Does Florida Home Insurance Cover Wildfire Damage? (2026)

Does Florida Home Insurance Cover Wildfire Damage?

The Direct Answer: Yes. A standard Florida homeowners insurance policy (HO-3 or HO-5) specifically covers fire as a "covered peril," which includes damage from wildfires. In April 2026, as Florida faces its most severe drought in over 25 years, this coverage is more critical than ever. Your policy protects you from direct flame contact, heat-related warping, and the extensive smoke and ash damage that can occur even if the fire never touches your structure.

However, achieving total visibility over your protection requires looking at the "fine print" of 2026. With rebuilding costs in Florida rising by 8% this year and new administrative resolution processes for disputed claims, being "covered" on paper isn't the same as being fully protected in practice.

1. What is Specifically Covered in 2026?

If a wildfire affects your home during this drought season, your policy typically provides four main layers of protection:

- Dwelling Coverage (Coverage A): Repairs or replaces the structure of your home. In 2026, the median cost to rebuild in Florida has hit approximately $280 per square foot.

- Personal Property (Coverage C): Replaces furniture, electronics, and clothing damaged by fire or smoke.

- Loss of Use / ALE (Coverage D): Pays for hotels and meals if a mandatory evacuation is ordered or if your home is uninhabitable.

- Other Structures (Coverage B): Covers detached garages, sheds, and fences.

2. The Smoke and Ash Factor

In 2026, many Florida claims are not for "burnt" homes, but for smoke and soot infiltration.

- Hidden Contamination: Wildfire smoke travels through HVAC systems and settles in attics and insulation.

- Chemical Residue: Wildfire ash often contains toxic particles from burned industrial materials. Standard policies cover the professional remediation of these contaminants.

- Documentation Rule: In 2026, insurers are strictly enforcing a "document before you clean" policy. Wiping away soot before an adjuster sees it can lead to a denied claim for lack of evidence.

3. Rebuilding Challenges in the 2026 Economy

The "Insurance Gap" is a major risk this year. Because of the widespread nature of the 2026 drought, a single wildfire event can destroy dozens of homes at once, causing a local surge in labor and material costs.

- Extended Replacement Cost: We strongly recommend this endorsement. It provides an extra 25% to 50% above your policy limit to cover the "price spikes" that happen after a disaster.

- Ordinance or Law Coverage: If your home was built before the latest 2026 Florida Building Code updates, you need this coverage to pay for mandatory upgrades during a rebuild.

4. 2026 Legislative Updates: HB 815

As of mid-2026, new Florida laws (HB 815) provide extra protection for homeowners during renewals. Insurers can no longer deny or non-renew your policy solely based on the age of your roof if an inspection shows it is in good condition. This is vital, as a well-maintained roof is your home’s first defense against wind-borne embers during a wildfire.

Why Working with an Independent Agency is the Best Move

At Walker Insurance Agency, we don't just look at today's premium; we look at tomorrow's rebuild. We provide the visibility you need to ensure your "Total Insured Value" reflects the actual 2026 cost of construction in Stuart and across Florida.

The Walker Advantage:

- Accurate Valuations: We use the latest 2026 data to ensure your Coverage A isn't lagging behind inflation.

- Evacuation Expertise: We help you understand exactly when your "Loss of Use" benefits trigger during a wildfire emergency.

- Claim Advocacy: If you face a dispute over smoke damage, we guide you through the new 2026 Administrative Resolution Process, which offers a faster path to settlement than traditional litigation.

FAQ

1. Does my insurance cover damage from a neighbor's "prescribed burn" that got out of control? Yes. Whether the fire is a natural wildfire or a man-made fire that spreads to your property, it is covered under the "Fire" peril of your homeowners policy.

2. Are my trees and lawn covered if they burn? Standard policies provide limited coverage for landscaping, often capped at 5% of your dwelling limit and usually no more than $500 per tree. In a severe drought, this may not cover the full cost of a mature landscape.

3. What if I am evacuated but my house doesn't burn? If a civil authority (like a sheriff or fire marshal) orders a mandatory evacuation due to an approaching wildfire, your "Additional Living Expenses" (ALE) coverage will typically pay for your hotel and meals for a limited time.

4. Does insurance cover a car that burns in my garage? No. Damage to vehicles is covered by the Comprehensive portion of your Auto Insurance, even if the car was inside your burning home.

