Why Florida Full Coverage Auto Insurance Fails in Hit-and-Runs

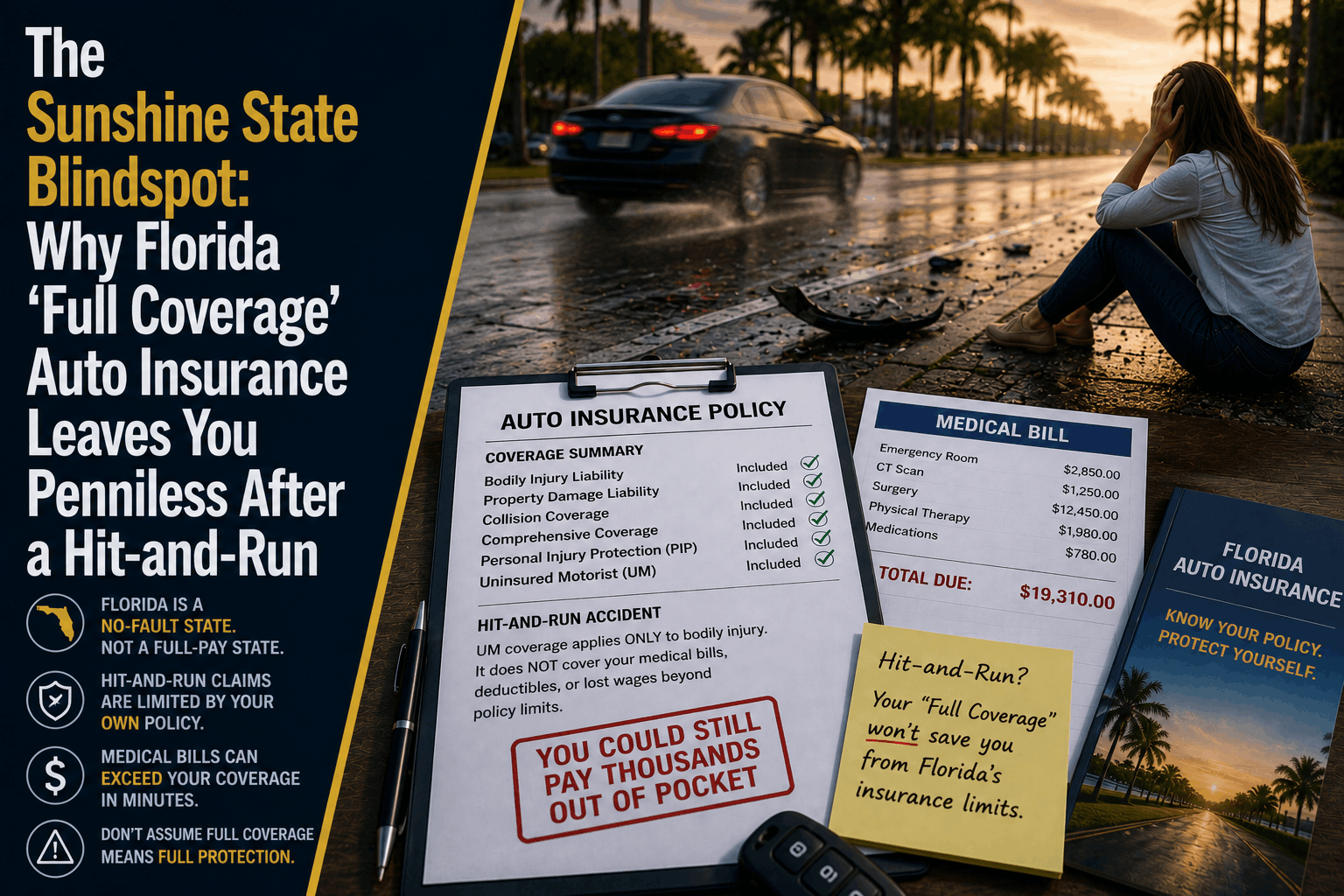

The Sunshine State Blindspot: Why Florida 'Full Coverage' Auto Insurance Leaves You Penniless After a Hit-and-Run

The Direct Answer: "Full coverage" is a marketing myth that carries no legal or standardized definition under Florida law. If you tell an insurance agent you want full coverage, they will typically give you a policy that satisfies Florida’s bare minimum legal mandates plus basic comprehensive and collision tracking. If an unidentified hit-and-run driver slams into your car and speeds away, this standard full coverage package will leave you with $0 for long-term medical care, lost wages, and pain and suffering.

Florida is a strict no-fault insurance state, and it consistently ranks as one of the worst states in the nation for uninsured motorists.

