The $10,000 Wind-Mitigation Hack: Florida's 2026 MSFH Grant Guide

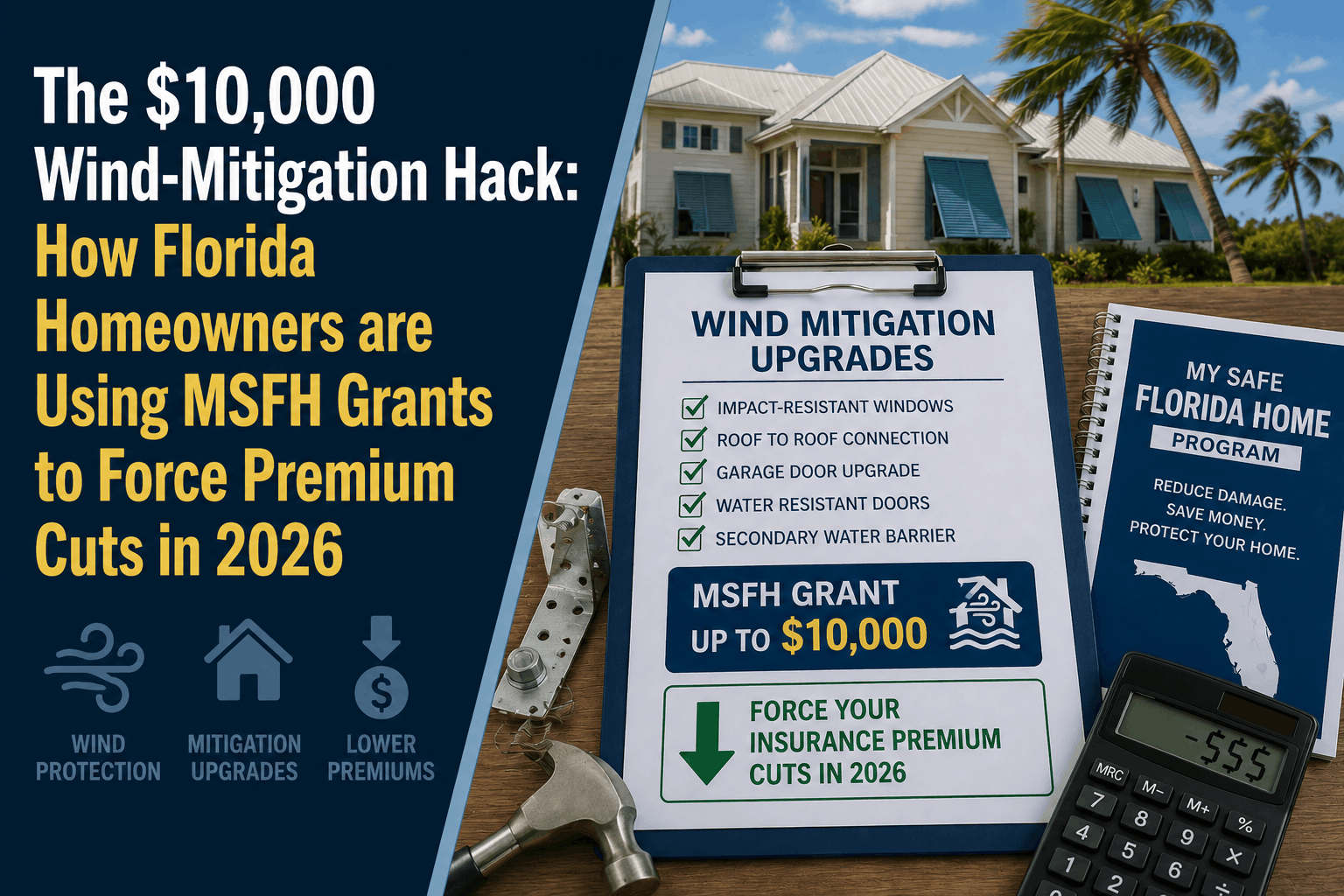

The $10,000 Wind-Mitigation Hack: How Florida Homeowners are Using MSFH Grants to Force Premium Cuts in 2026

The Direct Answer: The "$10,000 wind-mitigation hack" refers to a highly strategic deployment of the My Safe Florida Home (MSFH) grant program to legally force insurance companies to lower your property premiums. Under Florida Statute 627.711, insurers are legally mandated to offer permanent premium credits for wind-mitigation features. By utilizing the state’s 2-for-1 matching grant to secure up to $10,000 in state funds (or 100% free for low-income households), homeowners are upgrading their roofs and opening protections.

In May 2026, the data proves this strategy works: homeowners who complete the MSFH cycle are forcing private insurers to slice an average of $981 per year off their homeowners insurance premiums.

To achieve total visibility over your property expenses, you must understand that this isn't just about making your home safer—it is a financial maneuver. You are using state money to force a private corporation to lower your fixed cost of living.

1. The Legally Enforced Hack: Statute 627.711

Many homeowners assume insurance companies offer wind-mitigation discounts out of goodwill. They do not.

- The Mandate: Florida law dictates that insurance companies must submit a rating plan to the state that includes actuarially sound discounts for wind-hardened homes.

- The Power Dynamic: When you submit a certified Wind Mitigation Inspection Form (OIR-B1-1802) showing upgraded features, the insurance company's computer system is legally forced to apply the corresponding discount. They have zero underwriting discretion to deny the credit if the construction meets the code.

