Does Homeowners Insurance Cover a Fried HVAC or Broken Fridge?

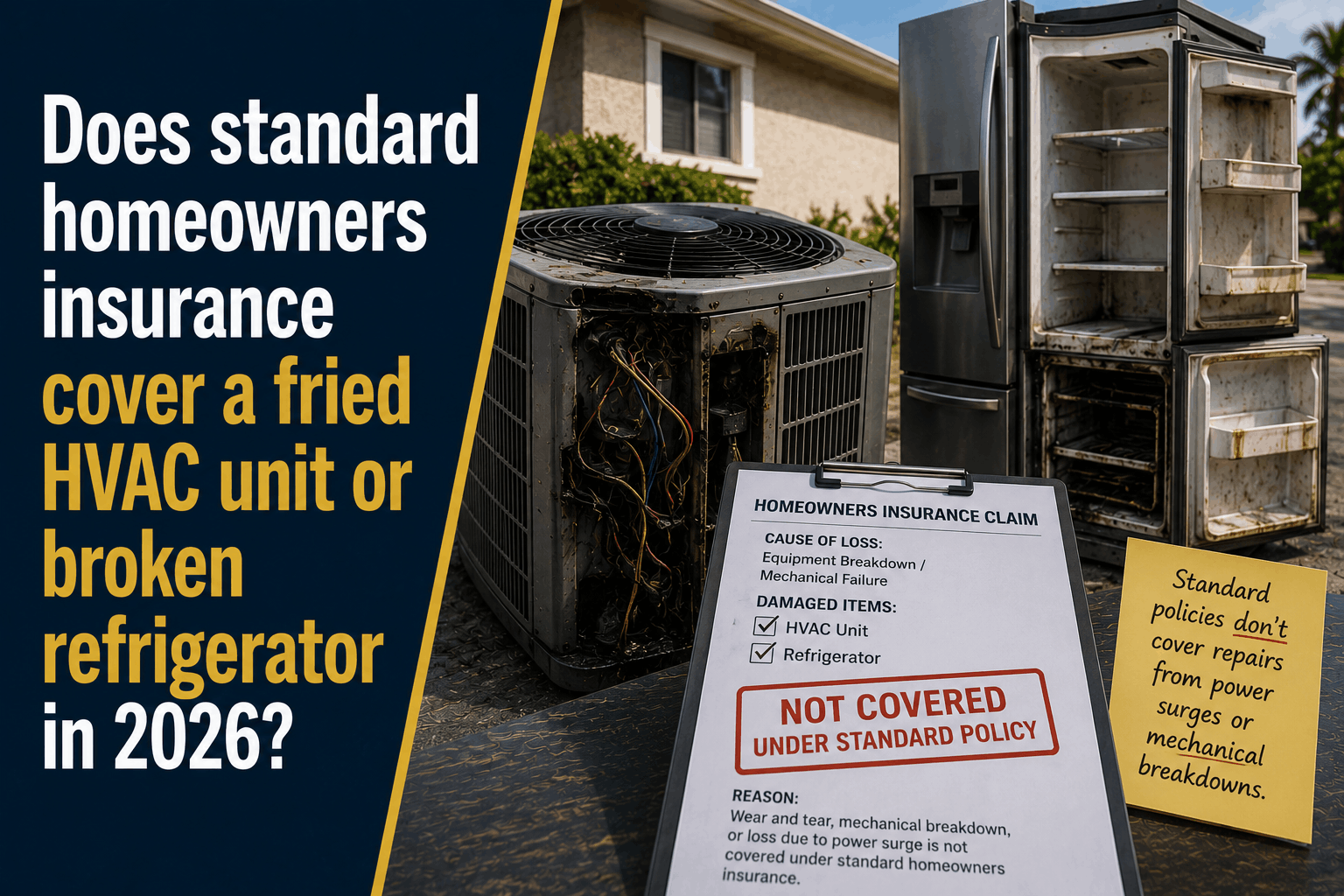

Does Standard Homeowners Insurance Cover a Fried HVAC Unit or Broken Refrigerator in 2026?

