Does Florida Full Coverage Pay Medical Bills in a Hit-and-Run?

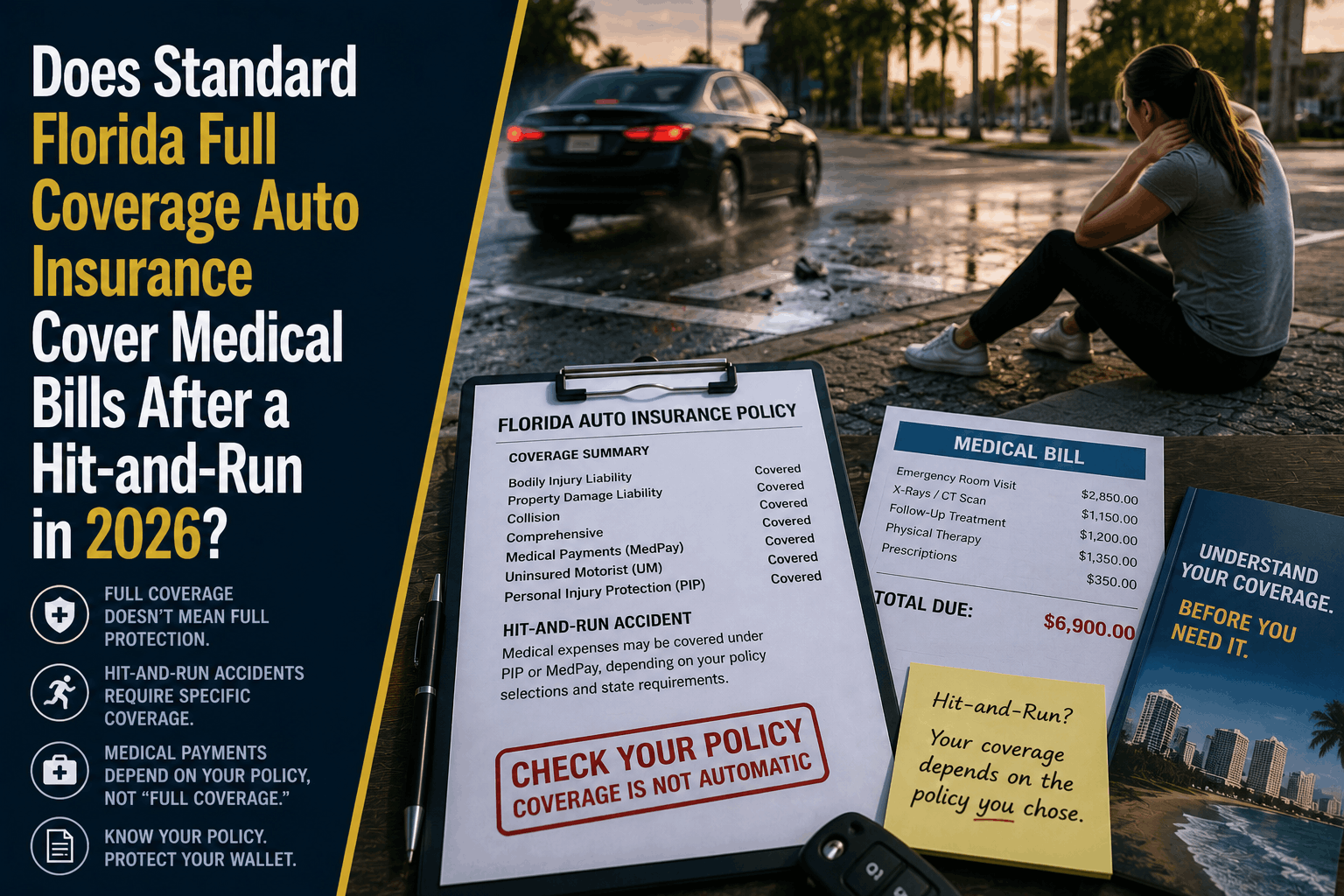

Does Standard Florida Full Coverage Auto Insurance Cover Medical Bills After a Hit-and-Run in 2026?

The Direct Answer: No, standard Florida "full coverage" auto insurance does not cover your long-term medical bills after a hit-and-run. The term "full coverage" is a highly dangerous marketing myth with zero legal definition. If you buy a standard full coverage policy in Florida, it typically only includes the bare state mandates plus comprehensive and collision to fix your car. If an unidentified driver hits you and speeds away, your standard policy leaves you with $0 for severe medical bills, ongoing physical therapy, or lost income.

Florida remains a strict no-fault insurance state, where every driver's own policy pays out first after a collision.

