The Code Compliance Trap: Why Home Insurance Won't Pay for Upgrades

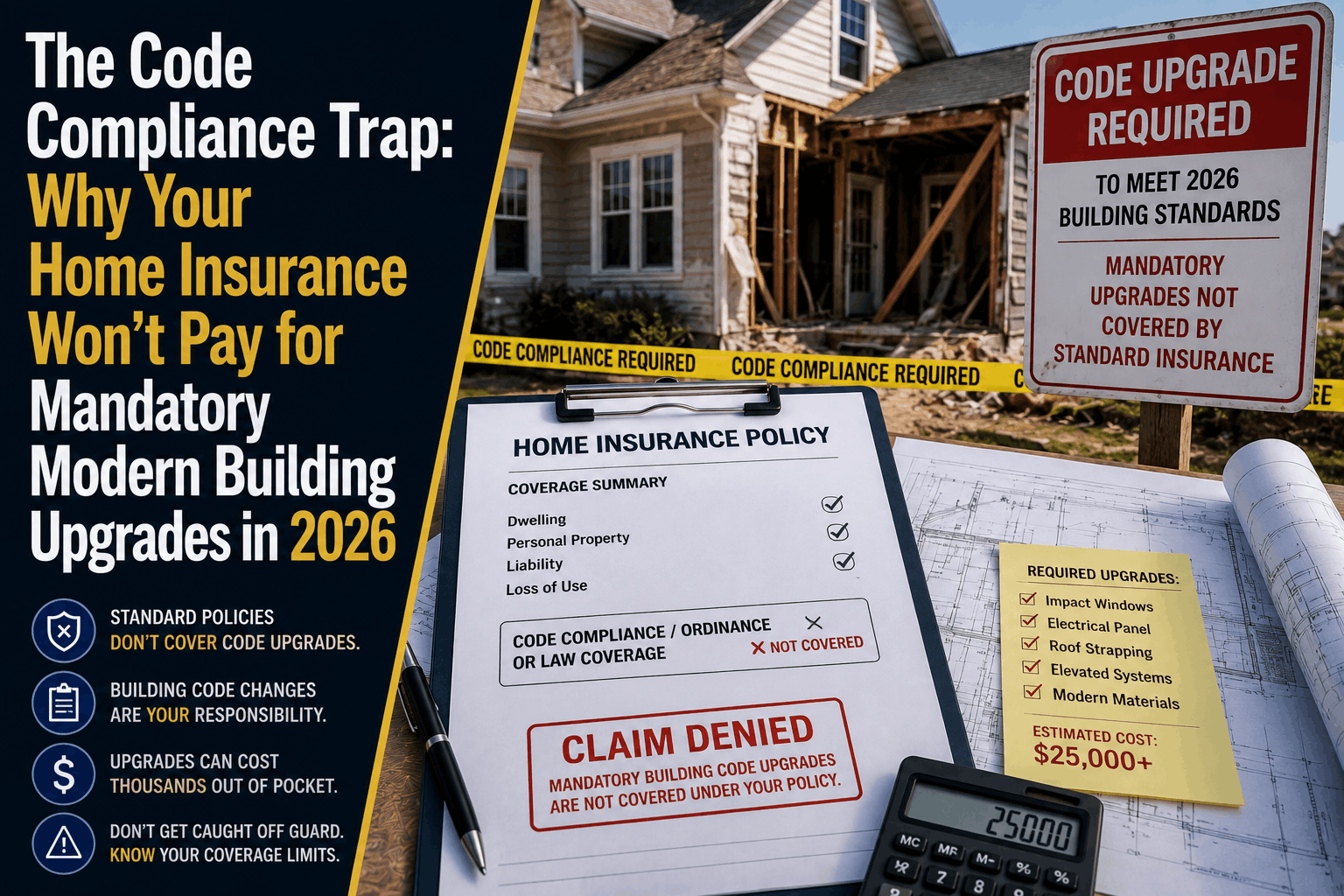

The Code Compliance Trap: Why Your Home Insurance Won't Pay for Mandatory Modern Building Upgrades in 2026

The Direct Answer: A standard homeowners insurance policy will completely refuse to pay for the extra costs required to bring your home up to modern building codes after a disaster. While your policy is contractually bound to pay to repair your home back to its original pre-loss condition, it operates under a strict "no betterment" rule. Insurance companies are only legally required to fix what was physically there before—not pay to make it better, safer, or legally compliant with updated local laws.