The Direct Answer: Generally, no—a standard homeowners insurance policy will not cover a fried HVAC unit or a broken refrigerator. While your policy is contractually bound to cover sudden and accidental physical damage caused by specific "named perils" (like a fire, a fallen tree, or a direct lightning strike), it explicitly excludes mechanical breakdowns, internal electrical shorts, electrical fluctuations, and normal wear and tear.

In 2026, this baseline exclusion is catching thousands of property owners completely off guard. As extreme summer heatwaves push regional power grids to their absolute limit, homes are experiencing an unprecedented number of rolling blackouts and voltage spikes.

To achieve total visibility over your property defenses, you must understand a critical legal catch: if a sudden power surge cuts through your neighborhood and fries the computer circuit boards inside your smart fridge or central air conditioner, your insurance carrier will legally deny 100% of the claim unless you have explicitly paid for an optional add-on rider known as an Equipment Breakdown Endorsement.

1. The Power Grid Surge Loophole

Many homeowners believe that any electrical damage is covered under standard fire and lightning protections. However, insurance adjusters utilize a strict diagnostic framework to separate covered utility losses from excluded events:

[Trigger: A physical bolt of lightning strikes your roof] ───> 100% COVERED.

[Trigger: A voltage spike rebounds from street power lines] ──> 100% DENIED by default.

The Technology Crisis: Modern appliances and inverter-driven HVAC systems are no longer basic mechanical motors; they are advanced computers. They feature intricate printed circuit boards (PCBs) and microprocessors that are hypersensitive to micro-changes in voltage. What used to be a harmless power flicker for a refrigerator built in 1990 means instant death for the main motherboard of a modern $4,000 smart appliance. Because a standard HO-3 policy only covers "artificially generated current" if lightning is the direct cause, street-level utility spikes fall right into a massive coverage loophole.

2. Payout Scenarios: Maintenance vs. Accident

If your refrigerator or HVAC system stops working this year, the outcome of your insurance claim depends entirely on the proximate (original) cause of the failure:

| What Caused the Failure? | Is It Covered by a Standard Policy? | How the Claim Settles |

|---|---|---|

| Old Age / Wear & Tear | NO | Excluded as routine homeowner maintenance. You must pay 100% of the repair bill out of pocket. |

| Grid Power Surge | NO | Excluded under the "artificially generated electrical current" fine print. Denied by default. |

| Direct Lightning Strike | YES | Covered under your primary policy. Pays to repair or replace the unit, minus your standard deductible. |

| Vandalism / Tree Strike | YES | Covered as a standard physical peril. Pays for structural and mechanical damage up to your policy limits. |

3. The Modern Repair Overhead

Relying on an unmodified baseline insurance policy leaves your cash reserves entirely exposed to record-high contractor labor rates and tech-heavy component pricing. If your systems are fried this summer, these are the average out-of-pocket numbers you face:

- Smart Refrigerator Circuitry: Replacing burned inverter boards, compressor relays, and digital touch-screen control panels on a high-end refrigerator promedias $800 to $1,500.

- HVAC Control Inverter Boards: Swapping out fried variable-speed fan components and main circuit relays inside a modern high-efficiency central air conditioner runs between $1,200 and $2,800.

- Burned AC Compressor: If a voltage spike shorts out the electrical windings inside your condensing unit, replacing the compressor or installing a new exterior unit costs $3,500 to $6,000.

How to Safely Close the Appliance Loophole

If your primary residential assets are currently sitting on an unmodified property contract, your emergency fund is entirely vulnerable to a single utility grid flicker.

At Walker Insurance Agency, we advise property owners to build an ironclad shield using a precise, two-layer defensive layout:

Step 1: Append an Equipment Breakdown Endorsement (Contractual Defense)

Step 2: Install a Certified Type 2 Panel Surge Protector (Physical Defense)

=============================================================================

= 100% Comprehensive Safety From Internal Bloat to External Power Grid Surges

- The Contractual Shield: Request that your independent agent add an Equipment Breakdown Endorsement to your homeowners line. For a very low premium addition (typically $25 to $50 per year), this rider completely overrides the standard exclusions. It forces the carrier to pay up to $50,000 for mechanical failures, electrical shorts, and grid surge damage across all your large appliances and HVAC systems, carrying a manageable, flat $500 deductible.