To achieve total visibility over your financial safety on the road, you must realize that if the phantom driver cannot be identified, your standard collision coverage will only fix the dented sheet metal of your vehicle. The massive medical bills, specialized physical therapy, and long-term income replacement that follow a catastrophic injury are completely excluded from traditional full coverage setups unless you have explicitly paid for Uninsured Motorist (UM) protection.

1. The Breakdown of Florida's Legally Mandated Minimums

To see where the blind spot originates, look at what the state of Florida actually requires you to carry to register a vehicle. The baseline statutory framework is highly restrictive compared to the rest of the United States:

- Personal Injury Protection (PIP): Mandated at a flat $10,000 limit. PIP pays for 80% of your necessary medical expenses and 60% of your lost wages, regardless of who caused the accident.

- Property Damage Liability (PDL): Mandated at a flat $10,000 limit. This line only pays to fix other people's property when you are at fault for a crash.

Notice what is missing from the state's mandatory framework: Bodily Injury Liability (BIL) is not legally required for standard drivers in Florida. Because thousands of drivers exploit this loophole, they cruise down the highway carrying absolutely zero coverage to pay for the medical rehabilitation of people they hit. When one of these uninsured drivers panics after a crash, they frequently flee the scene, turning a bad accident into a hit-and-run crisis.

2. Why the $10,000 PIP Limit Fails Instantly

Many drivers assume that if they are hurt by a runaway vehicle, their internal PIP coverage will foot the bill. In reality, a $10,000 medical cap disappears within the first hour of entering an emergency room.

Furthermore, Florida enforces a strict 14-day medical care rule. If you do not seek formal medical evaluation within 14 days of the hit-and-run, your PIP benefit drops to exactly $0.

Even if you seek immediate care, if a physician determines that you did not suffer an Emergency Medical Condition (EMC), your PIP coverage limit is automatically slashed from $10,000 down to a cap of $2,500. With modern medical inflation, a single diagnostic MRI scan or an ambulance ride will completely exhaust that balance, leaving you directly responsible for the remaining financial overhead.

3. How to Erect an Ironclad Auto Safety Shield

If your vehicle profile is currently floating on a standard corporate auto policy without customized selections, your family's financial stability is entirely exposed to the next reckless driver.

To safely insulate your personal wealth, you must instruct your independent agent to reconstruct your policy using a precise, three-step protective layout:

Step 1: Maintain Collision Coverage to repair the vehicle's physical sheet metal

Step 2: Maximize Bodily Injury limits to protect your liability exposures

Step 3: Add STACKED Uninsured Motorist (UM) Coverage to pay for your actual body

===================================================================================

= 100% Comprehensive Financial Protection Against Phantom and Hit-and-Run Drivers

- The Contractual Shield: You must formally add Uninsured/Underinsured Motorist (UM) Coverage to your auto line. UM coverage acts as an exact financial mirror of the missing at-fault driver. If a hit-and-run driver strikes your vehicle and escapes, your UM coverage steps into their shoes. It pays for 100% of your medical expenses above the PIP threshold, covers your ongoing lost income, and compensates you for non-economic damages like pain and suffering.

- The Stacked Advantage: When selecting your UM limits, always choose the Stacked option rather than non-stacked. In Florida, stacking allows you to multiply your UM protection limits by the number of vehicles insured under your household policy. If you have two cars insured at a $50,000/$100,000 limit, stacking combines them into an ironclad $100,000/$200,000 pool of medical protection available for any single accident.

Why Working with an Independent Agency is Vital

Attempting to manage your auto assets through a generic smartphone app or an automated corporate internet form leaves you completely exposed to the fine-print realities of Florida insurance guidelines. At Walker Insurance Agency, we provide the personalized, data-driven visibility you need to navigate the state's unique insurance market.

The Walker Advantage:

- Deep Portfolio Line Audits: We break down your policy documents line-by-line to ensure you haven't mistakenly signed a UM rejection waiver form.

- Asset Exposure Matching: We align your UM and medical payment thresholds with your actual household net worth and health insurance deductibles.

- Florida Market Navigation: As the domestic insurance market continues to evolve, we continuously shop your risk profile across premier private underwriters to secure the highest stacked liability thresholds at the lowest available premium floors in Stuart.

FAQ

1. If a hit-and-run driver damages my parked car while I am shopping, does my collision insurance pay for it?

Yes. If your vehicle is hit while parked and the driver flees, your Collision Coverage line will pay to repair the physical damage to your car. However, you will still be required to pay your standard out-of-pocket collision deductible (typically $500 or $1,000) before the repair shop will release your keys, unless local law enforcement catches the phantom driver and verifies their insurance data.

