The Lanai Loophole: Why Home Insurance Won't Fix Your Pool Cage

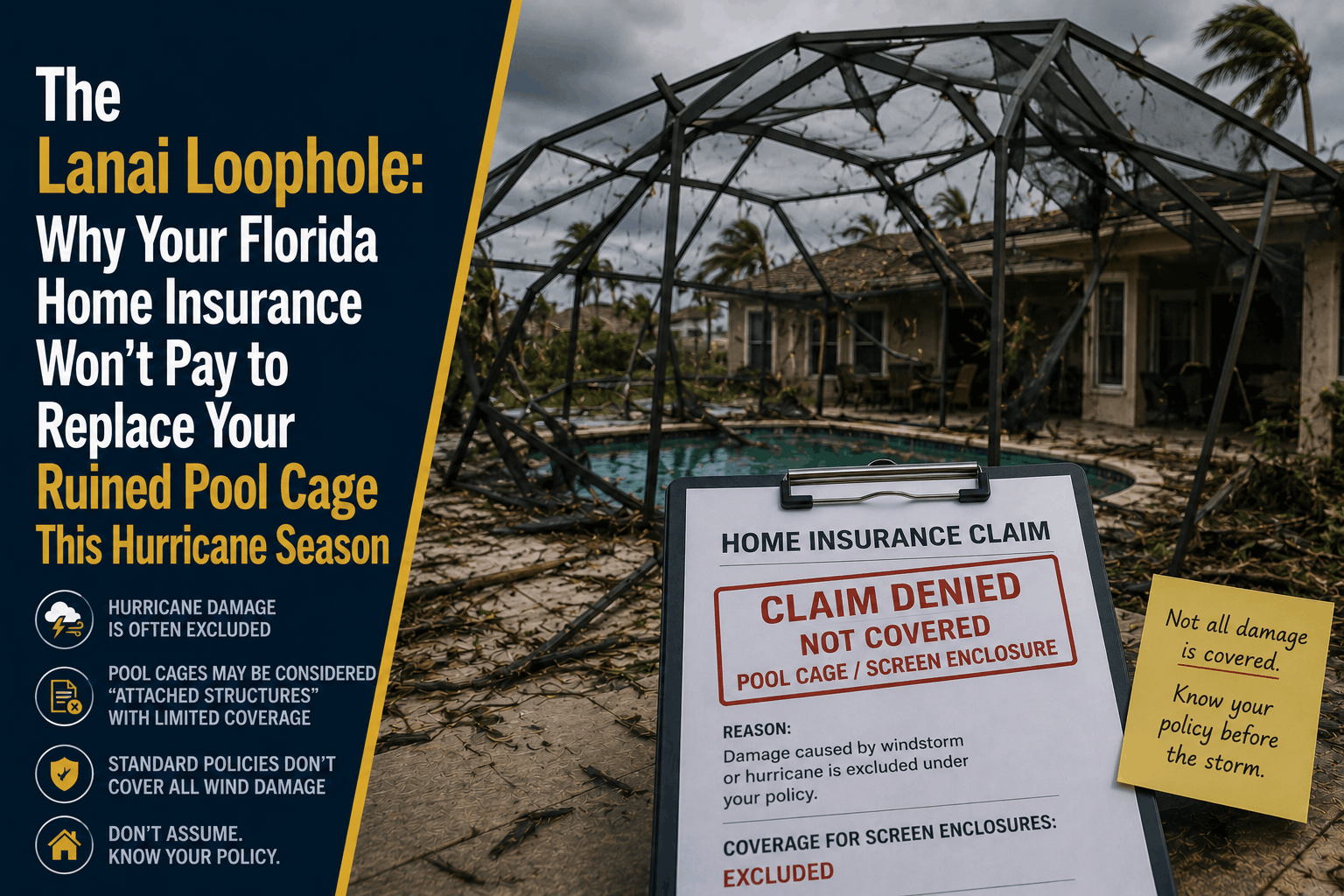

The Lanai Loophole: Why Your Florida Home Insurance Won't Pay to Replace Your Ruined Pool Cage This Hurricane Season