- The Physical Shield: Have a licensed electrician install a whole-house surge protector directly onto your main electrical panel. This device blocks high-voltage surges coming from the street before they ever reach your interior drywall outlets. Many preferred insurance carriers in Stuart offer premium discounts or require these installations to bind coverage on smart homes.

Why Working with an Independent Agency is Vital

Attempting to manage your primary property assets through a generic smartphone application or automated online form ensures you will miss the critical riders needed to survive utility failures. At Walker Insurance Agency, we provide the personalized, data-driven visibility you need to defend your home.

The Walker Advantage:

- Endorsement Portfolio Audits: We break down your current coverage details line-by-line to unearth hidden electrical limitations and fortify your contract with preferred riders before an emergency occurs.

- Mitigation Discount Integration: We ensure that your professional panel surge protector installation is formally logged with your underwriter, legally triggering safety credits to lower your annual costs.

- Resurgent Market Matching: As the stabilizing Florida market introduces 20 brand-new private insurance carriers entering the state, we continuously shop your profile to secure the highest-limit property riders at the absolute lowest available premium floors in Stuart.

FAQ

1. Does my standard home insurance cover the cost of spoiled food if my refrigerator breaks down? A standard policy will only pay for spoiled food (usually capped at $500) if the refrigerator fails due to a wide-scale power outage caused by a covered peril, such as a hurricane or a tree knocking down power lines on your property. If the food spoils because the refrigerator simply suffered an internal mechanical failure or a grid-level voltage surge, the food loss is completely excluded unless you carry an equipment breakdown endorsement.

2. Can an insurance company deny a lightning claim if I don't have proof of a direct strike? Yes. If you file a claim alleging that lightning fried your HVAC unit, the adjuster will request an inspection by a certified technician. If the diagnostic report reveals no physical signs of a lightning strike—such as melted wires, scorch marks, or blasted components—and instead shows basic electrical deterioration, the carrier will reclassify the event as an excluded power surge or wear-and-tear issue and deny the claim.

3. What should I do immediately if a power surge fries my appliances? Unplug the affected electronics immediately to prevent secondary thermal damage. Contact a licensed appliance repair technician or HVAC specialist to perform a formal diagnostic evaluation. Ensure the technician writes a detailed invoice specifying that the failure was caused by an acute voltage surge (documenting melted boards or shorted relays). Save this paperwork; it serves as the primary proof your independent agent needs to successfully open an endorsed claim.

Insulate Your Technology from an Infrastructure Crisis Today

Your modern home functions like a giant computer, but your insurance policy might still be written under the analog rules of the past. Leaving your expensive climate-control systems and smart appliances vulnerable to an unstable power grid is a gamble that can wipe out thousands of dollars from your family's savings account in a single second.

Secure your electronic systems before the next heatwave. Contact Walker Insurance Agency today for a comprehensive property coverage review. We provide the visibility you need to eliminate hidden utility loops, deploy high-limit equipment breakdown riders, and protect your hard-earned wealth safely in Stuart.

[GET A FREE QUOTE TODAY]

Call us at +1-407-977-7100 or visit our office in Stuart, FL. Let us safeguard your home today.

Related Articles

Does Homeowners Insurance Pay for Code Upgrades After a Fire?

A standard home insurance policy won't cover mandatory building code upgrades after a fire. Learn about the Ordinance or Law trap and how to protect your home.

Read More →

The Code Compliance Trap: Why Home Insurance Won't Pay for Upgrades

Discovered a massive gap in your property insurance after a disaster? Learn why standard home insurance completely denies mandatory building code upgrades in 2026.

Read More →

Does Florida Homeowners Insurance Cover a Pool Cage in 2026?

Learn about the "Lanai Loophole" in Florida. Discover why standard homeowners insurance excludes or limits hurricane damage to pool cages and screen enclosures.

Read More →