Wildfire Risk in Florida: Is Your Home Covered in the 2026 Drought?

Wildfire Risk in Florida: Is Your Home Covered in the 2026 Drought?

The Quick Answer: Yes, a standard Florida homeowners policy (HO-3) covers damage caused by wildfires, including smoke and ash. However, in April 2026, with over 96% of Florida gripped by the most severe drought in 25 years and over 120,000 acres already burned, the risk isn't just the fire—it's being underinsured. High inflation in construction costs (now averaging $150–$180 per sq. ft. in Florida) means a policy written two years ago might not cover a full rebuild if a wildfire strikes today.

To achieve total visibility over your sanctuary, you must look beyond the basic fire coverage and understand how the 2026 drought is changing the way insurers view your property.

1. The "Tinderbox" Reality of 2026

Meteorologists have officially labeled the current Florida spring as a "tinderbox." Record precipitation deficits (8 to 16 inches below normal since July 2025) have turned residential landscapes into fuel.

- Smoke and Ash Coverage: Even if the flames never touch your structure, your policy covers professional cleaning for smoke and ash. In 2026, many carriers are enforcing strict limits on these "indirect" claims, often requiring proof of a fire within a specific radius.

- Evacuation Costs: If a civil authority orders a mandatory evacuation, your Loss of Use (Coverage D) kicks in to pay for hotels and meals. Note: This usually does not apply to voluntary evacuations.

2. ISO Fire Protection Classes: The Hidden Cost

In 2026, drought-induced water restrictions in many Florida counties are impacting fire department readiness.

- Hydrant Pressure: If your municipality has reduced water pressure to conserve supply, your community's ISO rating (1–10) could be downgraded, leading to an immediate premium surcharge on your next renewal.

- Distance to Station: If you live more than 5 miles from a fire station in a high-risk brush area, some private carriers in 2026 are adding "Wildfire Surcharges" or excluding "Other Structures" (like sheds and fences) from fire coverage.

3. Rebuilding in the 2026 Economy

The cost to rebuild a home in Florida has spiked. According to 2026 construction data, a standard 2,000 sq. ft. home now costs between $300,000 and $360,000 to rebuild—excluding land.

- Extended Replacement Cost: Most standard policies only pay the "limit" on the page. We recommend an endorsement that provides 25–50% extra to protect against the surge in labor and material costs that follows a widespread wildfire event.

- Code Upgrades: If your home is older, the 2026 Florida Building Code requires expensive fire-resistant materials during a rebuild. Ensure you have Ordinance or Law coverage to pay for these mandatory upgrades.

4. Defensible Space: Your Insurance Discount

In 2026, proactive homeowners are being rewarded. Many Florida insurers now offer credits if you maintain "Defensible Space":

- Zone 0 (0-5 ft): Remove all dead vegetation and mulch from around the foundation.

- Zone 1 (5-30 ft): Thin out trees and remove "ladder fuels" (low branches that allow fire to climb).

- Wind Mitigation Link: A roof in good condition (per the new HB 815 laws of 2026) is also your best defense against embers, which cause 90% of home ignitions during a wildfire.

Why Working with an Independent Agency is Vital

The wildfire landscape in 2026 is dynamic. At Walker Insurance Agency, we provide the visibility needed to ensure your policy isn't a relic of a wetter, cheaper era.

The Walker Advantage:

- Replacement Cost Valuation: We use 2026-accurate software to ensure your Coverage A actually covers a rebuild at today's prices.

- Surcharge Protection: We shop carriers that don't penalize homeowners for temporary municipal water restrictions.

- Claims Advocacy: If you suffer smoke damage, we help navigate the new 2026 administrative resolution processes to ensure you aren't undervalued.

FAQ

1. Does my policy cover my landscaping if a wildfire burns my yard?

Standard policies have a limit (usually 5% of your dwelling coverage) for plants and trees, often capped at $500 per item. In the 2026 drought, replacing a mature landscape will likely exceed this limit.

2. Is wildfire considered an "Act of God" that I can't be canceled for?

While it is an "Act of God," frequent claims in a high-risk area can lead to non-renewal. However, under 2026 reforms, insurers must consider the condition of your home (defensible space) before denying coverage.

3. What is the "100-foot rule" in Florida insurance?

Many 2026 carriers require at least 100 feet of clearance from heavy brush to qualify for the best "Preferred" rates. If your home is closer, you may be moved to a higher-risk tier.