In 2026, this contractual boundary has become a massive financial trap for property owners. Building codes (such as the National Electrical Code and updated regional wind/wildfire structural mandates) change every few years.

If your home suffers a major fire or storm claim, local code enforcement agencies will not issue a reconstruction permit unless you upgrade your entire electrical panel, install modern fire sprinklers, or deploy impact-rated structural strapping. If you carry a standard, un-endorsed policy, 100% of these mandatory code upgrades must be paid entirely out of your own pocket.

1. The Anatomy of the Compliance Trap

The crisis usually unfolds after a partial loss, such as a localized kitchen fire or a tree smashing through a section of your roof. When the contractor submits the repair plans to the local municipal permit office, the city drops a major administrative bomb: because the home is being opened up for major repairs, the entire system must now be brought up to the current 2026 building code standards.

When you forward these mandatory code requirements to your insurance adjuster, they will point directly to the standard exclusions section of your policy jacket:

[Repair: Rebuilding to Original 1990 Specifications] ───> 100% COVERED by standard limits.

[Upgrade: Adding Mandatory 2026 Code Infrastructure] ───> 100% DENIED via Ordinance or Law Exclusion.

The 50% Demolition Trigger: Most municipalities enforce a strict "50% Rule." If a local inspector determines that a covered loss has damaged 50% or more of the market value of your home, local ordinances mandate that the undamaged portion of the house cannot remain as-is. The entire remaining structure must be completely demolished and rebuilt from scratch to comply with modern structural, energy, and flood codes. A standard property contract will pay nothing toward tearing down or rebuilding that undamaged half of the structure.

2. The High Cost of Modern Building Mandates

Allowing this gap to remain in your property portfolio leaves your cash reserves completely exposed to modern structural inflation. If you have to bring an older home up to modern compliance levels during a claim this year, these are the average costs you face out of pocket:

- The Electrical Overhaul: If you are repairing a wall and the city triggers an immediate upgrade to the latest National Electrical Code (NEC) standards—requiring arc-fault circuit interrupters (AFCIs) and a full panel upgrade to 200-amp service—the bill promedias $4,000 to $7,500.

- Wind-Hardening Roof Connections: In high-wind and coastal zones, modern codes require advanced roof-to-wall connections, such as heavy-duty hurricane straps and sealed roof decks (such as the IBHS FORTIFIED standard). Retrofitting an older roof deck during a repair adds $3,000 to $6,000 in un-covered structural labor.

- The Residential Fire Sprinkler Mandate: Many modern local zoning ordinances require the installation of residential fire sprinkler loops when executing major structural renovations. Retrofitting a pipe network through existing drywall structures routinely hits $8,000 to $15,000.

3. How to Defeat the Compliance Trap Safely

If your home is currently sitting on an unmodified baseline contract, your personal wealth is entirely vulnerable to local legislative changes. At Walker Insurance Agency, we help property owners eliminate this exposure using a precise, highly affordable policy endorsement:

Step 1: Run a Year-of-Construction Diagnostic on Your Property Limit

Step 2: Bind a Scheduled Ordinance or Law Endorsement (Select 10%, 25%, or 50%)

= 100% Seamless Coverage for Demolition, Debris Removal, and Modern Code Upgrades

To close this loophole, you must add an Ordinance or Law Endorsement to your homeowners policy. This rider completely overrides the standard exclusion and establishes a separate pocket of money calculated as a percentage of your primary Coverage A (Dwelling) limit.