Local Business Schema

Don’t Wait for the Tinderbox to Ignite

With Florida currently facing its most dangerous wildfire season in decades, "good enough" coverage is a gamble you can't afford.

Protect your sanctuary today. Contact Walker Insurance Agency for a complimentary wildfire risk audit. We provide the visibility you need to ensure your home is fully protected against the flames and the financial fallout of the 2026 drought.

[GET A FREE QUOTE TODAY] Call us at +1-407-977-7100 or visit our office in Stuart, FL. Let us help you protect your peace of mind.

Related Articles

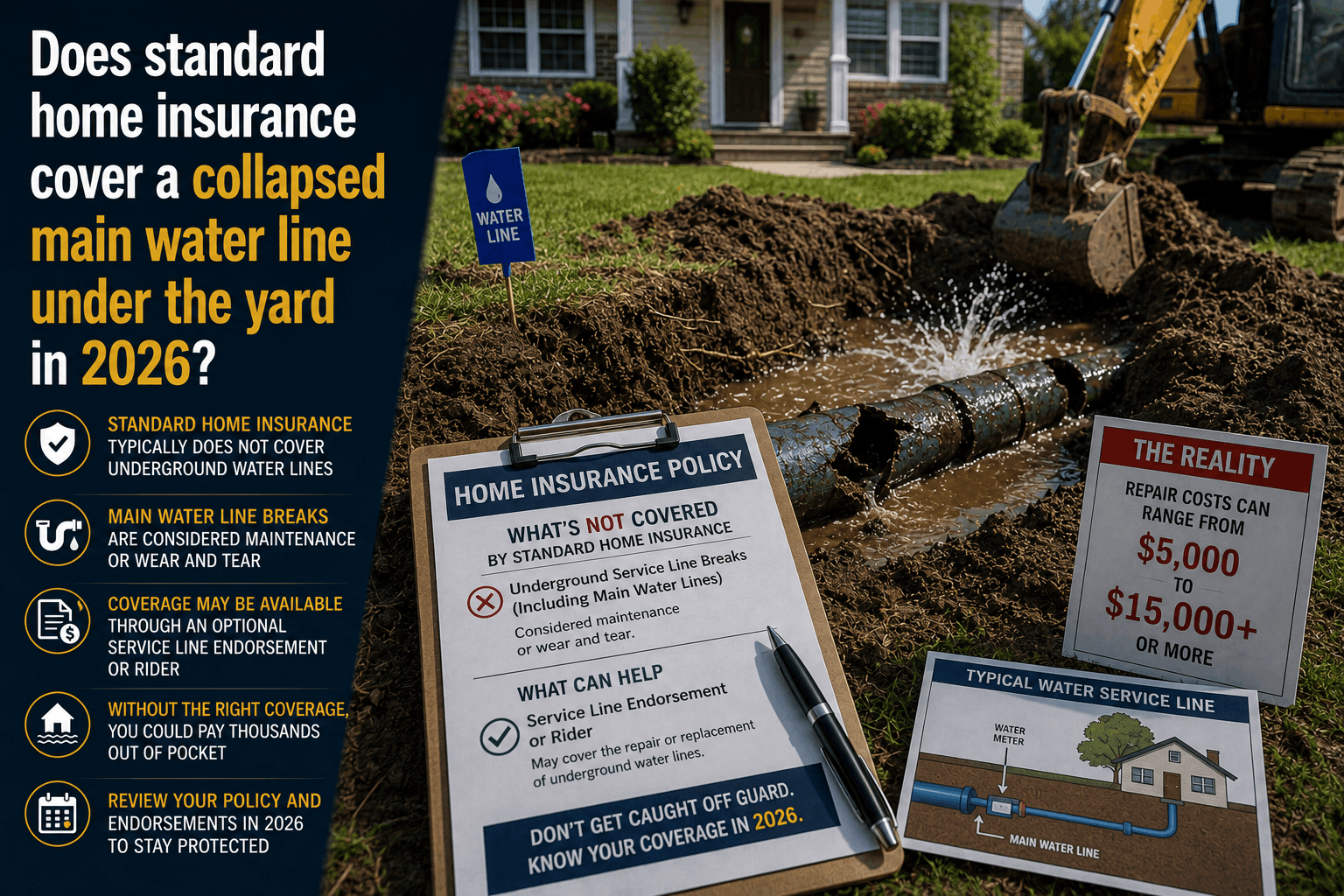

Does Home Insurance Cover a Collapsed Water Line in the Yard? (2026 Rules)

Find out if standard home insurance covers a water line collapse under your yard. Learn about the strict "slab-up" rule and the crucial Service Line Endorsement.

