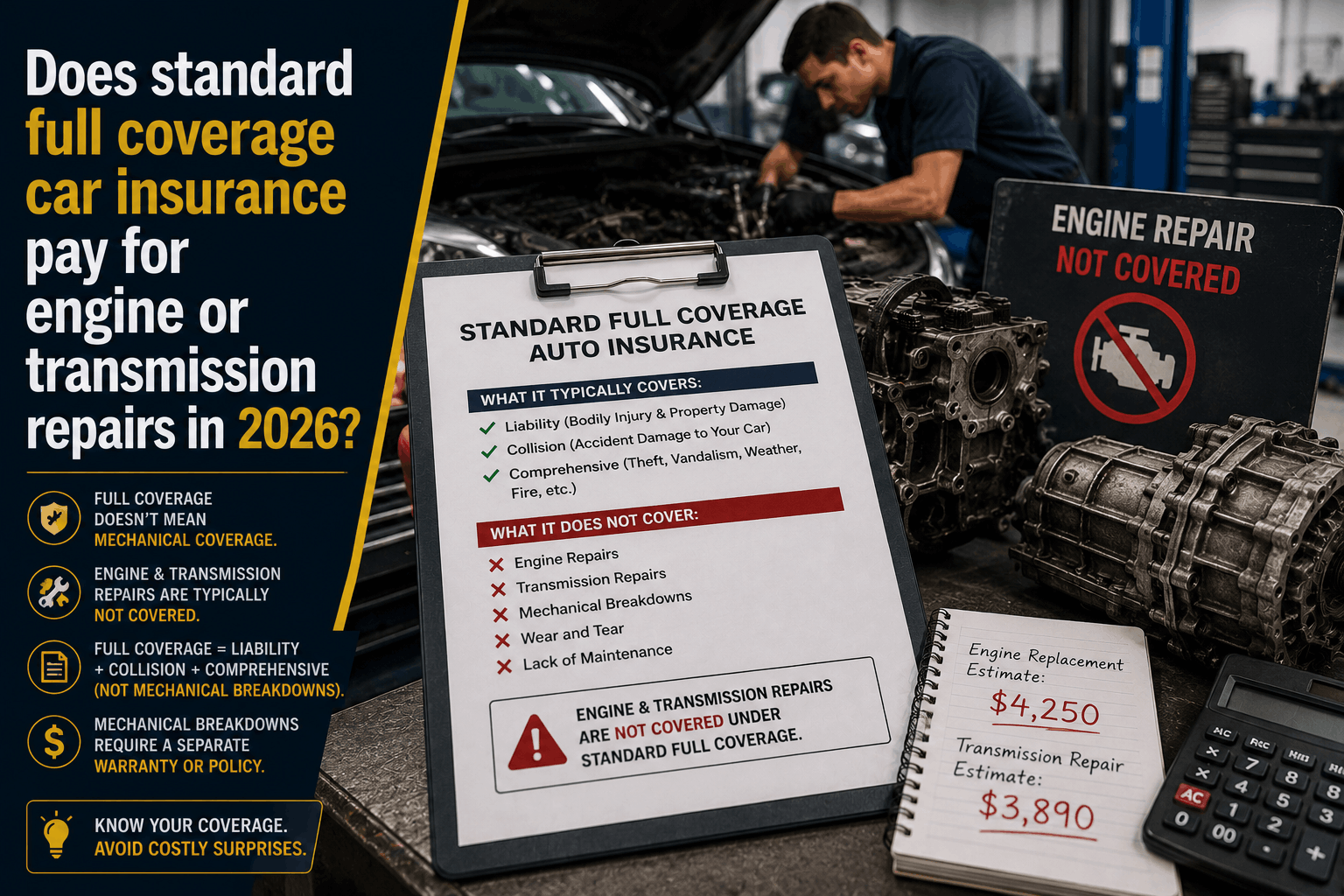

Does Full Coverage Car Insurance Cover Engine Repairs? (2026)

The Mechanical Myth: Why Your Standard 'Full Coverage' Auto Policy Won't Pay for Engine or Transmission Repairs This Summer