2. Is Uninsured Motorist coverage expensive to add to a Florida auto policy?

While UM coverage does add an extra premium charge because it forces your carrier to assume a massive amount of medical risk, it represents the highest value-to-cost ratio in the insurance industry. For the price of a couple of fast-food meals a month, you convert a policy that only fixes plastic bumpers into a robust medical safety net that can prevent personal bankruptcy after a severe crash.

3. What should I do immediately at the scene if I am involved in a hit-and-run collision in Stuart?

Safety is your top priority—move your vehicle to a secure shoulder if possible. Try to instantly memorize or dictate into your phone any identifying details of the fleeing vehicle: the license plate number (even a partial match helps), the make, model, color, and any unique bumper stickers or window damage. Call 911 immediately to get a state or local officer on the scene to file an official report, and look for nearby commercial buildings or traffic intersections that might have captured the incident on security cameras.

Insulate Your Personal Wealth Before Your Next Commute

Driving on Florida roads without checking your policy's fine print is an administrative gamble that can instantly compromise your family's economic survival. True peace of mind requires pulling back the curtain on marketing buzzwords like "full coverage" and replacing them with verified, high-limit protection.

Take control of your road safety today. Contact Walker Insurance Agency for a comprehensive portfolio evaluation. We provide the visibility you need to eliminate hidden legal blind spots, deploy high-limit stacked UM riders, and protect your hard-earned wealth safely in Stuart.

[GET A FREE AUTO QUOTE TODAY]

Call our personal lines division at +1-407-977-7100 or visit our office in Stuart, FL. Let us safeguard your vehicle boundaries today.