For an average cost of just $50 to $80 per year, a 25% Ordinance or Law rider on a $400,000 home unlocks an extra $100,000 of dedicated clean funding. This cash steps in to pay for the mandatory demolition of undamaged structures, the clearing of code-enforced debris, and the high cost of modern electrical, plumbing, and structural enhancements required to secure your city certificate of occupancy.

Why Working with an Independent Agency is Vital

Attempting to manage your primary residential asset through a generic smartphone application ensures you will miss the critical regional riders needed to survive local zoning updates. At Walker Insurance Agency, we provide the data-driven visibility you need to defend your property line.

The Walker Advantage:

- Chronological Gap Analysis: We audit the age of your property against current municipal code sets to determine if you require a basic 10% rider or a maximum 50% structural endorsement.

- Loss-of-Use Synchronization: We ensure your Loss of Use (Coverage D) limits are expanded, protecting your family with hotel and relocation funding while code-enforced construction delays extend your repair timeline.

- Resurgent Market Matching: As the stabilizing property market introduces brand-new private insurance carriers, we continuously match your profile with companies that automatically include high-limit code upgrades within their preferred policy tiers in Stuart.

FAQ

1. If my home is relatively new, do I still need Ordinance or Law coverage? Yes. While newer homes (built within the last 3 to 5 years) are closer to current code compliance frameworks, building ordinances do not move as a single unit. Structural, electrical, and energy-efficiency standards update on different cycles. Even a home built in 2022 can face substantial, unexpected compliance costs if a claim triggers the latest electrical or insulation mandates.

2. Can I use my standard replacement cost coverage to pay for code upgrades? No. Even if your policy features "Extended Replacement Cost" (which adds an extra 20% to 50% to your dwelling limit), that extended cash is strictly reserved to cover standard material and labor inflation to rebuild your original floor plan. It cannot legally be diverted to fund structural code modifications or building upgrades unless you carry the specific Ordinance or Law endorsement.

3. What should I do immediately if a local building inspector halts my repair project for code updates? Do not authorize the contractor to execute the code modifications until you notify your agent. Request that the city building inspector issue a formal, written citation specifying the exact code section violation and detailing the mandatory upgrades required to secure the permit. Forward this official city document directly to your independent agent; this paperwork serves as the primary verification needed to instantly activate your endorsement funds.

Insulate Your Savings From an Administrative Crisis Today

A property disaster is stressful enough, but discovering that local city building codes will force you to spend thousands of dollars of your own savings just to get a permit to rebuild is a financial crisis you can easily prevent. True peace of mind requires aligning your insurance contract with the legislative reality of your local municipality.

Verify your building code protection before a disaster strikes. Contact Walker Insurance Agency today for a comprehensive property coverage audit. We provide the visibility you need to eliminate hidden code loopholes, deploy high-limit compliance riders, and protect your hard-earned wealth safely in Stuart.

[GET A FREE QUOTE TODAY]

Call us at +1-407-977-7100 or visit our office in Stuart, FL. Let us secure your property boundaries today.