The Direct Answer

The short answer is no, it absolutely will not. In 2026, one of the most expensive assumptions a driver can make is believing that "full coverage" auto insurance doubles as a mechanical repair warranty. If your engine suddenly throws a rod, your head gasket blows, or your transmission shifts into a permanent limp mode while driving down US-1, your standard insurance carrier will deny your claim entirely. A standard full coverage policy—consisting of comprehensive and collision protections—is strictly designed to repair damage caused by external, sudden, and accidental events. It explicitly excludes internal mechanical failures, electrical defects, lack of maintenance, and standard wear and tear. If your car experiences an internal mechanical breakdown this summer, your regular car insurance will pay exactly $0, leaving you to fund thousands of dollars in engine or transmission replacement costs completely out of pocket.

For vehicle owners across Stuart and the Treasure Coast, this distinction is critical in 2026. As modern vehicles rely heavily on complex computerized powertrains, turbochargers, and hybrid systems, the market cost of a catastrophic mechanical failure has skyrocketed, transforming routine internal breakdowns into sudden, massive household financial crises.

1. The Covered vs. Excluded Divide: Tracing the Cause of Damage

The only scenario where a standard personal auto policy will touch an engine or a transmission is if a covered external peril physically compromises the mechanical asset. To understand where the legal line is drawn, compare these everyday operational scenarios:

- When Insurance WILL Pay (External Force): If you hit a deep pothole or strike a piece of road debris that cracks open your transmission fluid pan, causing the system to seize, your Collision Coverage will handle the repairs. Similarly, if a severe Florida summer thunderstorm knocks a tree limb onto your hood, crushing your engine block, or a flash flood submerges your front end and hydro-locks the cylinders, your Comprehensive Coverage steps in because the damage was caused by an unpredictable external event.

- When Insurance WILL NOT Pay (Internal Failure): If you are commuting to work and your transmission simply slips out of gear due to a faulty torque converter, worn-out clutch plates, or low fluid levels over time, your policy will issue an immediate denial. The same applies if your engine overheats and warps the cylinder walls. From an underwriting standpoint, these are internal mechanical failures, not accidents.

2. The Extreme Reality of Modern Replacement Overhead

Operating under the assumption that your standard policy acts as a catch-all maintenance shield leaves your personal savings completely exposed. If an engine or transmission fails outside of an accident, the real-world out-of-pocket costs at Martin County repair facilities are staggering:

- Standard Transmission Replacements: Sourcing and installing a new or remanufactured transmission on a modern crossover or sedan routinely scales from $4,000 to $7,500. For advanced continuous variable transmissions (CVTs) or dual-clutch systems, parts and labor overhead mount rapidly.

- Catastrophic Engine Swaps: If an internal component breaks and destroys your engine block, a full replacement routinely reaches $6,500 to $11,000 depending on the make and model. Because your personal policy excludes internal wear and tear, this entire balance must be cleared directly by you before the mechanic releases your keys.

- The Component Chain Reaction: If a mechanical failure causes you to lose control of your vehicle and strike an object, your collision policy will pay to fix your crushed bumper and sheet metal, but they will still deduct the cost of the original failed mechanical component from your claim payout.

3. How to Insulate Your Wallet from Surprise Component Failures

You do not have to drive in fear of an unexpected mechanical bill, but you must bridge the contract gap between traditional accident insurance and true internal vehicle protection. At Walker Insurance Agency, we advise local drivers to systematically audit their vehicle portfolios using three specific safety nets:

- Step 1: Check Your Factory Powertrain Warranty. If your vehicle is newer or has low mileage, verify if it is still protected under the manufacturer's original 5-year/60,000-mile or 10-year/100,000-mile powertrain warranty. This factory contract is your primary shield against manufacturing defects.

- Step 2: Explore Mechanical Breakdown Insurance (MBI). If your vehicle is out of warranty but still relatively young, ask your independent agent about adding an optional Mechanical Breakdown Insurance (MBI) rider. Available through specialized carriers, MBI functions exactly like an extended auto warranty but is regulated as an insurance policy. It explicitly steps in to pay for engine, transmission, electrical, and steering repairs after you pay a small, flat deductible (typically $100 to $250).

