Does Home Insurance Cover Broken Underground Utility Lines? (2026)

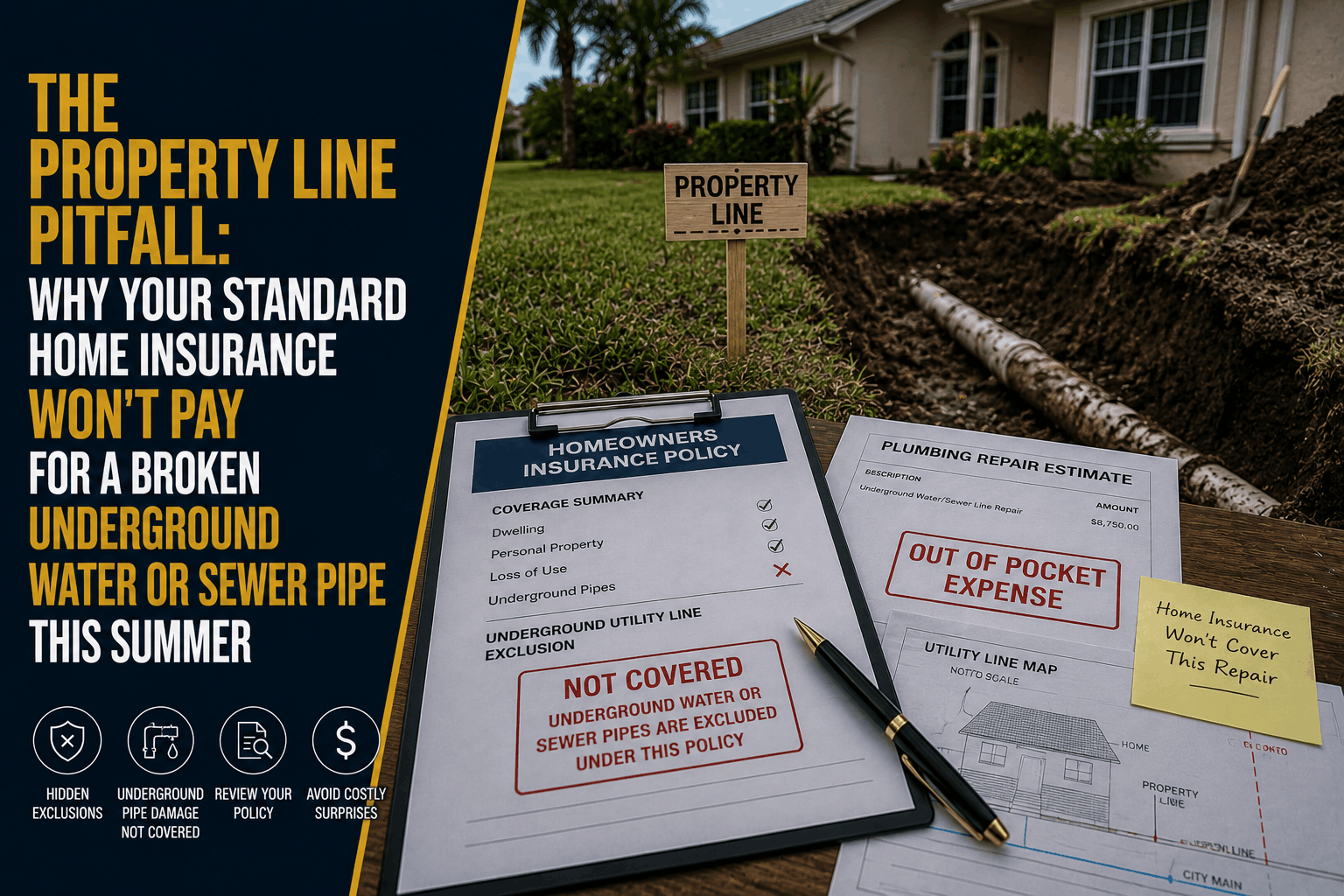

The Property Line Pitfall: Why Your Standard Home Insurance Won't Pay for a Broken Underground Water or Sewer Pipe This Summer