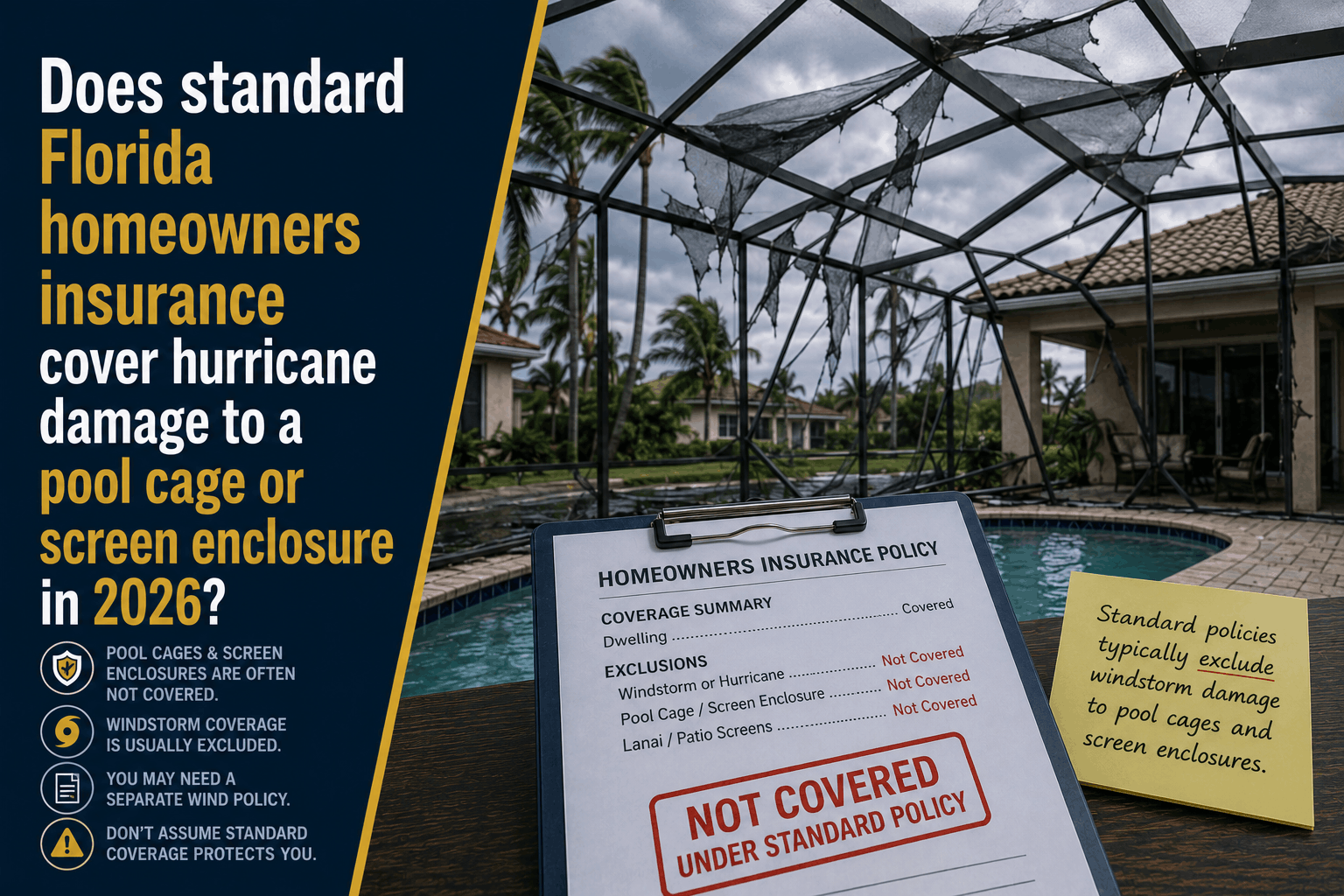

The Direct Answer: The devastating reason your insurance company will likely deny or severely underpay a claim for a twisted, torn, or flattened pool cage this hurricane season is a widespread contractual exclusion known as The Lanai Loophole. Under standard, off-the-shelf Florida homeowners insurance policies, screen enclosures, aluminum pool cages, and lanais are explicitly excluded from windstorm coverage.

In 2026, as the Florida property market undergoes rapid restructuring following years of intense storm activity, carriers are clamping down on external exposures. Unless you have explicitly paid for a separate, optional add-on endorsement specifically titled Screen Enclosure and Carport Coverage, you will be left entirely on your own to fund the replacement.

To achieve total visibility over your property defenses, you must accept that your main dwelling policy stops at your home’s sliding glass doors. The structural aluminum web over your pool is treated as an uninsured luxury exposure by default.

1. The Anatomy of a Lanai Exclusion

When a hurricane brings tropical-force wind gusts into your zip code, aluminum screen enclosures act like massive sails. The wind forces catch the nylon screening, creating immense pressure that twists aluminum struts, snaps anchoring bolts, and collapses the entire frame into the pool water.

If you submit this damage under a standard un-endorsed HO-3 or HO-5 policy, a claims adjuster will navigate directly to the "Property Not Covered" section of your policy jacket.