Read More →

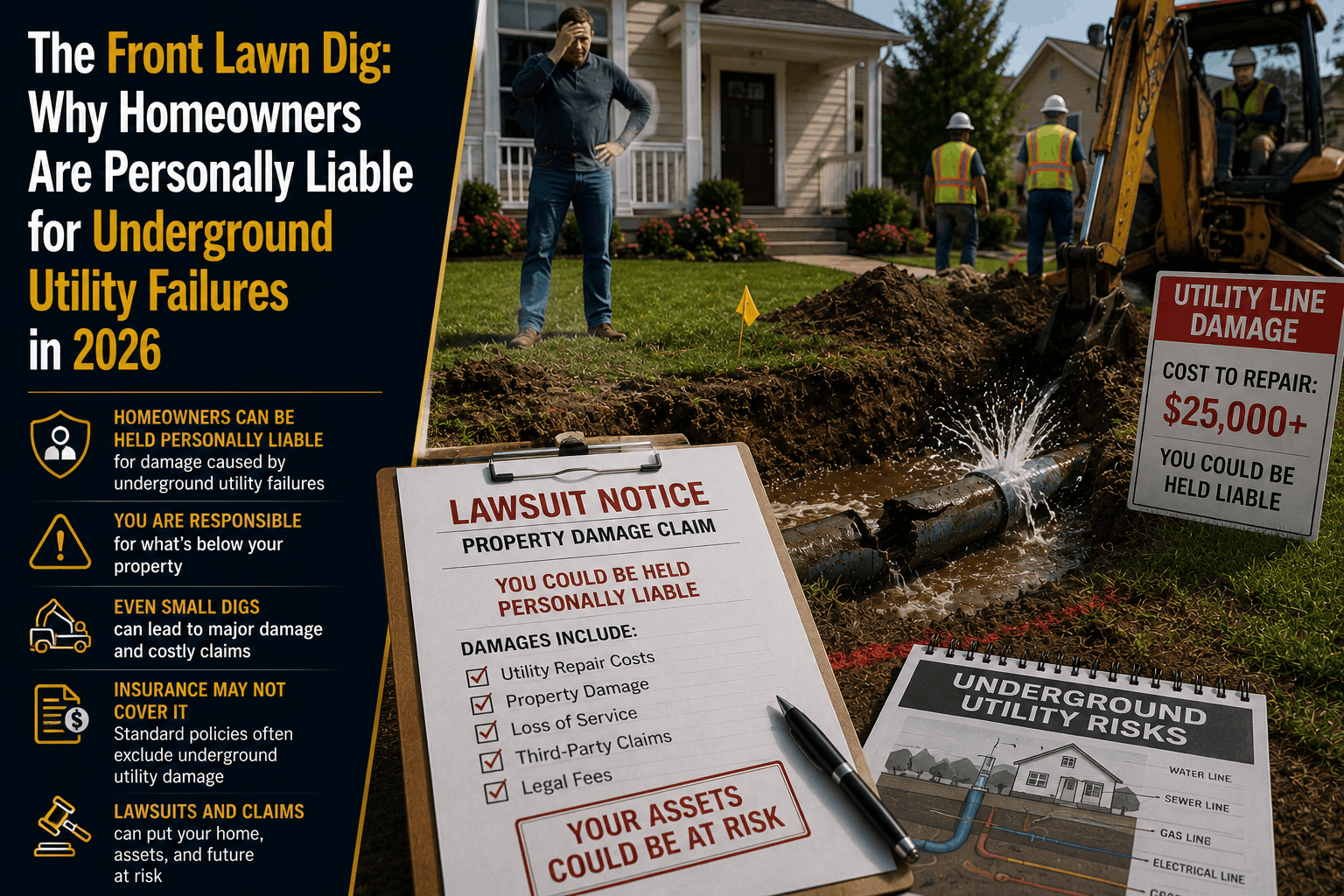

The Front Lawn Dig: Why You Own the Underground Utility Risk in 2026

Think the city pays if an underground pipe bursts under your lawn? Discover why standard Florida home insurance leaves you personally liable for buried utility lines.