The Direct Answer

The short answer is no, it will not pay a single dollar. In 2026, one of the most financially devastating surprises a Florida homeowner can face is discovering that standard homeowners insurance completely excludes underground utility lines running through their yard. If an underground water main cracks, a sewer pipe collapses, or invasive tree roots rupture your waste line this summer, your standard policy will issue an immediate denial. A baseline home policy is strictly designed to protect the structural dwelling and items located inside the footprint of the home. It explicitly excludes exterior underground piping, wiring, and service lines due to standard wear, tear, and gradual soil movement. Because the local city utility municipality only owns the main lines under the street, you are legally and financially responsible for the entire length of pipe running from the street curb to your foundation wall, leaving you to pay for excavation and replacement costs entirely out of pocket.

For property owners across Stuart and the Treasure Coast, this contractual boundary line creates a massive exposure gap. With high summer temperatures accelerating soil shifting and coastal humidity putting aging infrastructure under constant strain, underground pipe failures have become a leading cause of unrecoverable, multi-thousand-dollar property losses for completely unprotected households.

1. The Real Cost Breakdowns of an Excavation Denial

When an underground pipe fails, the financial impact involves far more than simply patching a section of PVC or clay tile. Because these conduits are buried multiple feet beneath your lawn, the out-of-pocket overhead scales rapidly across heavy operational phases:

- Trenching and Heavy Excavation: Simply locating, digging up, and exposing a broken sewer lateral or water main requires heavy equipment and specialized labor. Excavation crews routinely charge $3,000 to $6,000 just to cut open your yard, punch through walkways, or tear up a driveway before any plumbing work even begins.

- Pipe Replacement and Utility Hookups: Removing the compromised line and laying modern, code-compliant conduit routinely scales from $2,500 to $5,000. If the line runs beneath mature local landscaping or professional hardscaping, restoration costs climb rapidly.

- The Total Infrastructure Bill: When you combine excavation, material sourcing, city permitting, and full landscape restoration, a single broken exterior utility line easily results in a flat $6,000 to $12,000 out-of-pocket invoice. Because your baseline policy excludes everything outside your foundation wall, you must fund this entire amount immediately to restore water or waste services to your household.

2. Understanding the Crucial Difference: Water Backup vs. Service Line Coverage

Many homeowners assume they are protected because their policy includes a water backup endorsement. While backup protection is highly valuable, it addresses a completely different mechanical event, leaving a massive financial hole if your exterior lines physically fail:

Kin Insurance

- Water Backup Endorsement (The Internal Clad): This optional add-on protects your finances if a city sewer line backs up or a drain overflows, sending dirty water into your home. It pays to tear out ruined drywall, clean contaminated carpets, and replace waterlogged appliances inside the structure. However, it explicitly pays $0 to dig up, repair, or replace the physical broken pipe out in the yard that caused the issue.

Farmers Insurance+ 1 - Service Line Coverage (The External Shield): This is the precise rider required to defeat the property line pitfall. It is a distinct, low-cost endorsement that specifically extends your property insurance outward, covering the physical excavation, repair, and environmental restoration of underground water, sewer, electrical, and natural gas lines running through your property boundaries.

3. How to Protect Your Property and Erase the Loophole

You do not have to leave your savings vulnerable to an unexpected trenching bill, but you must take proactive steps to update your policy framework before an underground emergency occurs. At Walker Insurance Agency, we advise Stuart homeowners to safeguard their land using a clear three-step defensive layout:

- Step 1: Map Your Service Responsibilities. Locate your property lines and identify exactly where your water meter and sewer cleanouts sit relative to the municipal connection at the street curb. Trace the physical path your utilities take across your lawn to understand your exposure zone.

