Car Insurance in Florida: Does It Cover Hurricane & Flood Damage?

Does Car Insurance Cover Hurricane and Storm Damage in Florida?

Living in Florida means enjoying warm weather year-round — but it also means preparing for hurricane season.

If you live in Stuart or anywhere in Martin County, one major question you should ask is: If a storm damages my vehicle, am I covered?

The answer depends entirely on your coverage.

What Type of Car Insurance Covers Storm Damage?

In Florida, only comprehensive coverage protects your vehicle from natural disasters.

Comprehensive insurance typically covers:

- Hurricane damage

- Flooding

- Falling trees

- Wind damage

- Hail damage

- Flying debris

- Vandalism

- Fire

If you only carry liability insurance, your policy will NOT cover damage to your own vehicle — even if the damage is caused by a hurricane.

Liability coverage protects others. Comprehensive coverage protects your car.

Why Storm Damage Is a Real Risk in Martin County

Drivers in Stuart and surrounding areas face:

- Heavy rainfall accumulation

- Parking lot flooding

- Coastal storm surge

- Downed power lines

- Tree branches falling during high winds

During hurricane season, vehicles parked outside are especially vulnerable.

Every year, Florida drivers file thousands of comprehensive claims after named storms. Many only discover coverage gaps after removing comprehensive coverage to lower their premium.

Saving a small amount monthly can become a major financial loss after a storm.

Flood Damage Is More Serious Than Most Drivers Think

Water intrusion can cause immediate and long-term damage, including:

- Engine failure

- Transmission damage

- Electrical system failure

- Sensor malfunctions

- Interior mold and corrosion

Modern vehicles rely heavily on electronics. Even shallow flooding can total a car quickly.

Insurance companies often declare flood-damaged vehicles as total losses because repairs can exceed the vehicle’s value.

Without comprehensive coverage, that loss comes entirely out of pocket.

How Much Does Comprehensive Coverage Cost in Florida?

Comprehensive coverage is often more affordable than drivers expect — especially compared to:

- The cost of replacing a vehicle

- Repairing water-damaged electronics

- Engine replacement

- Transmission repairs

In many cases, the additional premium for comprehensive coverage is small relative to the financial protection it provides during hurricane season.

The key is choosing a deductible you can realistically afford.

Important: Hurricane Claims Follow Specific Rules

In Florida:

- Comprehensive coverage applies to storm-related vehicle damage

- Deductibles apply per claim

- Coverage must be active before the storm begins

Just like with homeowners insurance, once a storm is imminent, you cannot add coverage retroactively.

Preparation must happen before the storm is named.

Final Advice for Florida Drivers

Before hurricane season begins, review your auto policy and confirm:

- You have comprehensive coverage

- Your deductible is manageable

- You understand what is and isn’t covered

- Your vehicle’s value justifies the coverage

Storms are unpredictable. Your coverage shouldn’t be.

If you’re unsure whether your current car insurance in Florida protects you from hurricane or flood damage, reviewing your policy before storm season can prevent costly surprises later.

FAQ – Car Insurance & Storm Damage in Florida

Does liability insurance cover hurricane damage to my car?

No. Liability insurance only covers damage you cause to others. Comprehensive coverage protects your own vehicle from storm damage.

Does car insurance cover flood damage in Florida?

Yes — but only if you carry comprehensive coverage.

Can a flooded car be totaled?

Yes. Even minor flooding can damage electrical systems and engines, leading insurers to declare the vehicle a total loss.

Should I remove comprehensive coverage to save money?

It depends on your vehicle’s value and your financial situation, but during hurricane season in Florida, removing comprehensive coverage increases your risk significantly.