To achieve total visibility over your personal finances on the road, you must realize that if the runner is never caught, your standard full coverage path stops dead once your tiny, mandatory medical limits are exhausted. Without explicitly adding Uninsured Motorist (UM) protection to your portfolio, you are personally responsible for every dollar of medical debt that follows.

1. The 14-Day Rule & The $10,000 PIP Ceiling

Because Florida operates under a no-fault system, your basic medical recovery relies on Personal Injury Protection (PIP). Every standard policy includes it, but it features a massive structural trap:

- The 14-Day Treatment Deadline: Under Florida Statutes § 627.736, you must seek formal medical care within exactly 14 days of the hit-and-run. If you wait 15 days because you thought your neck pain would fade, your insurer will legally deny your medical benefits completely.

- The Emergency Medical Condition (EMC) Bottleneck: Even if you beat the 14-day clock, your PIP line will only pay out the full $10,000 limit if a physician formally diagnoses you with an Emergency Medical Condition. If your injuries are classified as non-emergency, your PIP medical benefit is automatically capped at just $2,500.

Furthermore, PIP only pays 80% of your medical expenses. With modern medical inflation, a single ambulance transport, emergency room evaluation, and diagnostic MRI scan will completely exhaust that balance before you ever receive treatment.

2. Why Collision Coverage Won't Fix Your Body

Many drivers feel a false sense of security because they see "Collision Coverage" on their insurance declarations page. It is vital to separate your vehicle's structural metal from your actual physical health:

- Collision protects the sheet metal: If a phantom vehicle crushes your rear bumper and flees, your collision policy will pay to fix or replace your car, minus your out-of-pocket deductible ($500 or $1,000).

- Collision pays $0 for bodily injury: It cannot be used to pay for surgeries, chiropractic adjustments, prescription medications, or the permanent lost wages caused by a reckless driver.

Because Florida law does not require drivers to buy Bodily Injury Liability (BIL) to cover other people, an unprecedented number of motorists carry zero injury protection. When they hit you, they panic and flee the scene, turning your morning commute into an uninsured financial crisis.

3. How to Erect an Ironclad Medical Safety Shield

If your vehicle's protection structure is currently resting on a baseline contract with zero custom riders, your household wealth is exposed to every hit-and-run driver on the road.

At Walker Insurance Agency, we advise clients to eliminate this exposure using a precise, high-limit policy layout:

Step 1: Keep Collision Coverage active to settle vehicle physical damages

Step 2: Add Medical Payments (MedPay) to absorb the 20% out-of-pocket PIP gap

Step 3: Bind STACKED Uninsured Motorist (UM) Coverage to protect your actual body

===================================================================================

= 100% Comprehensive Financial Protection Against Phantom and Hit-and-Run Crashes

- The Contractual Shield: You must formally add Uninsured/Underinsured Motorist (UM) Coverage to your auto line. In a hit-and-run where the at-fault driver escapes and cannot be identified, UM coverage steps directly into the shoes of the phantom vehicle's missing insurance. It pays for 100% of your past and future medical expenses above the PIP threshold, covers your lost income, and compensates you for non-economic damages like pain, suffering, and permanent scarring.

- The Stacked Advantage: When setting up your UM protection, always choose Stacked UM. In Florida, stacking allows you to multiply your coverage limits by the number of vehicles insured under your household policy. If you have two cars on a policy with a $50,000 limit, stacking combines them into a $100,000 pool of clean medical funding available for a single crash.

Why Working with an Independent Agency is Vital

Attempting to manage your primary auto assets through a generic smartphone application or automated online form ensures you will miss the critical regional riders needed to survive a hit-and-run. At Walker Insurance Agency, we provide the personalized, data-driven visibility you need to secure your financial safety.

The Walker Advantage:

- Waiver Verification Audits: We review your policy files line-by-line to ensure you haven’t unknowingly signed a state-approved UM rejection form.

- MedPay Alignment: We embed optional Medical Payments (MedPay) riders to automatically pick up the 20% co-insurance gap that standard PIP leaves behind.

- Strategic Market Sifting: As the domestic insurance market continues to stabilize, we continuously shop your profile across premier private underwriters to locate providers offering the highest stacked UM limits at the absolute lowest available premium floors in Stuart.

FAQ

1. If a hit-and-run driver strikes me while I am walking or riding a bicycle, does my auto insurance still apply?

Yes. In Florida, your personal auto insurance policy’s PIP and Uninsured Motorist (UM) coverages are highly portable. If you or a resident relative are struck as a pedestrian or a cyclist by a phantom vehicle, your own auto policy covers your medical bills and bodily injuries exactly as if you were sitting inside your car.