- Step 2: Bind a Dedicated Service Line Endorsement. Request your independent agent to attach a specialized service line rider directly to your home insurance policy. This targeted addition explicitly covers wear, tear, rust, and tree root intrusion for underground utilities, providing up to $10,000 or $20,000 in dedicated protection for a nominal monthly cost.

- Step 3: Document Tree Canopy Proximity. Take note of any mature trees or large root systems growing within ten feet of your primary water and waste lines. Tree root intrusion is the single most common cause of subterranean line collapse along the Treasure Coast, making active preventative coverage essential.

Why Working with an Independent Agency is Vital

Attempting to manage complex property boundaries and structural exclusions through a basic digital form ensures you will miss the fine-print limitations that trigger immediate claims denials. At Walker Insurance Agency, we provide the personalized, data-driven visibility you need to keep your home fully insulated.

The Walker Advantage:

- Exclusion Form Dissection: We thoroughly audit your underlying homeowners declarations to expose hidden property-line gaps before a utility failure catches you off guard.

- Rider Integration Sourcing: We continuously shop your profile across Florida's leading independent insurance market to locate comprehensive service line and water backup options tailored to your home's age.

- Local Inflation Balancing: We align your policy limits with the actual reality of local Martin County contractor rates and excavation overhead so your hard-earned wealth is completely protected.

FAQ

1. Does the city cover any portion of the pipe if the break happens under the sidewalk?

It depends strictly on your local municipal contract, but in most areas of Florida, the homeowner is responsible for the line all the way until it connects directly to the main utility trunk line, even if that section runs beneath a public sidewalk or easement on your property. You must review local ordinances or carry a service line rider to absorb this risk.

2. Will a standard policy cover the repair if a contractor accidentally cuts my line while digging?

Yes, potentially. If an unrelated third-party contractor breaches your underground utility line while performing work, the damage is caused by a sudden, accidental external force, which can be covered under standard property lines or pursued through the contractor's commercial general liability insurance. The policy exclusions focus primarily on natural degradation, wear, tear, and root damage.

3. Can I add service line coverage to a policy on an older home with cast iron pipes?

Yes, but availability varies by insurance company. Some carriers place age restrictions or require a clean plumbing inspection before binding underground utility riders on older homes. Working with an independent agency allows us to match your specific home age with a carrier that accepts the risk without charging predatory premiums.

Insulate Your Property Lines Before an Underground Break Occurs

Your home is your most valuable asset, but assuming a standard property policy covers the extensive infrastructure buried beneath your grass is an administrative gamble that can instantly drain your bank account. True peace of mind requires pulling back the curtain on your policy’s structural exclusions and ensuring your contract matches the physical reality of your utility lines.

Take control of your home protection today. Contact Walker Insurance Agency for a comprehensive portfolio evaluation. We provide the visibility you need to eliminate hidden side-yard loopholes, deploy high-limit service line riders, and protect your family's hard-earned wealth safely in Stuart.

[GET A FREE QUOTE TODAY]

Call our personal lines division at +1-407-977-7100 or visit our office in Stuart, FL. Let us safeguard your property boundaries today.