Related Articles

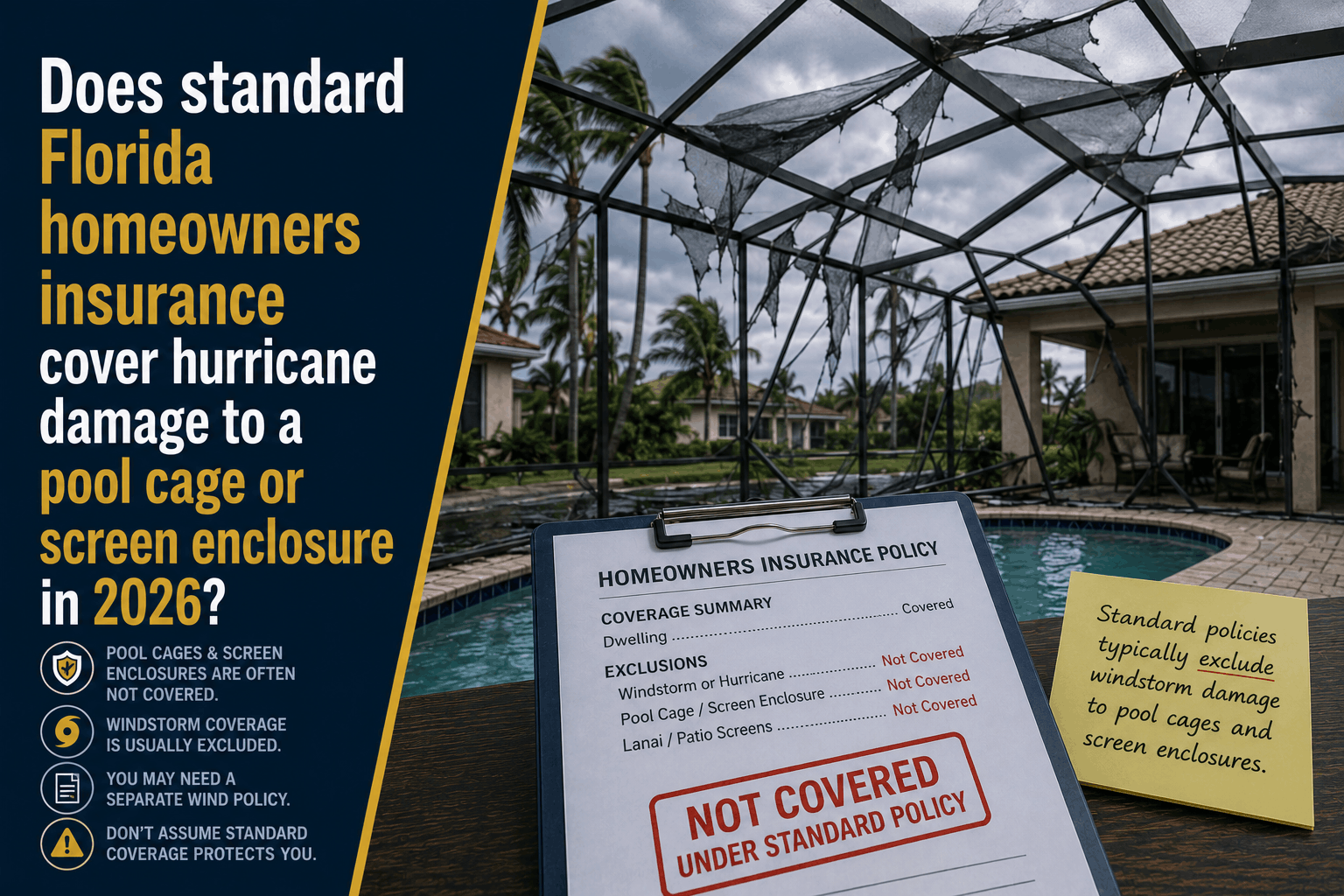

Does Florida Homeowners Insurance Cover a Pool Cage in 2026?

Learn about the "Lanai Loophole" in Florida. Discover why standard homeowners insurance excludes or limits hurricane damage to pool cages and screen enclosures.