Related Articles

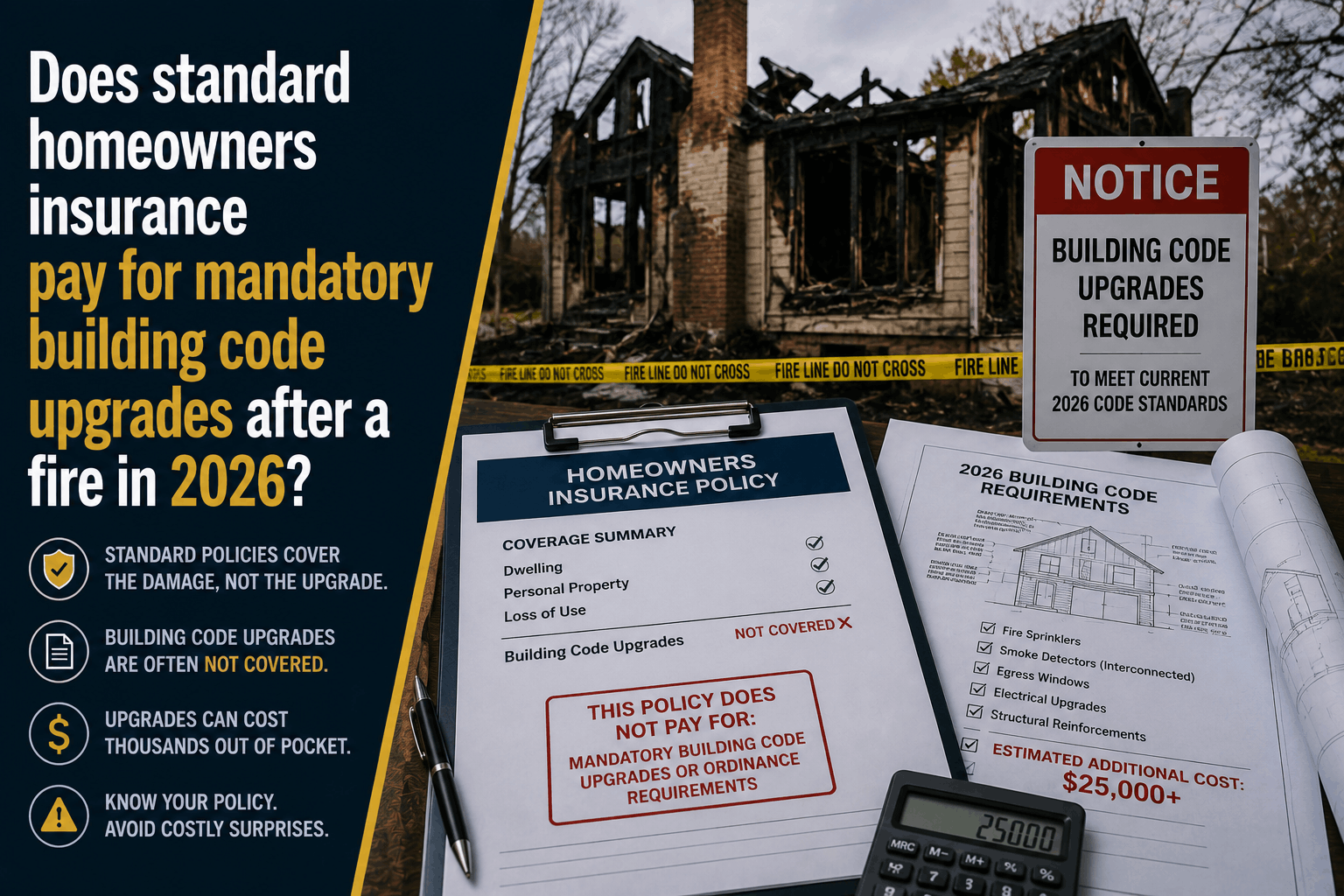

Does Homeowners Insurance Pay for Code Upgrades After a Fire?

A standard home insurance policy won't cover mandatory building code upgrades after a fire. Learn about the Ordinance or Law trap and how to protect your home.