Related Articles

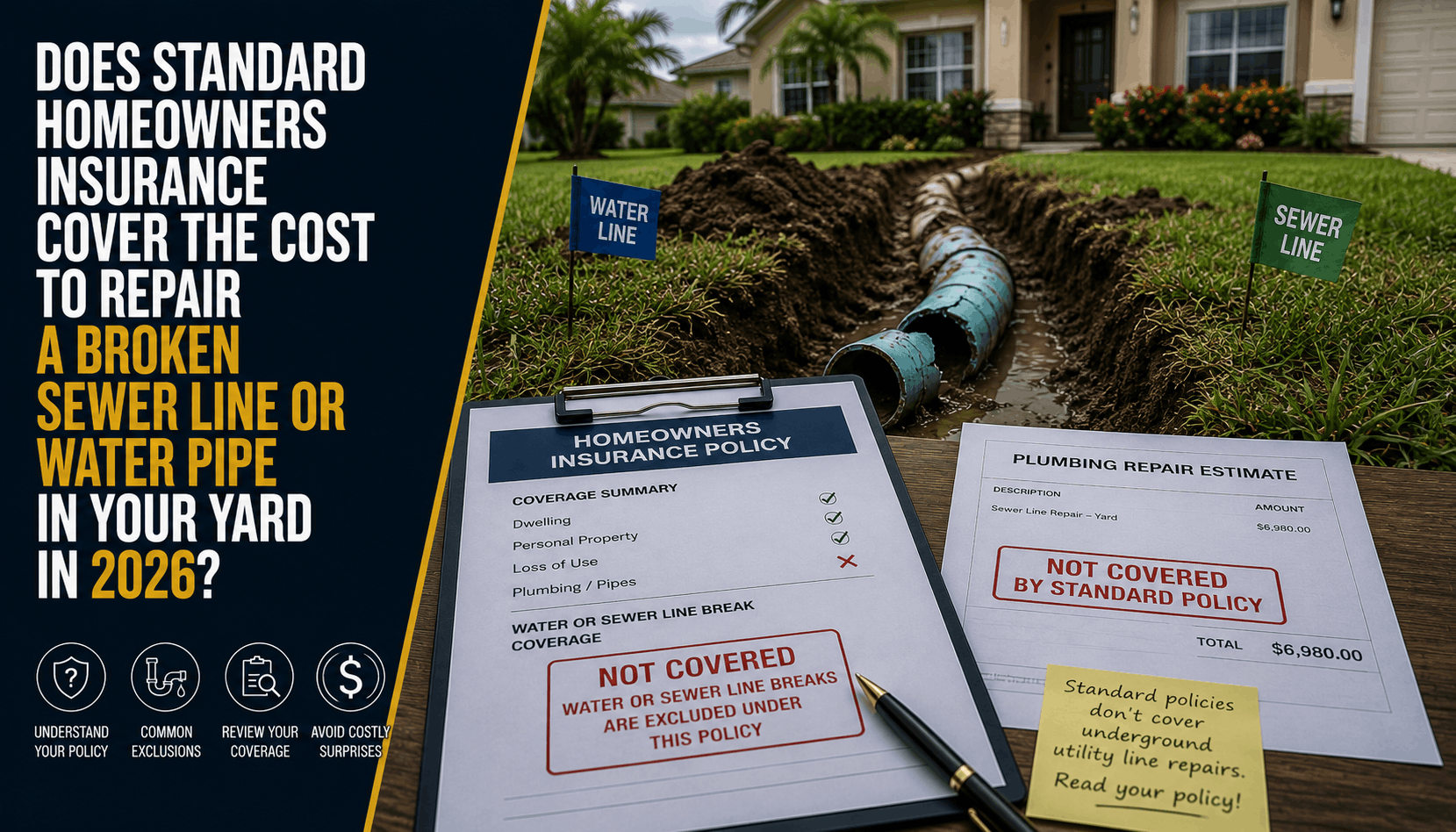

Does Home Insurance Cover Broken Pipes in the Yard? (2026)

Discover why standard homeowners insurance completely denies the cost to repair a broken sewer line or water main in your yard, and how Stuart homeowners can fix this gap.