Read More →

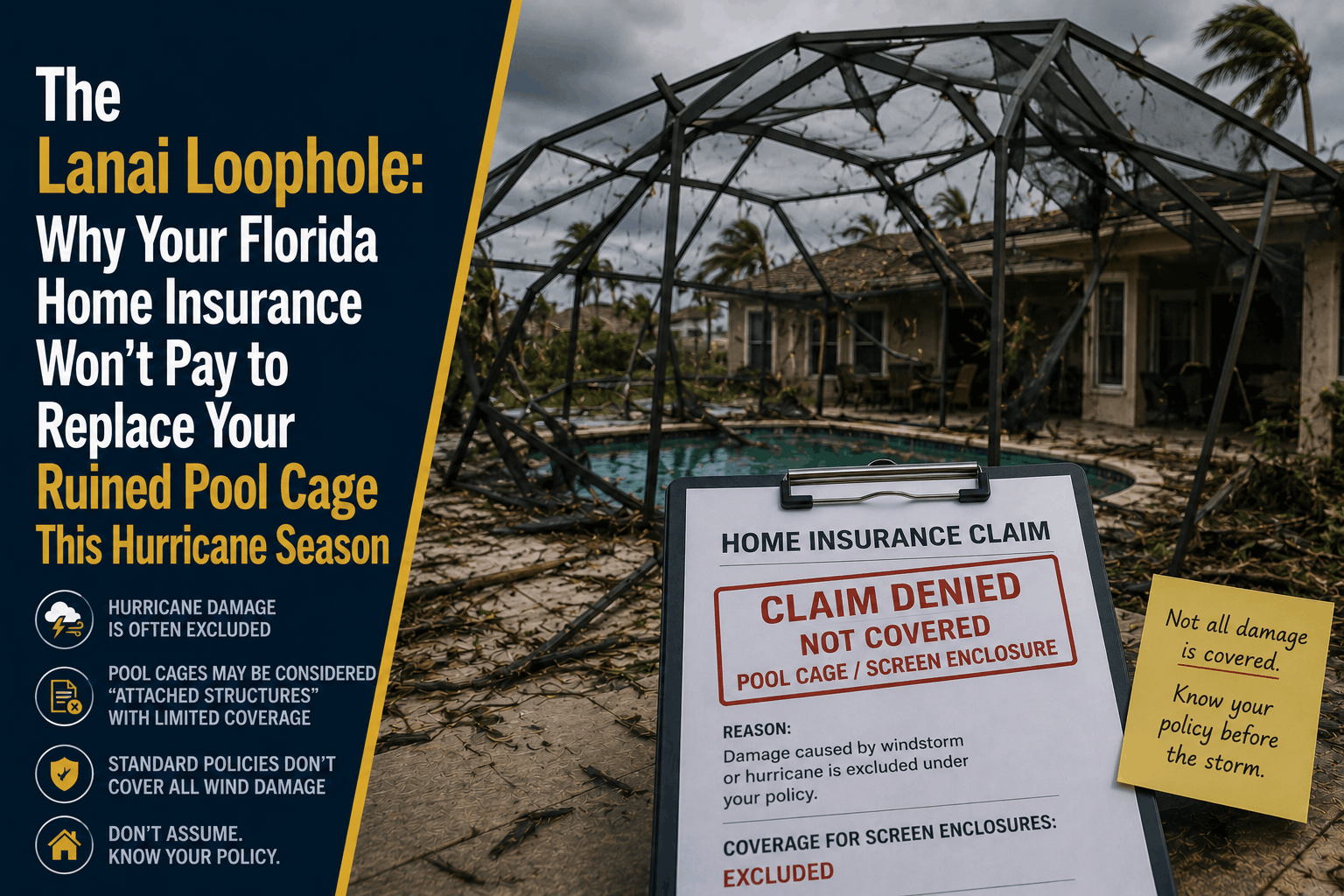

The Lanai Loophole: Why Home Insurance Won't Fix Your Pool Cage

Discover how Florida’s strict "Lanai Loophole" can completely exclude or limit your pool cage and screen enclosure coverage this hurricane season.

