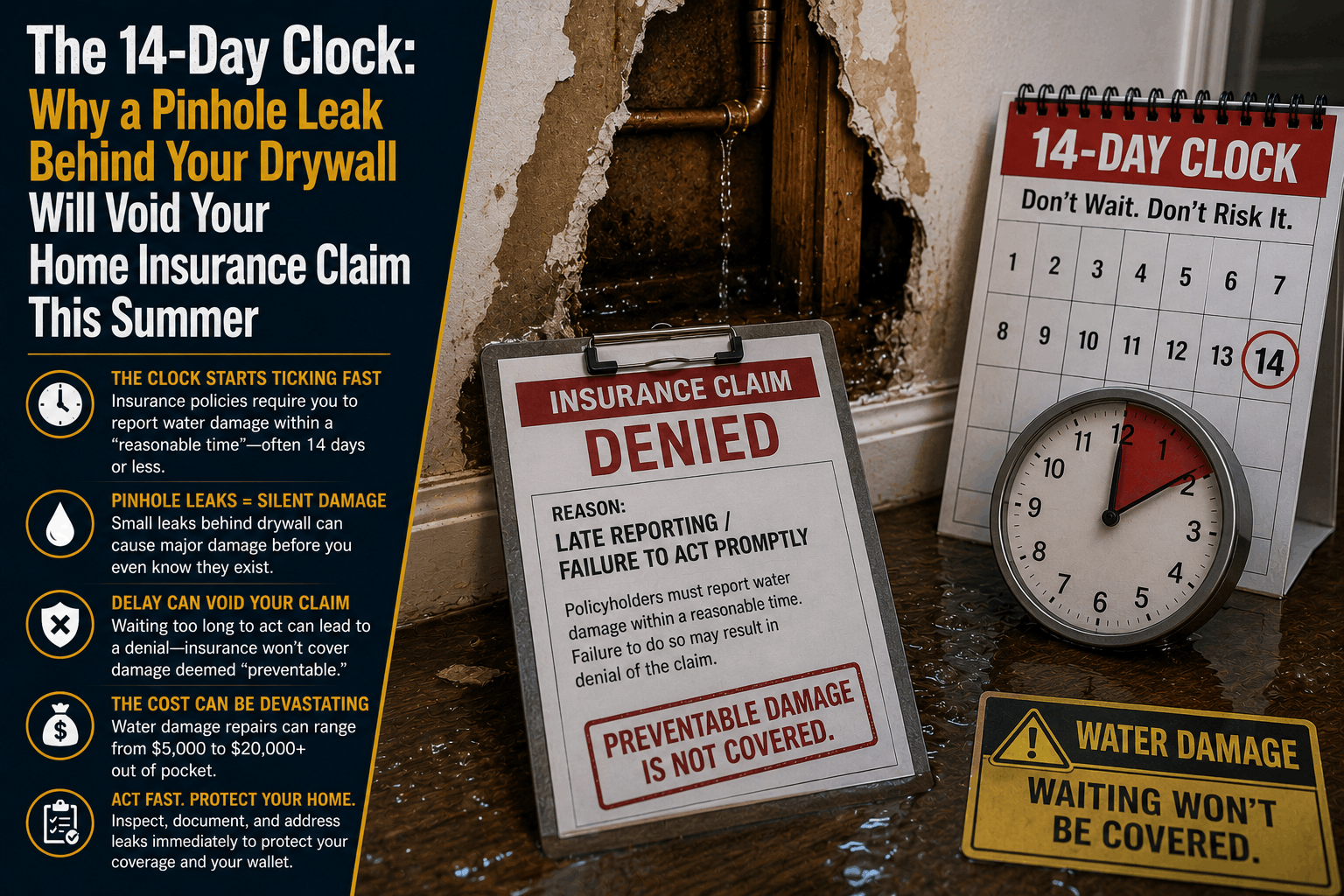

The 14-Day Clock: How a Pinhole Leak Voids Home Insurance

The 14-Day Clock: Why a Pinhole Leak Behind Your Drywall Will Void Your Home Insurance Claim This Summer

The Direct Answer: The devastating reason your insurance company will completely deny a water damage claim caused by a tiny pinhole leak behind your drywall this summer is the 14-day constant seepage exclusion. While standard homeowners insurance is contractually designed to cover sudden and accidental water bursts (like a washing machine hose snapping open), it explicitly excludes any water damage that occurs over a prolonged period.