Related Articles

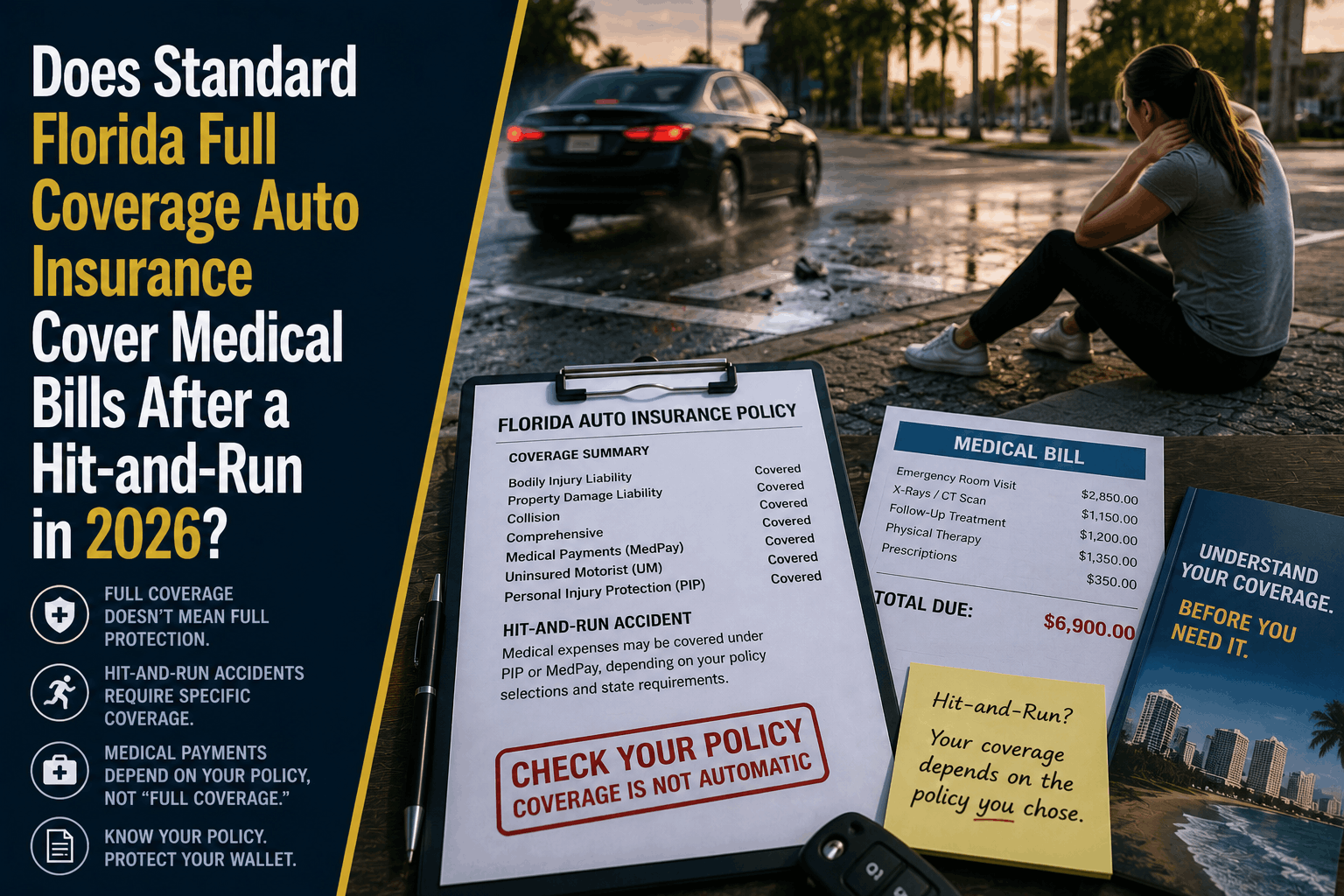

Does Florida Full Coverage Pay Medical Bills in a Hit-and-Run?

Relying on Florida "full coverage" auto insurance to pay your medical bills after a hit-and-run in 2026? Discover why it fails and leaves you broke.

Read More →

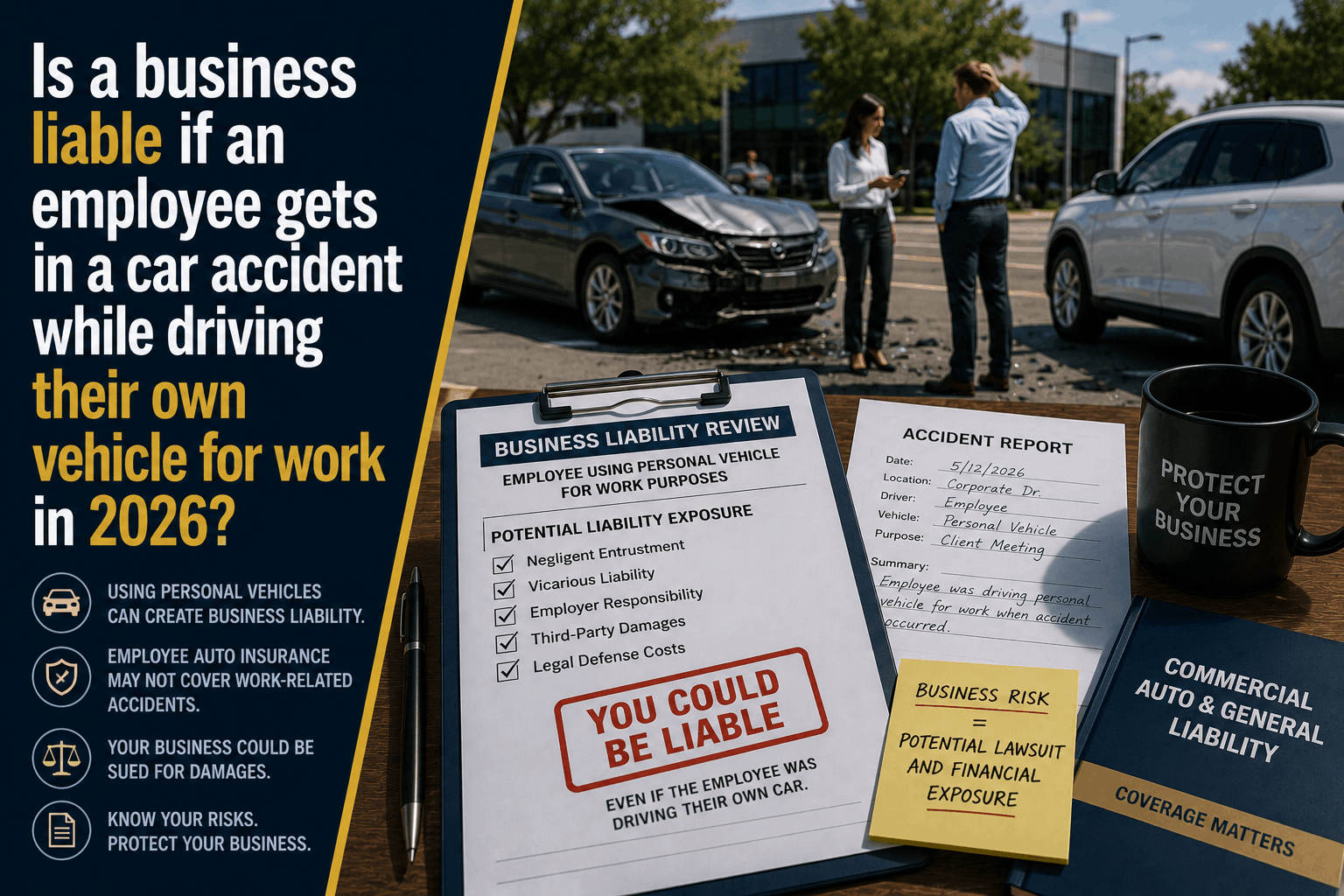

Is a Business Liable If an Employee Crashes a Personal Car for Work?