4. Does insurance cover a fire caused by a neighbor's "prescribed burn"?

Yes. Whether a fire is a natural wildfire or an escaped prescribed burn, your homeowners insurance provides primary coverage for your structure and belongings.

Local Business Schema

Don’t Wait for the Smoke to Clear

The 2026 drought is a historic threat to Florida property. With building costs rising and water supplies dwindling, being "mostly covered" isn't enough when the tinderbox ignites.

Get a wildfire audit today. Contact Walker Insurance Agency for a complimentary policy review. We provide the visibility you need to ensure your home survives the most dangerous fire season in decades.

[GET A FREE QUOTE TODAY]

Call us at +1-407-977-7100 or visit our office in Stuart, FL. Let us help you protect your sanctuary.

Related Articles

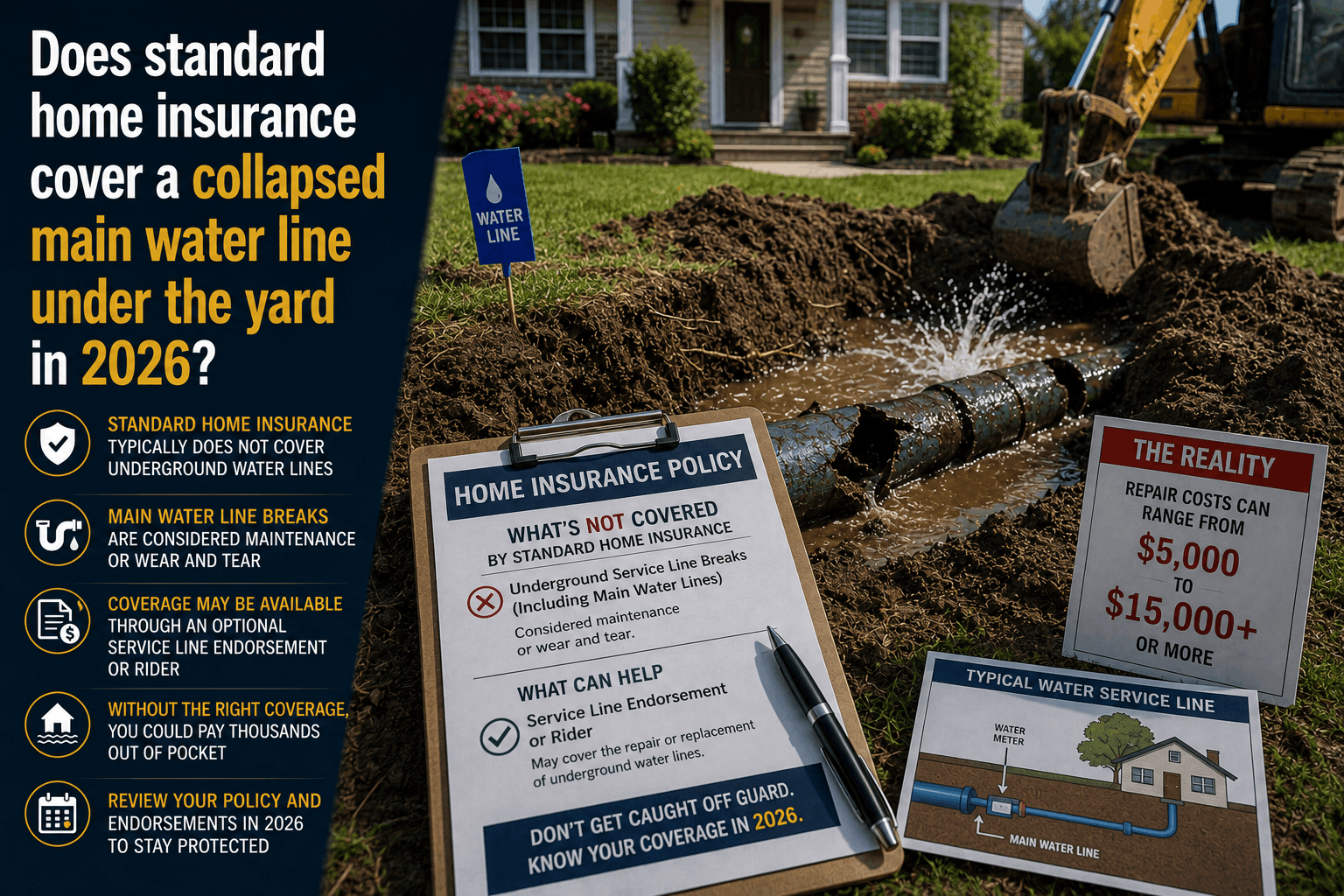

Does Home Insurance Cover a Collapsed Water Line in the Yard? (2026 Rules)

Find out if standard home insurance covers a water line collapse under your yard. Learn about the strict "slab-up" rule and the crucial Service Line Endorsement.