Read More →

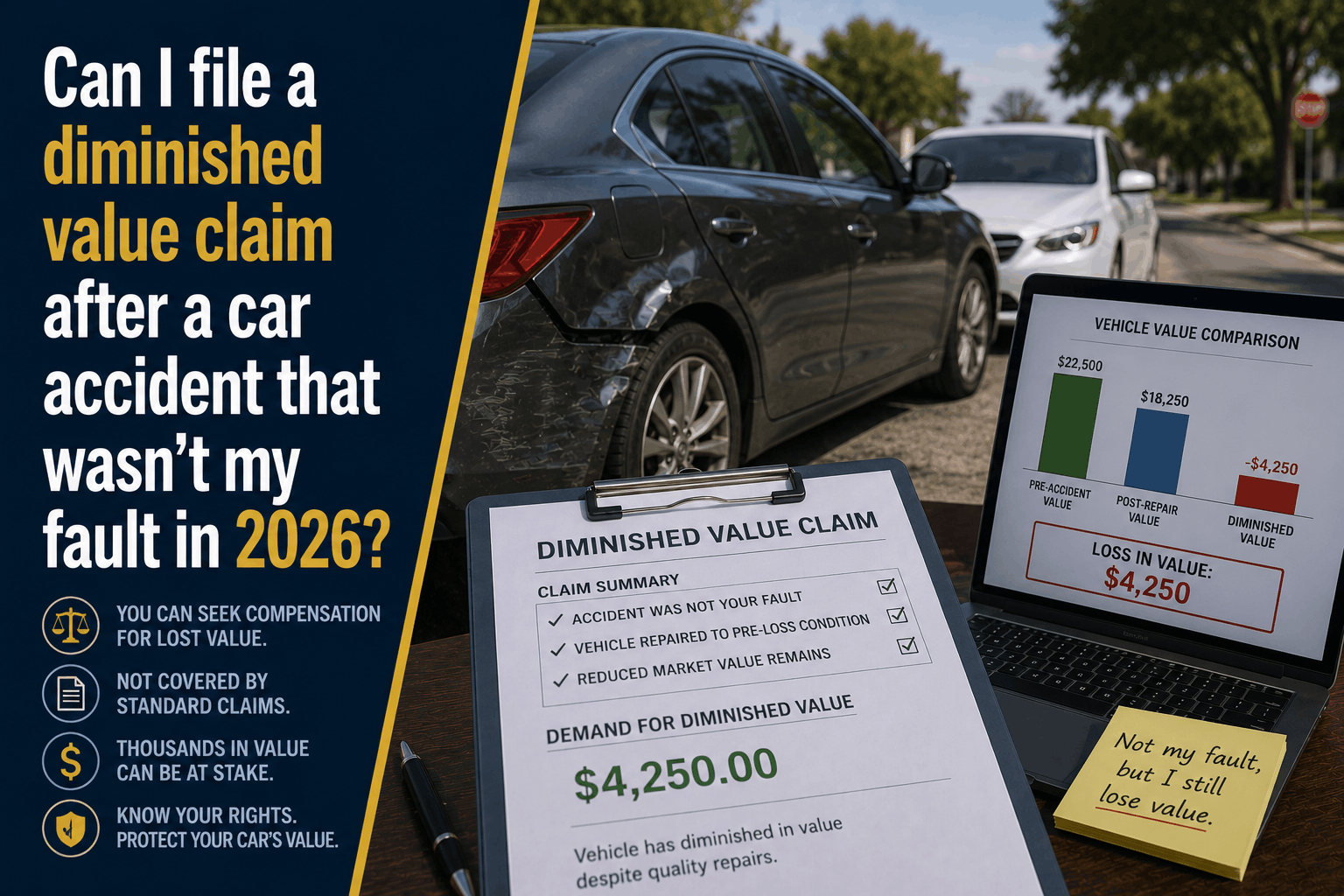

Can I File a Diminished Value Claim in 2026? (Not At-Fault Guide)

If you were involved in a car accident that wasn't your fault, discover how to file a Diminished Value claim to recover your vehicle's lost resale value.

Read More →