[Main House & Attached Roof] ───> CUBIERTO (Subject to Hurricane Deductible).

[Pool Cage / Screen Enclosure] ──> EXCLUDED entirely under the default Lanai Loophole.

The Structural Illusion: Many homeowners assume that because a pool cage is bolted directly to the concrete foundation slab of the house, it is automatically protected under Coverage A (Dwelling) or Coverage B (Other Structures). It is not. Florida insurance contracts specifically segregate screen enclosures, aluminum carports, awnings, and trellises into a non-covered classification to protect carriers from the nearly 100% destruction rate these structures face in major windstorms.

2. The 2026 Cost Reality: Why the Bill is a Budget-Killer

Allowing this gap to remain unaddressed exposes your family to skyrocketing modern construction and materials overhead. If a hurricane destroys your outdoor living area this season, the financial fallout is brutal:

- The Material Squeeze: Aluminum manufacturing and local labor inflation have driven the cost of a standard 2-story pool enclosure to an average of $12,000 to $28,000. Large, custom multi-angled panoramic lanais routinely cross the $40,000 mark.

- The Tearing and Debris Overhead: Before a new enclosure can even be engineered and permitted, you must pay out of pocket to have a specialty crew cut apart the twisted aluminum frame, fish the shredded screening out of your pool filtration pump, and haul the metal debris away—a process that averages $2,500 to $4,500 alone.

3. How to Safely Build a Pool Cage Shield

If your backyard oasis is sitting on a baseline contract with zero custom riders, your cash reserves are entirely vulnerable. At Walker Insurance Agency, we advise Florida property owners to secure their outdoor spaces using a precise, three-tier framework:

Step 1: Audit the Policy Jacket for active "Screen Enclosure Exclusions"

Step 2: Bind a Scheduled Screen Enclosure Rider (Select Limits: $10k to $50k)

Step 3: Verify the Deductible Structure (Is it subject to the heavy % Hurricane Cap?)

====================================================================================

= 100% Continuous Financial Restitution From Aluminum Frames to Nylon Mesh

Adding a dedicated Screen Enclosure and Carport Endorsement allows you to select a specific dollar limit (typically starting at $10,000 and climbing in increments of $5,000) dedicated strictly to rebuilding the structure.

However, you must look closely at how the deductible applies. Some carriers apply your standard, high-percentage Hurricane Deductible (2% to 10% of your home's total value) to this enclosure rider, while preferred carriers allow the rider to operate under a flat, manageable $500 or $1,000 deductible—saving you thousands of dollars before a single contractor is hired.

Why Working with an Independent Agency is Vital

Attempting to manage a complex coastal property asset through a faceless online application or automated digital broker ensures you will miss the critical regional riders needed to survive a hurricane. At Walker Insurance Agency, we provide the personalized, data-driven visibility you need to defend your land.

The Walker Advantage:

- Rider Scope Optimization: We accurately calculate the replacement cost of your specific lanai volume to ensure your endorsement limits match local Stuart construction labor rates.

- Carrier Stabilization Management: As the stabilizing 2026 Florida market introduces 20 brand-new private property companies to the state, we shop your profile to locate providers that offer flat-deductible screen riders at the lowest rate floors.

- Comprehensive Wind Mitigation Alignment: We link your pool cage asset protection with active home wind-mitigation credits, lowering your overall premium costs while expanding your total structural safety net.

FAQ

1. If a tree from my neighbor's yard falls and crushes my pool cage, does their insurance pay? No, rarely. Under Florida insurance guidelines, if an act of God (like hurricane winds) causes a neighbor's tree to fall onto your property, it is treated as your own windstorm event. You must file the claim through your own property policy. If you do not have a specific screen enclosure rider active, the claim will be denied, and you cannot legally force your neighbor's carrier to pay unless you can prove the tree was dead, rotting, and documented as a hazard before the storm.

2. Does a screen enclosure rider cover the cost of the screening, or just the aluminum metal frame? A top-tier endorsement covers the entire physical structure, including the aluminum framing members, the anchoring cables, and the nylon or fiberglass screening mesh. However, some ultra-low-cost policies carry a "Frame Only" clause that explicitly excludes the mesh fabric. We audit your fine print to ensure your mesh and frames are 100% unified under the coverage limits.

3. What should I do immediately to secure my pool cage if a major hurricane is tracking toward Stuart? Do not attempt to climb the structure to remove screens yourself. If your model features engineered "hurricane release panels" or pop-out screen sections, carefully remove them at ground level according to the manufacturer's manual. This allows heavy winds to flow clean through the structure rather than turning the lanai into a sail, significantly reducing the chances of a total structural collapse.