2. Can I use my regular private health insurance to pay for car accident injuries instead of auto insurance?

Only as a secondary layer. In Florida, auto PIP is contractually designated as the primary payer for car accident injuries. Your health insurance provider will legally refuse to process or pay your emergency medical bills until your auto carrier issues a "PIP Exhaustion Letter" proving that your auto policy limits have been completely drained to $0.

3. What critical evidence do I need to preserve to ensure my insurance carrier doesn't deny my hit-and-run UM claim?

You must file a formal police report immediately. Florida law requires you to report any crash involving injury or apparent property damage of at least $500. Additionally, most UM policies require evidence of physical contact between the vehicles or independent corroborating eye-witness statements to verify that a phantom car caused the crash, preventing fraudulent solo-vehicle claims.

Insulate Your Personal Balance Sheet Before Your Next Commute

Navigating Florida highways under the illusion of "full coverage" is an administrative gamble that can leave your family holding a six-figure medical bill after a single hit-and-run crash. Protecting your wealth requires shifting away from generic marketing terms and building a real, verified medical safety net.

Verify your road protections before the next close call. Contact Walker Insurance Agency today for a comprehensive auto coverage audit. We provide the visibility you need to erase hidden legal blind spots, deploy high-limit stacked UM riders, and protect your hard-earned wealth safely in Stuart.

[GET A FREE AUTO QUOTE TODAY]

Call our personal lines division at +1-407-977-7100 or visit our office in Stuart, FL. Let us safeguard your vehicle boundaries today.