In 2026, carrier claims adjusters are enforcing this boundary with absolute rigidity. Under standard policy language, if a copper or PEX pipe behind your wall develops a microscopic pinhole leak that drips quietly for 14 calendar days or longer before you notice the bubbling paint or mold, the entire claim is legally voided.

To achieve total visibility over your property defenses, you must accept that the insurance contract does not care when you discovered the leak; it only cares when the water started dripping.

1. The Summer Pressure Cooker: The Anatomy of a Pinhole Leak

Pinhole leaks behind drywall peak during the hot summer months due to a perfect storm of environmental and mechanical factors unique to the season:

- The Humidity and Thermal Expansion Squeeze: Intense summer heat causes structural framing and plumbing lines to expand and contract. This subtle shifting forces pipes to rub continuously against metal brackets or wooden studs, wearing down the outer wall of the pipe until a microscopic hole fractures open.

- The HVAC Condensate Backlog: Summer forces air conditioning units to run around the clock. If an AC condensate drain line buried inside your wall bottlenecks due to algae buildup, it will sweat or drip micro-amounts of water continuously into the insulation, mimicking a plumbing leak and ticking down your 14-day contractual clock.

- The Chemical Pit Factor: High summer water demand changes the velocity and chemical balance of municipal water treatments. Pitting corrosion—a localized chemical reaction that eats tiny pits into the interior walls of copper piping—accelerates rapidly in warmer water temperatures, punching out pinholes from the inside out.

2. The Claims Forensic Trap: How Adjusters Count the Days

Many property owners assume that if they file a claim the exact same day they spot a damp patch on their drywall, the claim is safe. However, modern insurance adjusters utilize advanced forensic tools to determine the exact timeline of the moisture:

[Sudden Pipe Exploded: 1 Day Ago] ──> 100% COVERED under standard policy lines.

[Micro-Drip Seepage: >14 Days Ago] ──> 100% DENIED entirely under the seepage clause.

The Forensic Blueprint: Adjusters do not rely on guesswork. When they inspect a wall leak, they look for structural telltales. If the drywall displays deep rotting, structural wood decay, black mold colonization, or rusted framing nails, these physical characteristics mathematically prove the moisture has been present for weeks or months. The carrier will invoke the exclusion and deny the entire claim on the grounds of chronic, un-remedied seepage.

3. The Multi-Thousand Dollar Fallout: Mold and Structural Limits

If your claim is discarded under the 14-day seepage exclusion, you are left holding the bill for an incredibly destructive repair cycle.

Because summer heat accelerates fungal growth, a hidden drip will quickly transform into a severe toxic biohazard:

- The Mold Cap Exclusion: Even if you manage to prove a leak happened within the 14-day window, standard Florida home insurance policies carry a strict, separate statutory cap on mold remediation—typically limited to just $10,000. If toxic mold spreads through your home's central HVAC ductwork from a wall cavity, professional remediation can easily skyrocket to $30,000+, leaving you to pay the difference out of pocket.

- The Drywall Tear-Down Overhead: Fixing a pinhole leak is cheap; fixing the collateral damage is not. In 2026, contractor labor inflation means cutting open walls, drying the interior structural studs, replacing insulation, hanging new drywall, matching textures, and repainting room-to-room averages $8,000 to $15,000 per incident.

How to Defeat the 14-Day Clock Safely

Allowing your property asset to sit on autopilot without tracking your internal infrastructure means your entire savings account is exposed to a microscopic droplet of water.

At Walker Insurance Agency, we advise property owners to protect their wealth using a proactive, dual-layer shield:

Step 1: Install Smart Automatic Water Shut-Off Valves (Mechanical Defense)

Step 2: Add a Hidden Seepage / Continuous Leak Rider (Contractual Defense)

=============================================================================

= Complete Eradication of the 14-Day Exclusion Loophole Above and Below Ground

- The Mechanical Shield: Deploying smart leak detectors (such as Moen Flo or LeakSmart) onto your main water line creates an automated defense. These systems continuously monitor micro-changes in water pressure. If a pinhole leak opens behind your drywall and drips even a few ounces of water, the system detects the pressure anomaly, sends an alert to your smartphone, and automatically shuts off your home's main water valve within minutes.

