2026 My Safe Florida Home Grant Eligibility Requirements Guide

What Are the Eligibility Requirements for the My Safe Florida Home Grant in 2026?

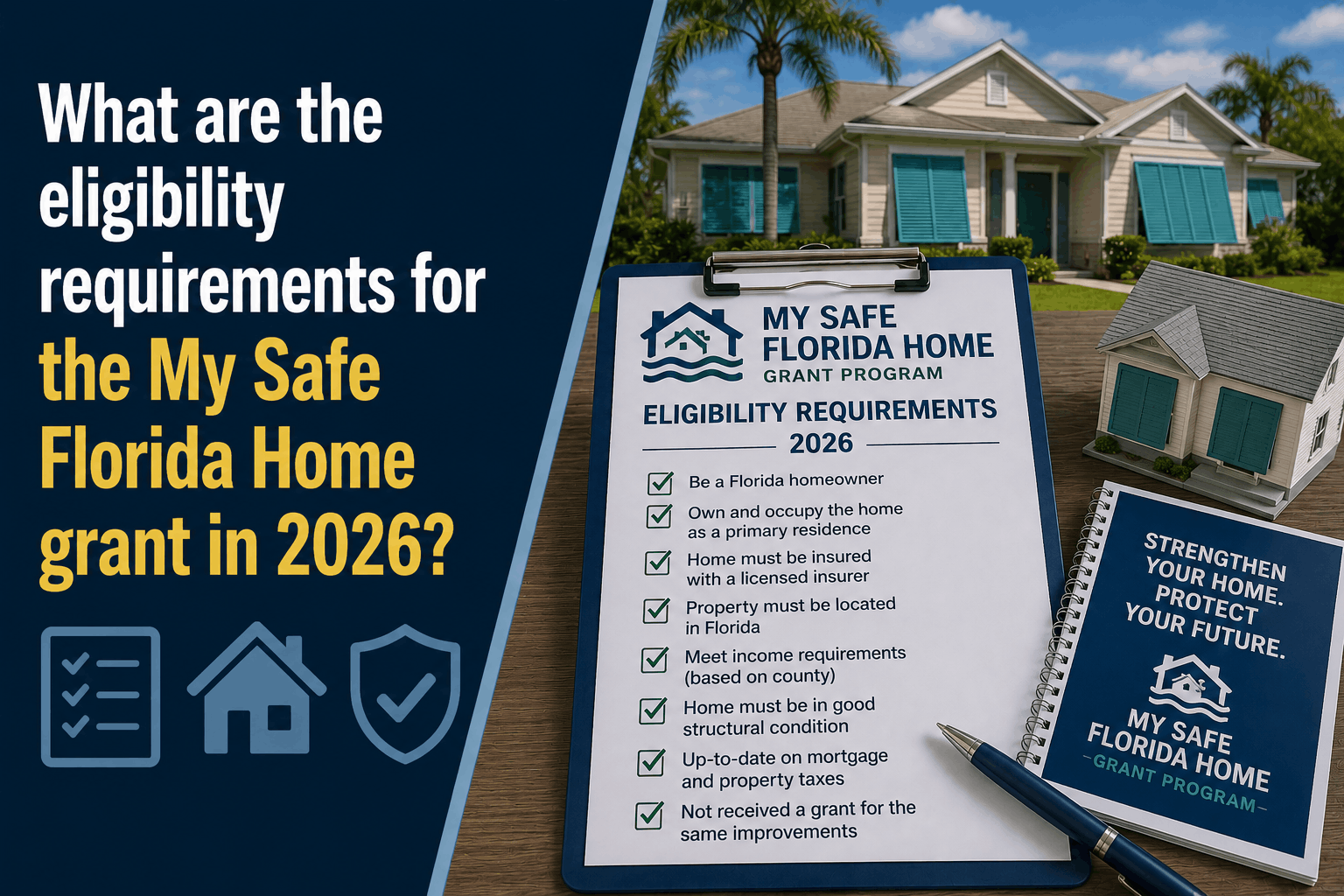

The Direct Answer: To qualify for the $10,000 My Safe Florida Home (MSFH) grant in May 2026, both you and your property must meet a strict, updated set of criteria. The baseline rules mandate that your home must be an owner-occupied, site-built, single-family detached home or townhouse with a valid Florida homestead exemption, and its initial building permit must date before January 1, 2008. Furthermore, your home's insured value (Coverage A) cannot exceed $700,000, you must provide proof of active homeowners insurance, and your household income must fall at or below 120% of your county's Area Median Income (AMI).

To achieve total visibility over your application, you must realize that qualifying for the program's free inspection does not automatically guarantee you grant money. In 2026, the state has phased out high-income applications for grant funds entirely, dedicating the current $600+ million budget exclusively to low- and moderate-income households.

1. Property Eligibility: The Physical Requirements

Your home must fit specific structural and legal definitions to be considered for a hardening grant this year:

- Property Type: It must be a site-built, single-family detached home or a townhouse (up to 3 stories). Mobile homes, manufactured housing, modular homes, multi-family apartment buildings, and individual condominium units are completely ineligible for the main program.