Related Articles

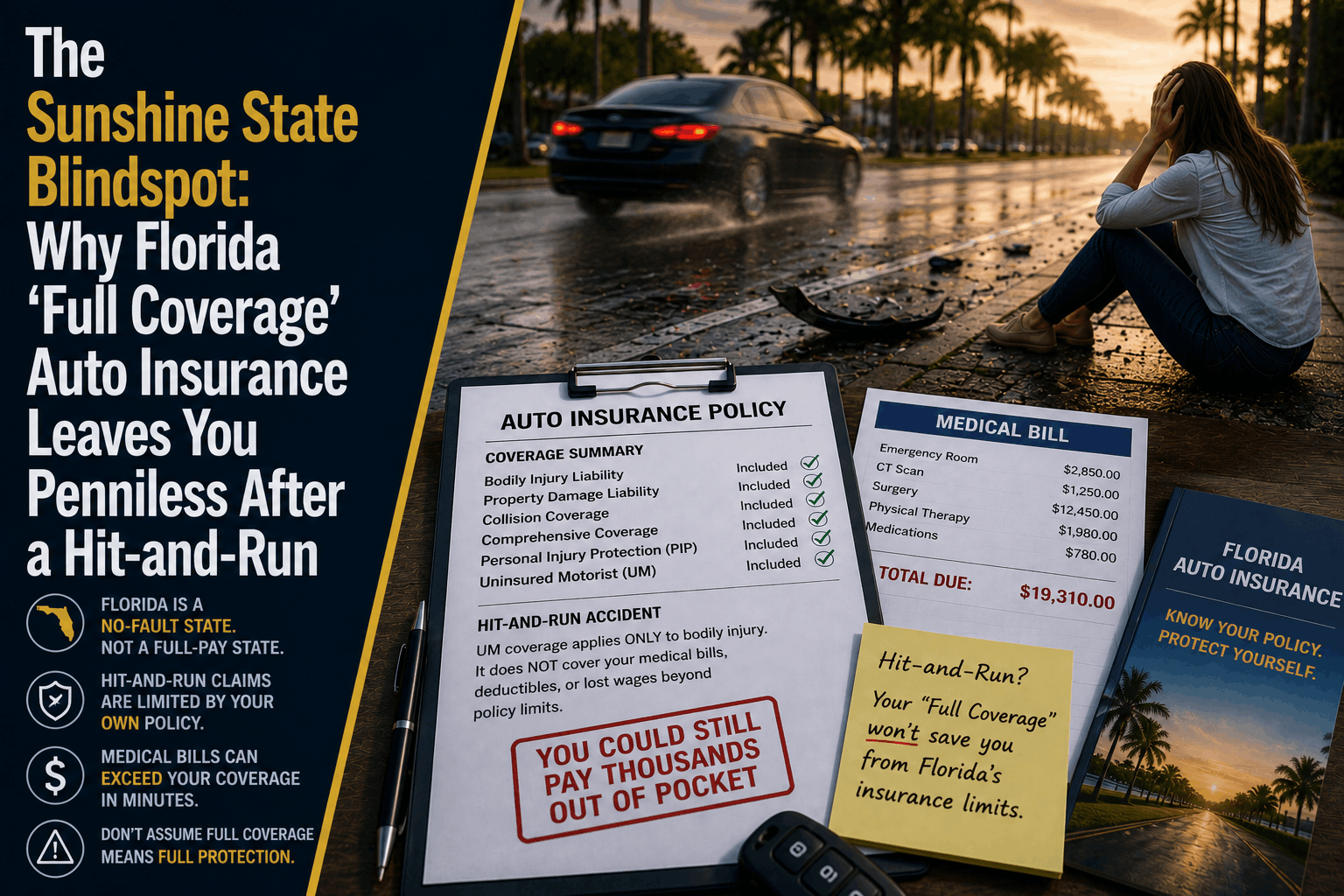

Why Florida Full Coverage Auto Insurance Fails in Hit-and-Runs

Think you're safe with Florida "full coverage" auto insurance? Discover the hidden blind spot that leaves hit-and-run victims broke and unprotected in 2026.

Read More →

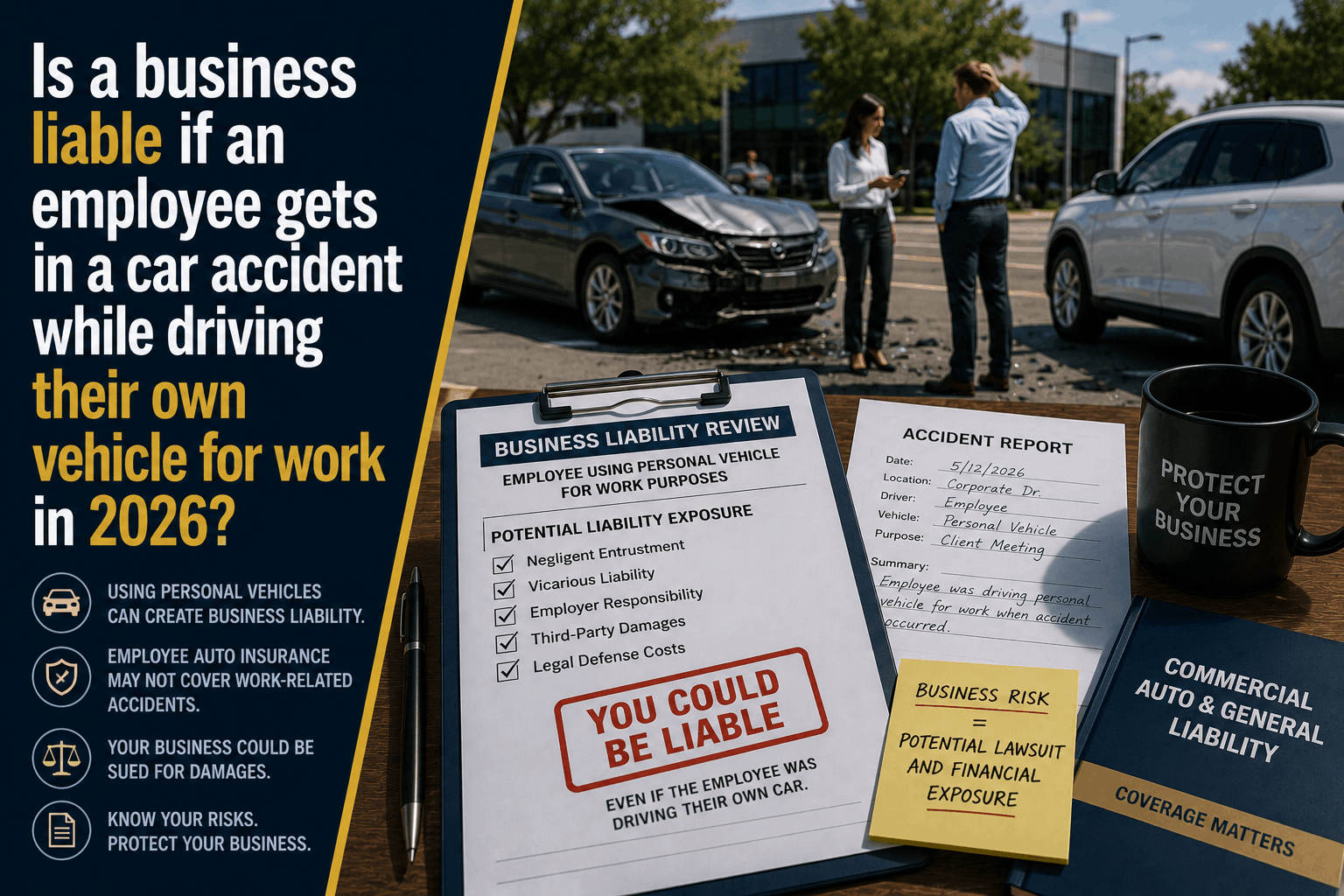

Is a Business Liable If an Employee Crashes a Personal Car for Work?