Read More →

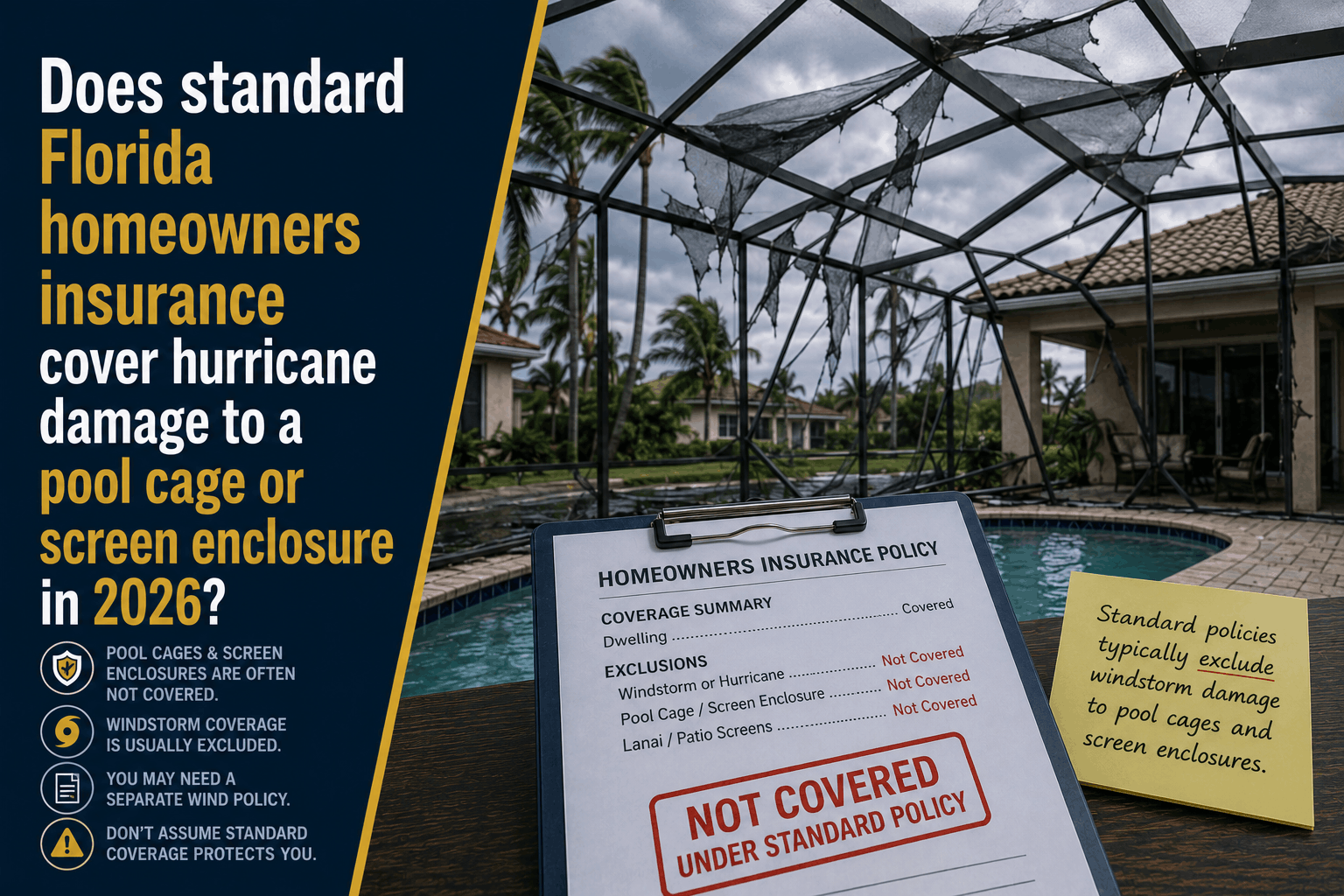

Does Florida Homeowners Insurance Cover a Pool Cage in 2026?

Learn about the "Lanai Loophole" in Florida. Discover why standard homeowners insurance excludes or limits hurricane damage to pool cages and screen enclosures.