- Homestead Exemption: The home must be your primary residence. You must have a valid Florida homestead exemption on file with your county property appraiser. Second homes, vacation rentals, and investment properties do not qualify.

- The 2008 Rule: The initial building permit for the home's construction must have been issued before January 1, 2008. Homes built after this date were already constructed under the modernized, post-2007 Florida Building Code wind standards and are excluded.

- The $700,000 Insured Value Cap: The Coverage A (Dwelling) limit listed on your homeowners insurance declarations page must be $700,000 or less.

- Note: Verified low-income applicants are completely exempt from this $700k limit.

2. Household Eligibility: 2026 Income Tiers & Prioritization

The 2026 program structure is aggressively prioritized. If your household income exceeds 120% of your county's median income, you can still get a free inspection, but you are barred from receiving the $10,000 grant.

The state opens application windows in staggered phases according to this matrix:

| Priority Group | Household Status | Income Threshold | Grant Match Structure |

|---|---|---|---|

| Group 1 & 2 | Low-Income (Seniors 60+ apply first) | ≤ 80% of County Median | No Match Required: State pays 100% of real costs up to $10,000. |

| Group 3 & 4 | Moderate-Income (Seniors 60+ apply first) | 80% to 120% of County Median | 2:1 Match: State pays $2 for every $1 you spend, capped at $10,000. |

The 2026 Insurance Mandate: As of recent updates, all applicants—including low-income households who were previously exempt—must show proof of an active homeowners insurance policy to clear the eligibility portal.

3. The Technical Prerequisites

Meeting the property and income guidelines is only half the battle. To keep your eligibility active, you must follow the state's technical protocol:

- Official Program Inspection: You cannot submit a standard wind mitigation report from a private home inspector. You must request and complete a free inspection through the official mysafeflhome.com portal.

- The Prioritization Questionnaire: After your inspection is finished, you must log back into the portal and complete the income verification questionnaire (uploading your most recent IRS Form 1040). Skipping this step is the number-one reason applications freeze.

- No Prior Grants: The program follows a strict "one-and-done" rule. If your property received an MSFH grant during a previous funding cycle, it cannot receive a second allocation.

- Licensed Contractor Rule: All work must be performed by a Florida-licensed contractor. DIY installations or unpermitted work are immediately disqualified from reimbursement.

Why Working with an Independent Agency is Vital

Qualifying for the grant is a massive financial win, but the ultimate goal is forcing your insurance carrier to cut your premium. At Walker Insurance Agency, we provide the visibility you need to leverage your eligibility into long-term savings.

The Walker Advantage:

- Pre-Application Document Audit: We review your insurance declarations page and property appraiser data to ensure your Coverage A and permit dates match state requirements perfectly before you apply.

- Filing Optimization: Once your grant work passes final inspection, we submit your new OIR-B1-1802 Wind Mitigation Form to the top 20 private carriers entering the resurgent 2026 Florida market, often uncovering discounts that save homeowners an average of $981 per year.

- The Citizens Exit Execution: If your home is trapped in Citizens due to historical roof or window ages, we use your MSFH eligibility path to transition your property back to lower-cost, comprehensive private coverage in Stuart.

FAQ

1. Is the $700,000 limit based on my home's current market value? No. It is based strictly on the Coverage A (Dwelling) replacement cost limit found on your homeowners insurance policy declarations page. What your home could sell for on the real estate market does not impact this requirement.

2. What happens if I sign a contract with a window or roofing company before I get my grant approval?You will be completely disqualified. The state explicitly dictates that any construction started or contractual agreements signed prior to receiving your official Grant Award Letter cannot be reimbursed under any circumstances.

3. If my home has functioning hurricane shutters, can I qualify for a grant to upgrade to impact windows? No. The "No-Swap" rule states that if an opening already has code-compliant, functional storm protection (like aluminum panels), the program will not fund an upgrade to impact glass for convenience or cosmetic reasons. The grant is strictly reserved for unprotected or unrated openings.

Lock in Your State Funding Before the Windows Close

The 2026 MSFH budget is moving quickly, and the priority application windows close automatically once the county-level funding allocations are spoken for. If you wait for the next storm tracking towards the coast, the repository will be completely exhausted.

Verify your policy data today. Contact Walker Insurance Agency for a complete pre-application review. We provide the visibility you need to navigate the state portal flawlessly and convert your hardening grant into permanent premium reductions in Stuart.

[GET A FREE QUOTE TODAY] Call us at +1-407-977-7100 or visit our office in Stuart, FL.

Related Articles

Does Home Insurance Cover Broken Pipes in the Yard? (2026)

Discover why standard homeowners insurance completely denies the cost to repair a broken sewer line or water main in your yard, and how Stuart homeowners can fix this gap.

Read More →

Does Home Insurance Cover Broken Underground Utility Lines? (2026)

Think your standard Florida homeowners insurance pays to fix a cracked water main or collapsed sewer line in your yard? Discover the property line pitfall leaving Stuart homes exposed.

Read More →

Does Full Coverage Car Insurance Cover Engine Repairs? (2026)

Think your standard 'full coverage' policy pays to fix a blown engine or failed transmission in Stuart? Discover the mechanical breakdown trap leaving Florida drivers exposed.

Read More →