Read More →

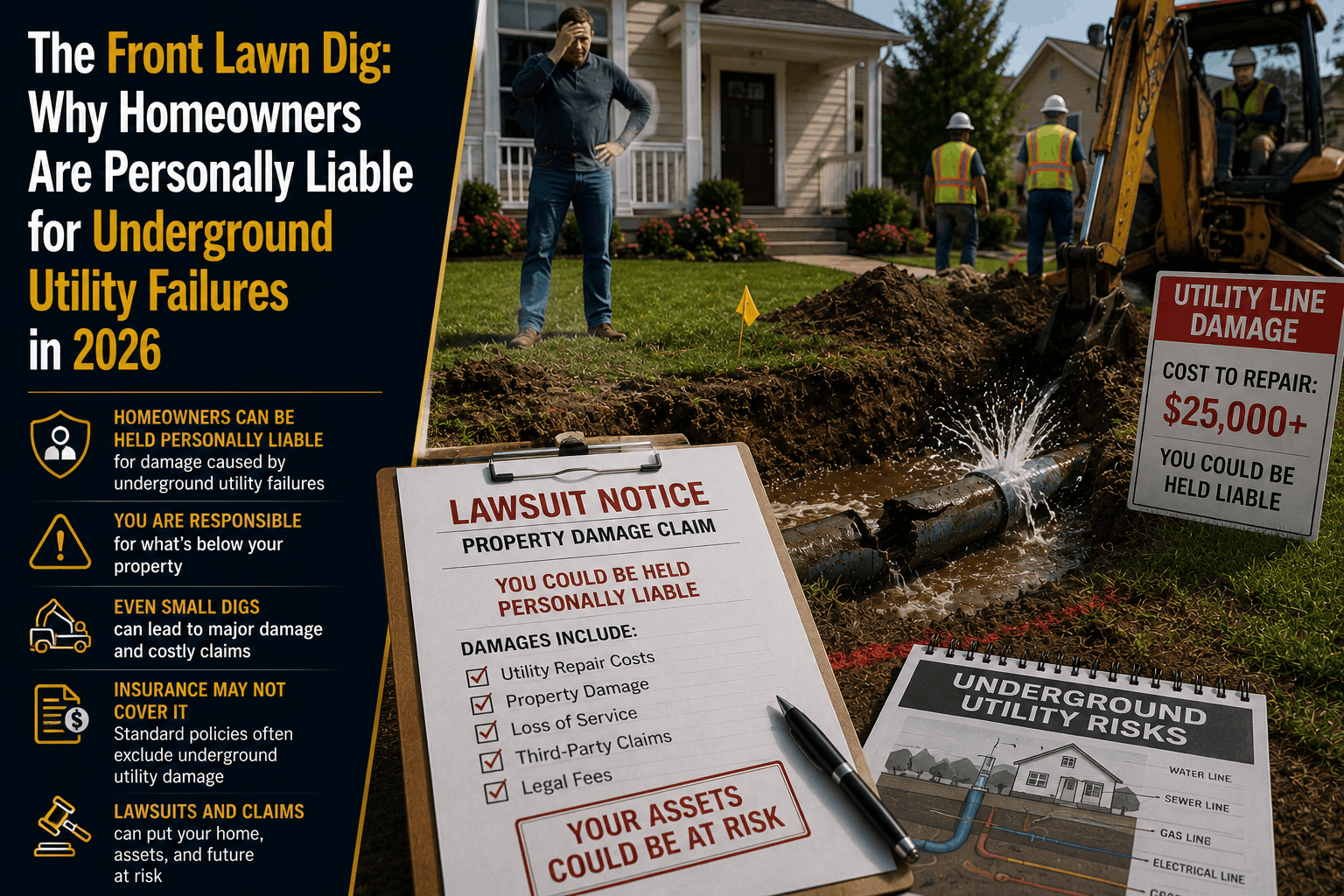

The Front Lawn Dig: Why You Own the Underground Utility Risk in 2026

Think the city pays if an underground pipe bursts under your lawn? Discover why standard Florida home insurance leaves you personally liable for buried utility lines.