Read More →

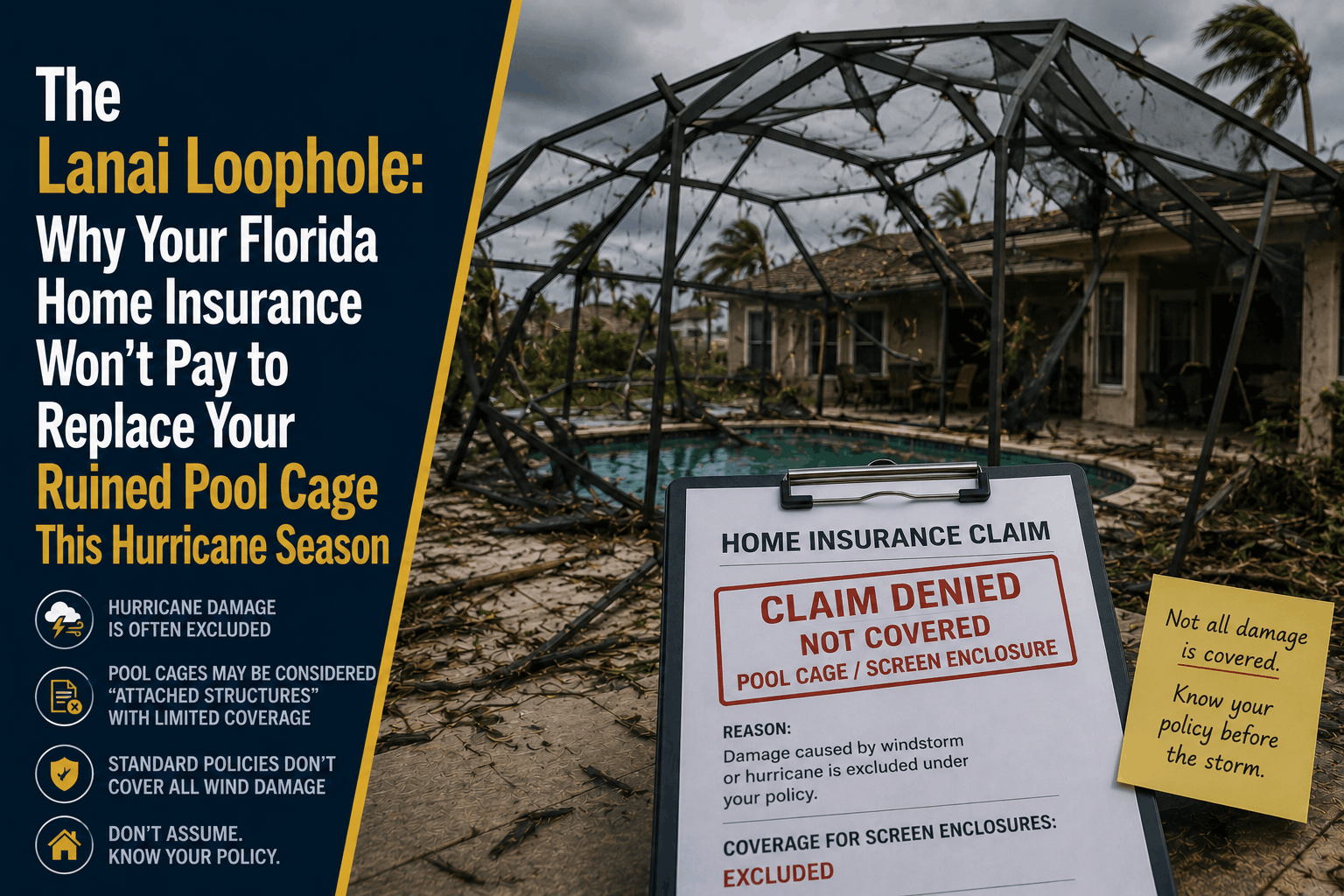

The Lanai Loophole: Why Home Insurance Won't Fix Your Pool Cage

Discover how Florida’s strict "Lanai Loophole" can completely exclude or limit your pool cage and screen enclosure coverage this hurricane season.

Read More →