Insulate Your Outdoor Lifestyle Before the Storm Tracks West

Your pool cage is an essential component of your Florida lifestyle, but leaving it unprotected under a generic, off-the-shelf insurance contract is an administrative gamble that can instantly wipe out your emergency funds in a single stormy afternoon.

Expose your true policy protections today. Contact Walker Insurance Agency for a comprehensive 2026 property risk evaluation. We provide the visibility you need to eliminate hidden lanai loopholes, deploy high-limit screen riders, and protect your family's hard-earned wealth safely in Stuart.

[GET A FREE QUOTE TODAY]

Call us at +1-407-977-7100 or visit our office in Stuart, FL. Let us secure your property boundaries today.

Related Articles

Does Florida Homeowners Insurance Cover a Pool Cage in 2026?

Learn about the "Lanai Loophole" in Florida. Discover why standard homeowners insurance excludes or limits hurricane damage to pool cages and screen enclosures.

Read More →

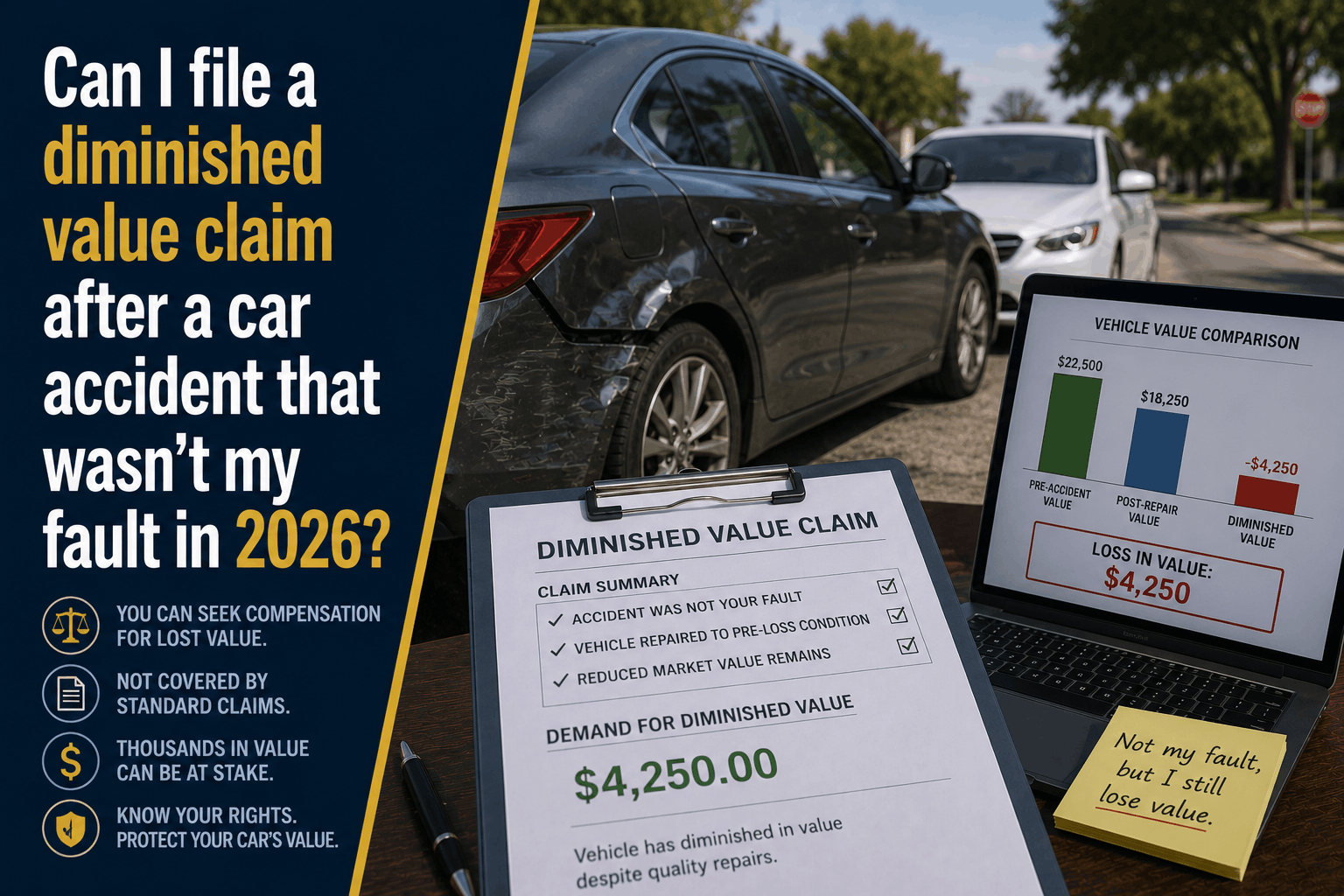

Can I File a Diminished Value Claim in 2026? (Not At-Fault Guide)

If you were involved in a car accident that wasn't your fault, discover how to file a Diminished Value claim to recover your vehicle's lost resale value.