Read More →

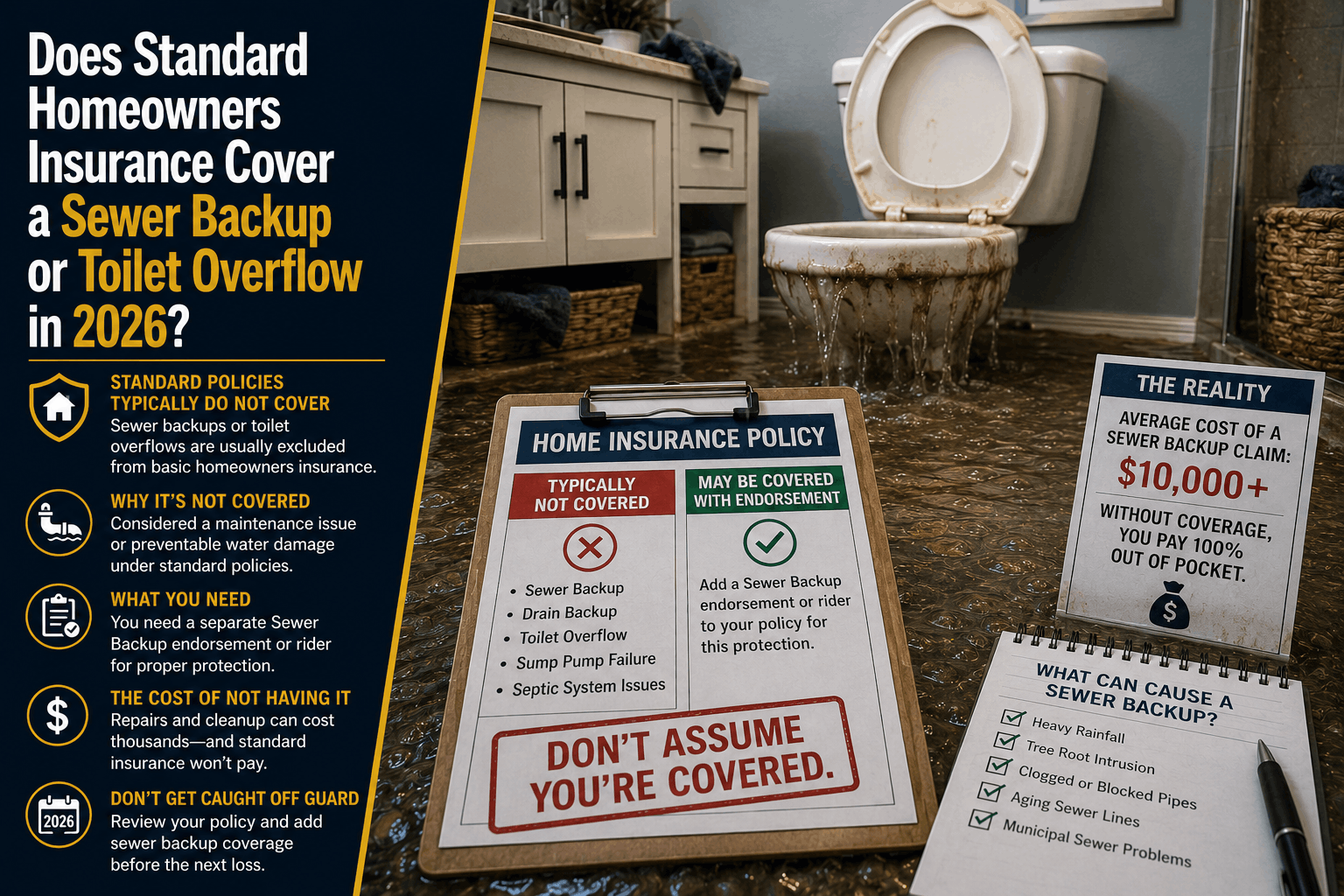

Does Homeowners Insurance Cover Sewer Backup or Toilet Overflow? (2026 Guide)

Discover how standard homeowners insurance handles sewage backups and toilet overflows in 2026\. Learn the strict rules that separate a covered claim from a denial.

Read More →