2. Sizing the Project: The $15,000 "Sweet Spot"

To maximize the 2026 grant structure, standard moderate-income homeowners (earning below 120% of their county’s Area Median Income) are utilizing precise project math:

[Your Contribution: $5,000] + [State Grant Match: $10,000]

= $15,000 Total Mitigation Power (The Sweet Spot)

- The Matching Rule: The state pays $2 for every $1 you spend. If you size your project exactly at $15,000, you pull the maximum $10,000 out of the state repository while only spending $5,000 of your own money.

- The Low-Income Waiver: If your household income is at or below 80% of the county median, the matching requirement is waived entirely. The state pays 100% of the cost up to $10,000, meaning your out-of-pocket cost is exactly $0.

3. The Big Three Premium Slicers

You cannot use MSFH funds for cosmetic home additions. To force the largest insurance cuts, you must target the specific engineering categories listed in the 2026 guidelines:

- Category 1: Secondary Water Resistance (SWR). This involves applying a self-adhering polymer modified bitumen underlayment (commonly called "peel-and-stick") directly to the roof decking before shingles are laid. If a storm blows your shingles off, the SWR keeps the water out. This single feature triggers one of the highest discounts on a Florida policy.

- Category 2: Roof-to-Wall Connection (Clips vs. Straps). If your home was built before 2008, your roof trusses are likely held down by "toenails" or simple clips. Using the grant to upgrade these to multi-nail hurricane straps wraps tightly over the truss, forcing a dramatic re-rating of your wind risk profile.

- Category 3: 100% Opening Protection. To get the master opening credit, every single glazed opening (windows, exterior doors, garage doors, and skylights) must be impact-rated or protected by compliant shutters. If you protect 19 windows but leave one small bathroom window bare, the insurance system throws out the master discount. The hack requires total completion.

4. The Order of Execution: Avoid Disqualification

The state is incredibly strict about the sequence of events. If you get the order wrong, you will be disqualified from receiving the reimbursement check:

**1.Apply for the Free Inspection:**Takes 10-15 Minutes.

Log onto mysafeflhome.com and submit your homestead exemption and active homeowners insurance documentation.

**2.Complete the Initial Inspection:**1-3 Hours on Site.

A state-contracted inspector will evaluate your home's roof-decking, attachments, and openings to generate an official Initial Inspection Report.

**3.Submit the Prioritization Questionnaire:**Critical Income Step.

Log back into the portal and upload your financial data. Over 30,000 Floridians missed this step and froze their eligibility. This step confirms your priority window.

**4.Secure Your Grant Award Letter:**Do NOT Start Work Before This.

Submit your formal grant application matching the recommendations in your report. You must receive your official Grant Award Letter before signing a contractor agreement or swinging a hammer.

**5.Execute Work & Pass Final Inspection:**Must Complete Within 1 Year.

Hire a Florida-licensed contractor to execute the upgrades. Once completed, request and pass the official MSFH final inspection via the portal to trigger your reimbursement check.

Why Working with an Independent Agency is Vital

The MSFH portal gives you the grant money, but it doesn't automatically fix your insurance bill. At Walker Insurance Agency, we bridge the gap between completed construction and active premium cuts.

The Walker Advantage:

- Pre-Project Audit: We review your initial inspection report before you select a contractor to calculate exactly which upgrade will yield the highest premium ROI relative to your out-of-pocket match.

- The Citizens Exit Strategy: If your home is trapped in Citizens, we use your new 2026 wind-mitigation credits to market your home to the 20 brand-new private insurance companies entering Florida, often cutting your rate by an additional 15% to 25%.

- Form OIR-B1-1802 Verification: We review the final inspection form to ensure the inspector checked the correct engineering boxes, preventing automated data entry errors at the carrier level.

FAQ

1. Can I use the grant to swap my existing hurricane shutters for impact windows?

No. The "No-Swap" rule is strictly enforced. The program only funds upgrades for openings that are currently unprotected. If your home already has code-compliant removable shutters, the state will not pay to upgrade them to impact glass for convenience or aesthetics.

2. Is the $700,000 insured value cap based on market value?

No. It is based strictly on the Coverage A (Dwelling) limit listed on your homeowners insurance declarations page. If your home's market value is $900,000 but your rebuild cost (Coverage A) is $650,000, you qualify. Low-income applicants are completely exempt from this limit.

3. Does the grant cover townhouses or condos in 2026?

Townhouses that are site-built and owner-occupied are eligible for Opening Protection grants only. They cannot receive roofing grants because townhouse roofs are typically governed by communal association guidelines. Condominiums are entirely excluded from the program.

Force the Insurance Market to Work for You

Don't let legacy insurance companies dictate your cost of living. By exploiting Florida's legal wind-mitigation mandates, you can build an ironclad barrier around your home using the state's checkbook.

Execute the hack today. Contact Walker Insurance Agency for a complimentary Pre-Mitigation Policy Review. We provide the visibility you need to map out your structural upgrades, maximize your wind credits, and secure the lowest premium floor available in Stuart.

[GET A FREE QUOTE TODAY]

Call us at +1-407-977-7100 or visit our office in Stuart, FL. Let us lower your premium today.

Related Articles

Does Home Insurance Cover Broken Pipes in the Yard? (2026)

Discover why standard homeowners insurance completely denies the cost to repair a broken sewer line or water main in your yard, and how Stuart homeowners can fix this gap.

Read More →

Does Home Insurance Cover Broken Underground Utility Lines? (2026)

Think your standard Florida homeowners insurance pays to fix a cracked water main or collapsed sewer line in your yard? Discover the property line pitfall leaving Stuart homes exposed.

Read More →

Does Full Coverage Car Insurance Cover Engine Repairs? (2026)

Think your standard 'full coverage' policy pays to fix a blown engine or failed transmission in Stuart? Discover the mechanical breakdown trap leaving Florida drivers exposed.

Read More →