Read More →

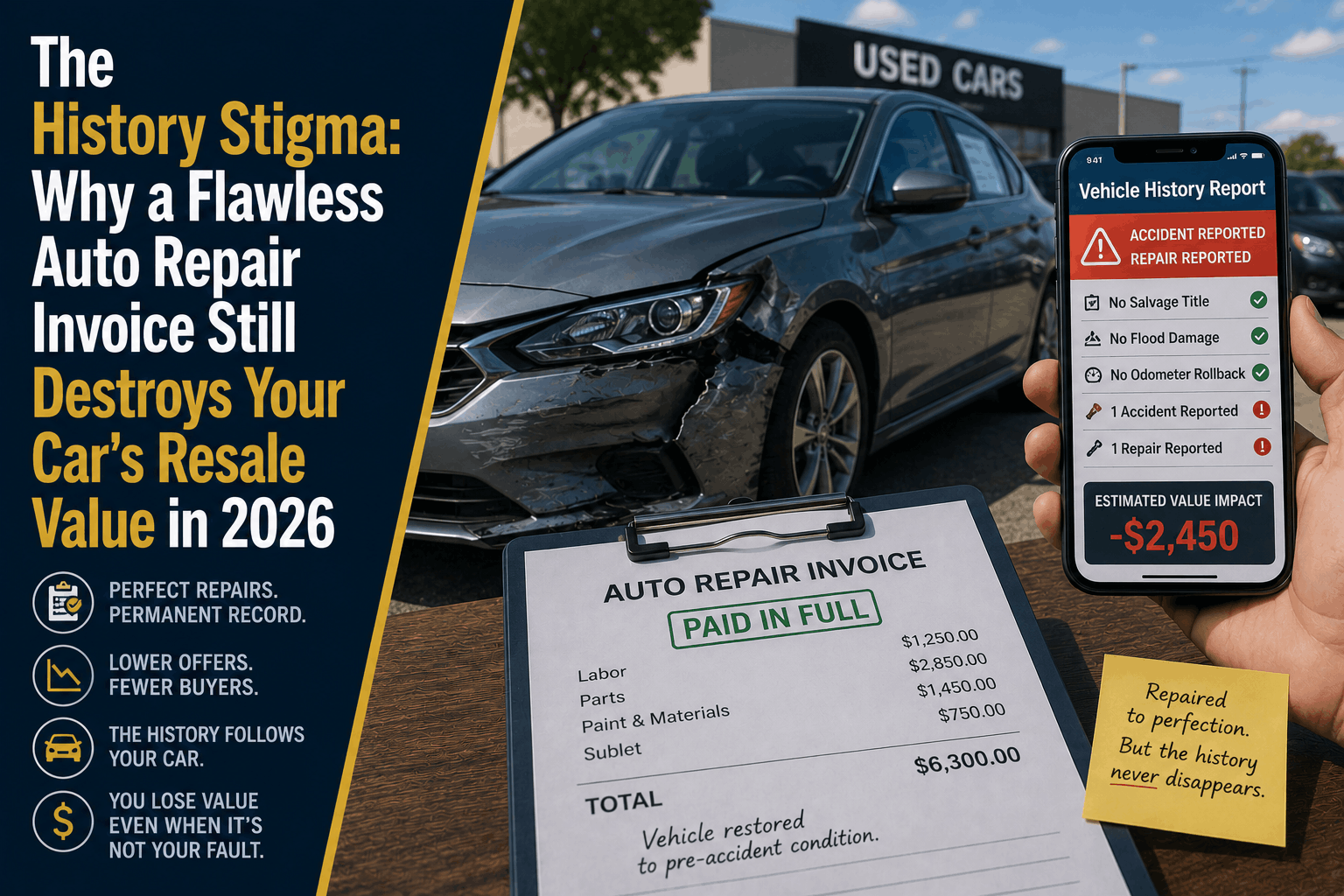

The History Stigma: Diminished Value Claims in 2026

Even a flawless repair can instantly wipe out 10% to 30% of your vehicle's resale value. Discover the history stigma and how to claim Diminished Value in 2026.

Read More →