- Step 3: Establish a Dedicated Liquid Upkeep Buffer. Neither standard insurance nor extended warranties cover wear-and-tear items like brake pads, tires, or missed oil changes. Divert a portion of your monthly budget into a dedicated vehicle emergency fund to protect your primary capital from inevitable maintenance cycles.

Why Working with an Independent Agency is Vital

Navigating the complex gray areas between mechanical warranties, factory recalls, and physical damage auto insurance through a basic smartphone app is a recipe for a costly claims denial. At Walker Insurance Agency, we deliver the personalized oversight required to keep your assets fully insulated on the road.

The Walker Advantage:

- Contract Loophole Analysis: We thoroughly cross-reference your auto policy declarations against your vehicle's current mileage to pinpoint exactly where your accident coverage stops and your mechanical vulnerability begins.

- Specialized Rider Sourcing: We shop your profile across Florida's leading independent carriers to locate competitive companies offering comprehensive MBI add-ons for a fraction of the cost of dealership extended service contracts.

- Local Claim Advocacy: If an accident causes a complex mechanical issue, our team acts as your direct advocate, ensuring claims adjusters don't falsely label collision damage as standard wear and tear.

FAQ

1. Does a manufacturer's vehicle recall cover my engine or transmission if it breaks down?

Yes, but only if the failure is directly tied to a specific component defect officially recognized by the National Highway Traffic Safety Administration (NHTSA) and the vehicle manufacturer. If a recall is active, the dealership must perform the repair for free. However, if the component fails due to age, high mileage, or a lack of routine maintenance outside of a recall window, you are fully responsible for the bill.

2. If my engine blows because I forgot to change the oil, will Mechanical Breakdown Insurance cover it?

No. Every mechanical protection policy—whether it is an MBI rider or a third-party extended warranty—explicitly requires the owner to maintain the vehicle according to the manufacturer’s schedule. If a claims adjuster requests your service history and finds that you skipped routine oil changes or ignored critical warning lights, your claim will be denied for owner negligence.

3. What is the difference between Mechanical Breakdown Insurance (MBI) and a dealership extended warranty?

MBI is backed and regulated by an insurance company, allowing you to choose any licensed repair facility and typically costing significantly less per year as an integrated policy add-on. Dealership extended service contracts are often expensive, flat-fee packages rolled directly into your auto loan (meaning you pay interest on them), and they often restrict your repair options to specific brand networks.

Safeguard Your Vehicle's Lifeline Before an Internal Failure Strikes

Your car's engine and transmission are its most expensive mechanical components, but assuming a standard "full coverage" label will save you from an internal mechanical failure is an administrative gamble that can derail your financial summer. True peace of mind requires looking closely at your real-world warranty status and ensuring your asset protection matches the physical realities of vehicle wear and tear.

Take complete control of your auto protection today. Contact Walker Insurance Agency for a comprehensive portfolio evaluation. We provide the strategic visibility you need to eliminate hidden coverage blind spots, deploy specialized mechanical breakdown options, and keep your family's hard-earned wealth safe in Stuart.

[GET A FREE QUOTE TODAY]

Call our personal lines division at +1-407-977-7100 or visit our office in Stuart, FL. Let us safeguard your property boundaries today.

Related Articles

Does Home Insurance Cover Broken Pipes in the Yard? (2026)

Discover why standard homeowners insurance completely denies the cost to repair a broken sewer line or water main in your yard, and how Stuart homeowners can fix this gap.

Read More →

Does Home Insurance Cover Broken Underground Utility Lines? (2026)

Think your standard Florida homeowners insurance pays to fix a cracked water main or collapsed sewer line in your yard? Discover the property line pitfall leaving Stuart homes exposed.

Read More →

Why Full Coverage Auto Insurance Won't Pay Your Car Loan (2026)

Think your standard 'full coverage' policy will wipe out your car loan after a total loss in Stuart? Discover the dangerous actual cash value trap leaving drivers exposed this summer.

Read More →