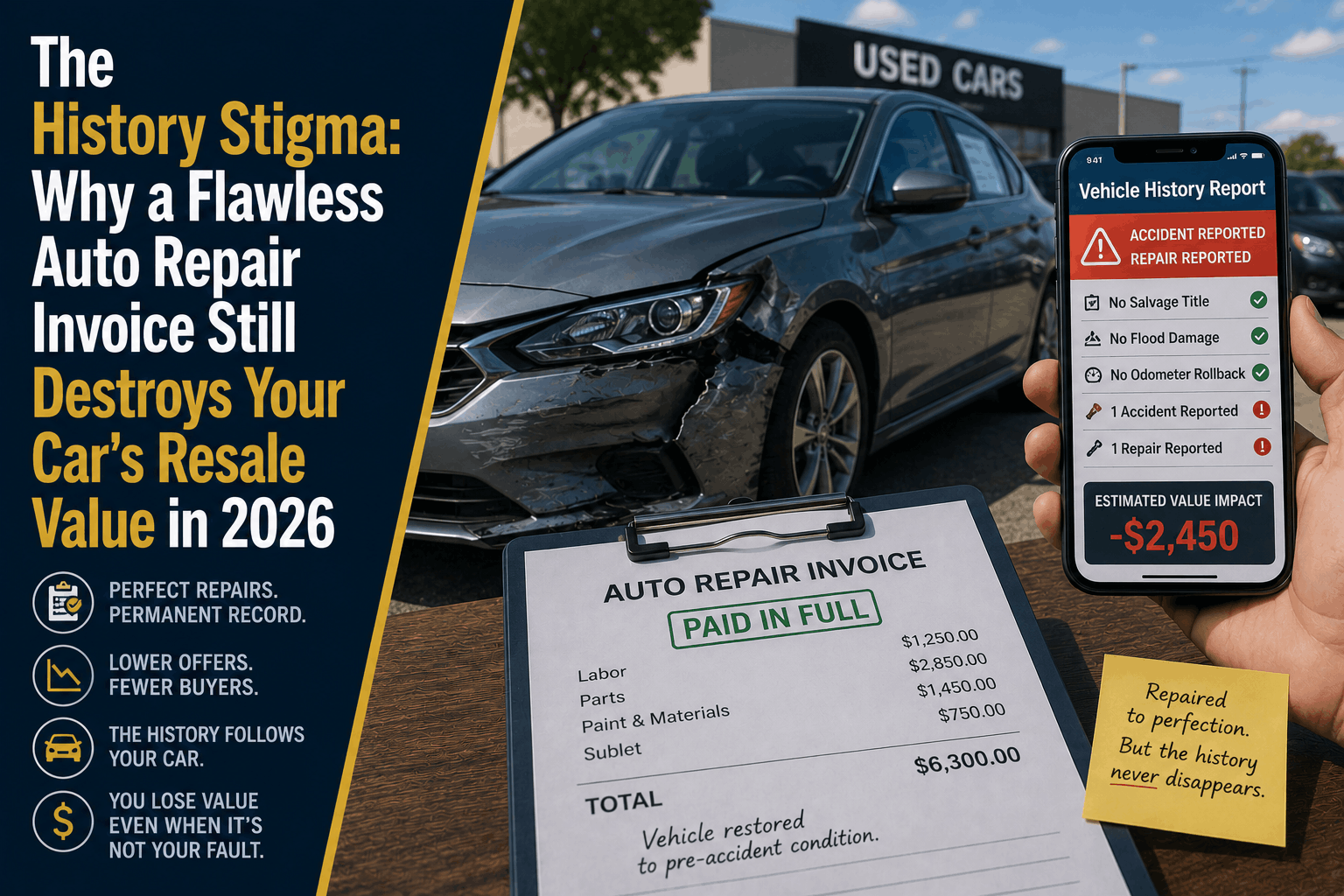

The History Stigma: Diminished Value Claims in 2026

Even a flawless repair can instantly wipe out 10% to 30% of your vehicle's resale value. Discover the history stigma and how to claim Diminished Value in 2026.

Read More →