Read More →

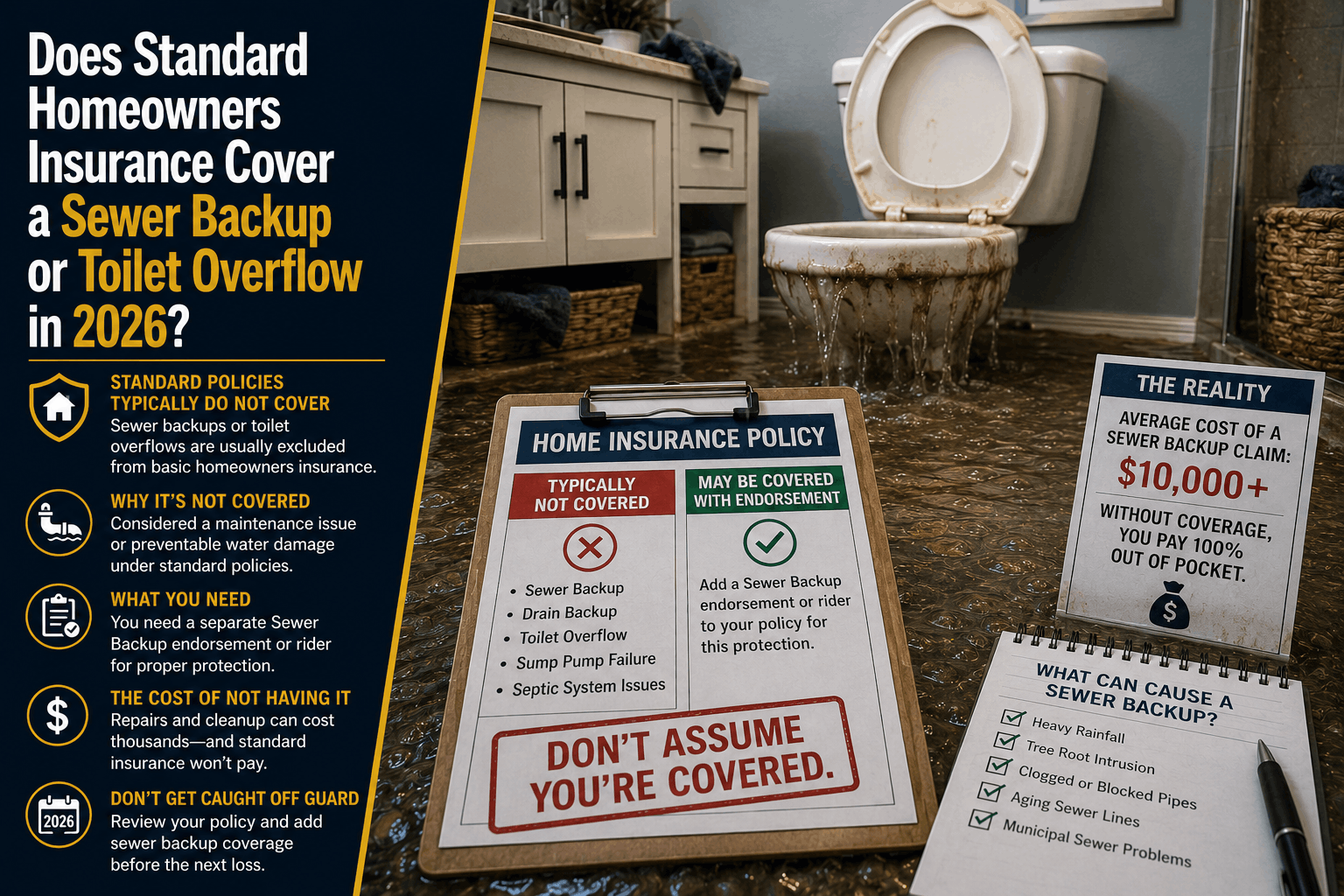

Does Homeowners Insurance Cover Sewer Backup or Toilet Overflow? (2026 Guide)

Discover how standard homeowners insurance handles sewage backups and toilet overflows in 2026\. Learn the strict rules that separate a covered claim from a denial.

Read More →