Read More →

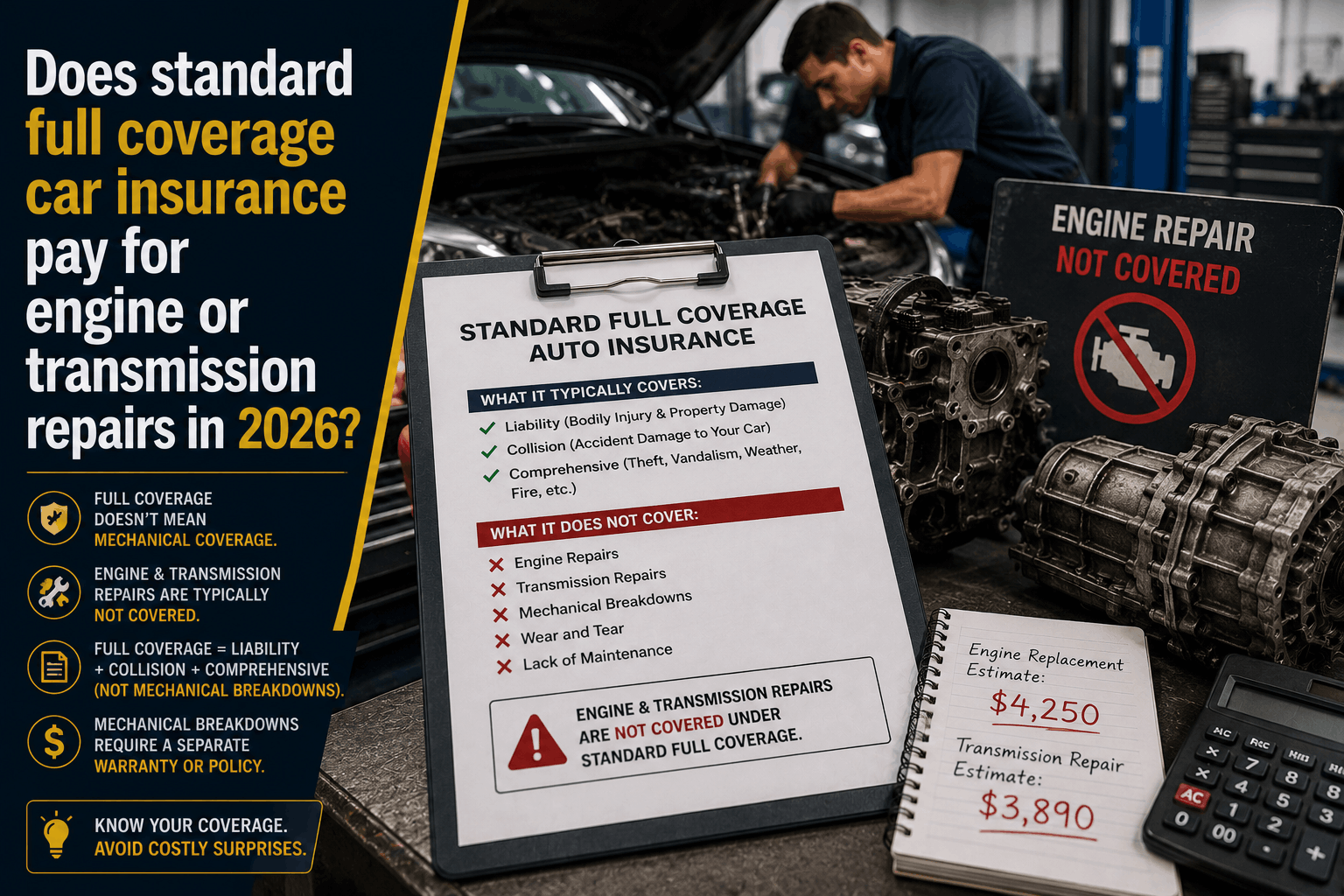

Does Full Coverage Car Insurance Cover Engine Repairs? (2026)

Think your standard 'full coverage' policy pays to fix a blown engine or failed transmission in Stuart? Discover the mechanical breakdown trap leaving Florida drivers exposed.

Read More →

Why Full Coverage Auto Insurance Won't Pay Your Car Loan (2026)

Think your standard 'full coverage' policy will wipe out your car loan after a total loss in Stuart? Discover the dangerous actual cash value trap leaving drivers exposed this summer.

Read More →