Discover your corporate liability if an employee causes a car accident while driving their own vehicle for work in 2026\. Learn about the HNOA loophole.

Read More →

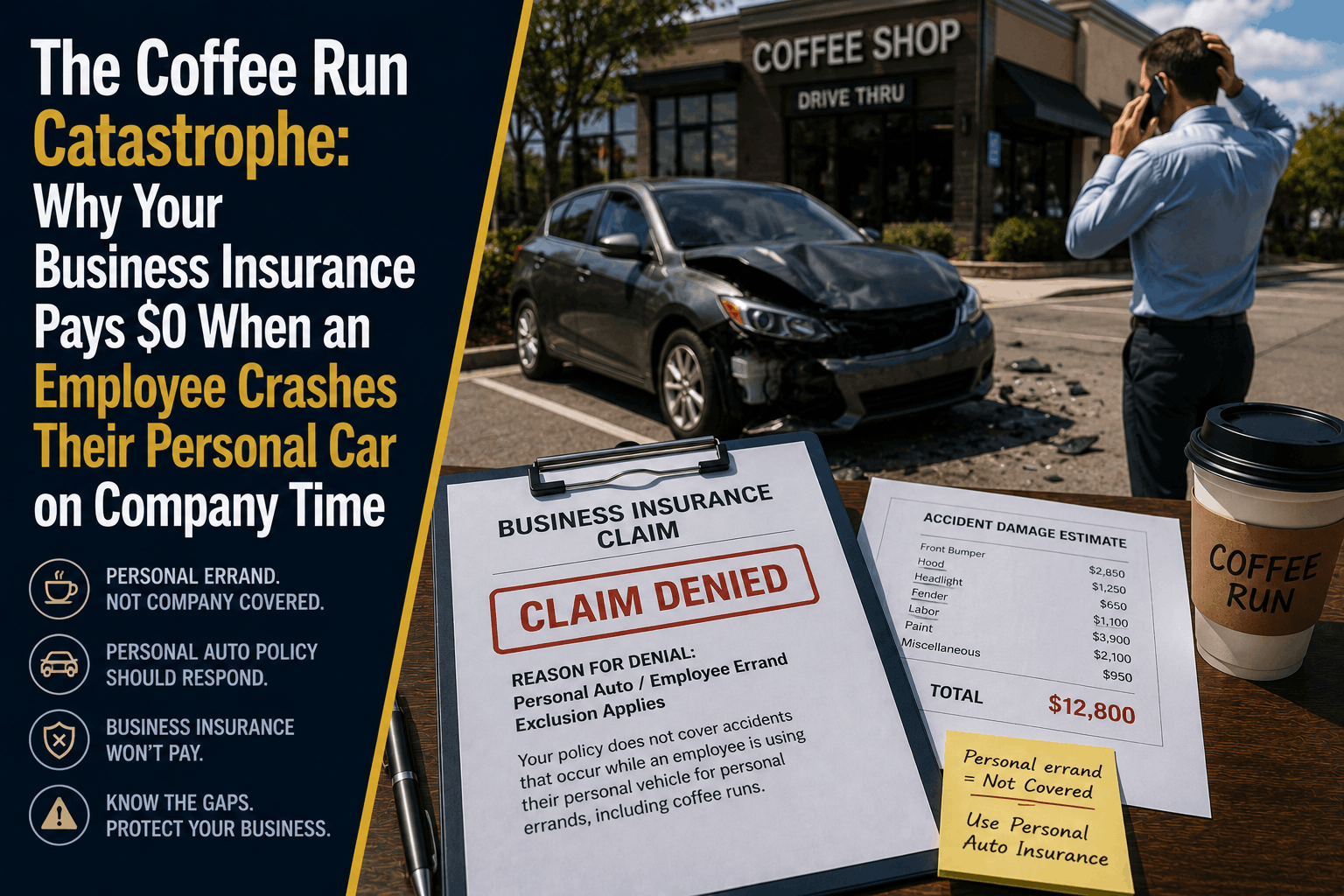

The Coffee Run Catastrophe: Hired & Non-Owned Auto Policy Gaps

If an employee crashes their personal vehicle while running a business errand, your standard insurance pays $0. Discover the Hired & Non-Owned Auto loophole.

Read More →