- The Contractual Shield: Ask your independent agent about adding a Hidden Seepage or Continuous Leak Endorsement. This optional rider explicitly overrides the standard 14-day exclusion, providing coverage for leaks that are completely concealed behind walls, under concrete slabs, or beneath flooring panels, even if they have been dripping undetected for months.

Why Working with an Independent Agency is Vital

Attempting to manage a complex property asset through a generic smartphone application or automated online portal ensures you will miss the critical riders needed to survive hidden plumbing emergencies. At Walker Insurance Agency, we provide the data-driven visibility you need to insulate your home.

The Walker Advantage:

- Endorsement Portfolio Audits: We meticulously read your policy jacket to identify hidden seepage limitations and fortify your contract with specialty hidden water riders before a claim occurs.

- Mitigation Credit Structuring: We ensure that installing state-of-the-art smart leak shut-off valves legally forces your carrier to apply premium discount credits to your account.

- Market Stabilization Shopping: As the 2026 Florida market stabilizes with 20 brand-new private property companies entering the state, we continually shop your profile to secure the highest-limit property riders at the absolute lowest available premium floors in Stuart.

FAQ

1. Does my standard home insurance cover the plumber's bill to fix the pinhole leak? No, never. Even if the claim is fully approved because the leak was sudden, standard property insurance is strictly designed to pay for the consequential physical damage caused by the water—such as ruined drywall, insulation, and warped flooring. The actual physical repair to the copper or PEX pipe itself is considered basic homeowner maintenance and must be paid for out of pocket.

2. What if a pinhole leak happens while my home is vacant during summer vacation? If your home is left vacant for more than 30 or 60 consecutive days without notifying your carrier, your entire water damage coverage line can be completely suspended under standard Vacancy Exclusions. If you leave for the summer, you should always shut off your home's main water valve at the meter and ensure your independent agent logs a seasonal occupancy rider on your account.

3. What is the fastest way to check for a hidden pinhole leak without tearing down walls? Go to your main water meter box at the edge of your property line and ensure all faucets and appliances inside your house are completely turned off. Look closely at the meter's face; if the small, triangular low-flow indicator dial is spinning, or if the digital read-out numbers are climbing even slightly, water is moving through your system—proving you have an active, hidden leak somewhere inside your infrastructure.

Insulate Your Savings from a Hidden Water Disaster Today

A pinhole leak is quiet, entirely invisible, and mathematically weaponized to void your insurance policy if left unresolved for two weeks. Relying on an ordinary, unmodified property contract to cover a hidden, long-term drip is an administrative gamble that can instantly wipe out thousands of dollars from your family's savings account.

Verify your water riders before a drip breaks your budget. Contact Walker Insurance Agency today for a comprehensive property coverage review. We provide the visibility you need to eliminate hidden seepage loopholes, deploy smart shut-off defenses, and protect your family's lifestyle safely in Stuart.

[GET A FREE QUOTE TODAY]

Call us at +1-407-977-7100 or visit our office in Stuart, FL. Let us secure your home boundary lines today.

Related Articles

Does Homeowners Insurance Cover Trampoline Injuries? (2026 Rules)

Putting up a backyard trampoline? Discover how 2026 home insurance policies handle trampoline injuries and why the attractive nuisance rule can trigger a denial.

Read More →

The Summer Playground Trap: How Undeclared Trampolines Void Insurance

Putting up a backyard trampoline this summer? Learn why failing to declare it to your homeowners insurance can lead to total liability claims denial in 2026.

Read More →

Does Homeowners Insurance Cover Mold & Slow Wall Leaks? (2026 Rules)

Think a hidden pipe drip is covered by insurance? Discover how Florida’s strict 14-day constant seepage rule and mold caps apply to slow leaks inside walls.

Read More →