Discover your corporate liability if an employee causes a car accident while driving their own vehicle for work in 2026\. Learn about the HNOA loophole.

Read More →

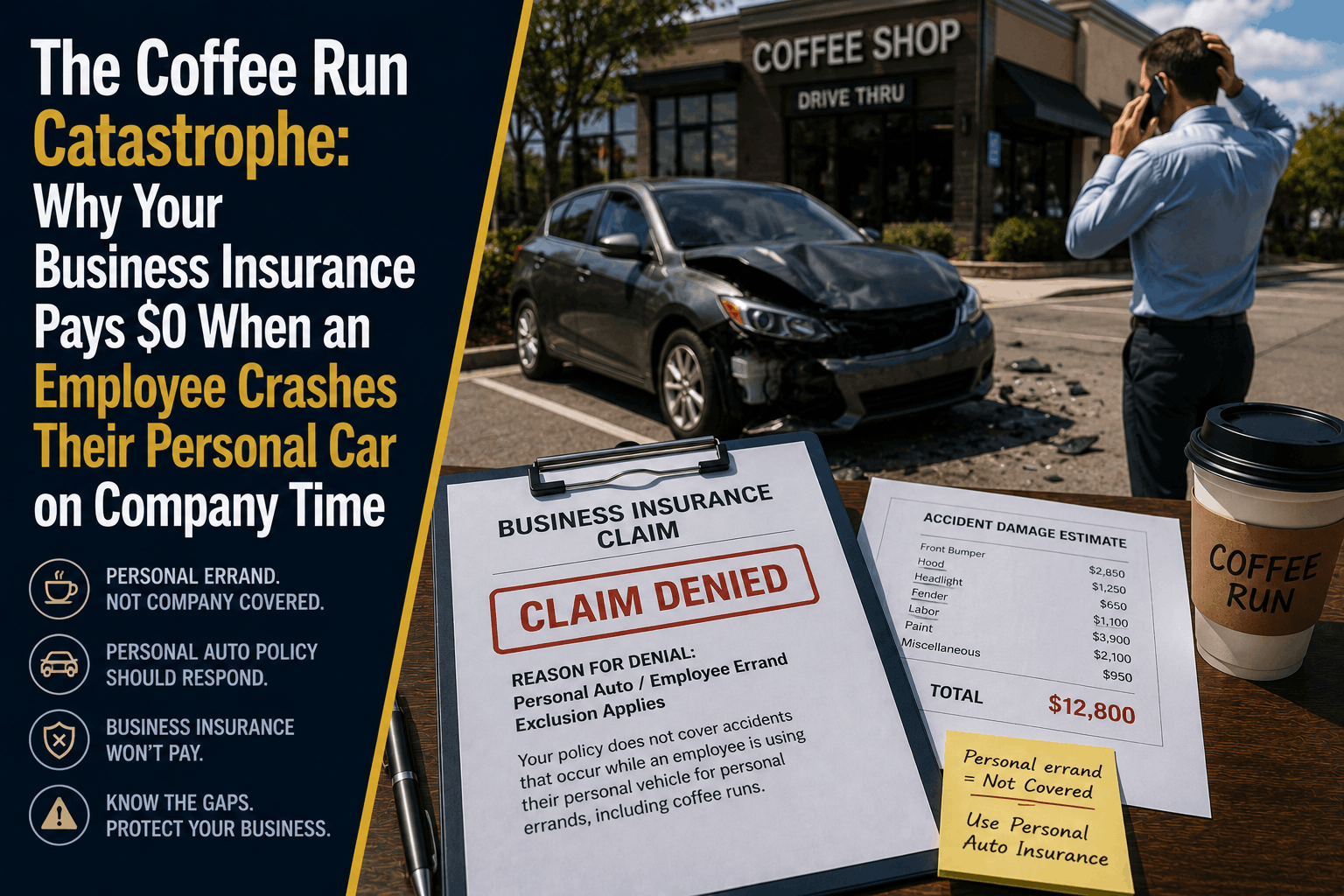

The Coffee Run Catastrophe: Hired & Non-Owned Auto Policy Gaps

If an employee crashes their personal vehicle while running a business errand, your standard insurance pays $0. Discover the Hired & Non-Owned Auto loophole.

Read More →