What Is the Most Misunderstood Part of Car Insurance? | Florida Guide

What Is the Most Misunderstood Part of a Car Insurance Policy?

Navigating car insurance in Florida often feels like learning a second language. Between state-mandated requirements and the marketing terms used by large carriers, it is easy to get lost in the fine print. For many drivers in Stuart and across the Sunshine State, the most misunderstood part of a car insurance policy isn't just a single clause—it’s the fundamental gap between what they think they have and what they actually have.

Understanding these nuances is the difference between a seamless recovery and a financial disaster after an accident. To achieve true financial visibility, you must look beyond the premium price and understand exactly how your assets are protected. In this guide, we break down the most common points of confusion to ensure you are never left vulnerable.

The Myth of "Full Coverage" vs. Reality

The term "Full Coverage" is perhaps the most deceptive phrase in the insurance industry. Many Florida drivers believe that if they have full coverage, they are protected against every possible scenario.

The Reality:

"Full Coverage" is not a specific policy; it is typically just a combination of Comprehensive and Collision coverage required by lenders. It does not automatically include:

- Uninsured Motorist (UM): Protection if someone hits you who has no insurance.

- Medical Payments (MedPay): Coverage beyond the basic PIP limits.

- Gap Insurance: Coverage for the difference between your car's value and your loan balance.

- Rental Reimbursement: A car to drive while yours is in the shop.

Liability Coverage: What You Owe vs. What You Get

Liability insurance is frequently misunderstood as protection for the policyholder. In reality, Liability coverage is designed to protect other people from the damage you cause.

Factors that affect your liability risk:

- Bodily Injury (BI): In Florida, this is often optional but highly recommended. Without it, you are personally responsible for the medical bills of anyone you injure.

- Property Damage (PD): This covers the other person’s car or property. With the rising cost of modern vehicles, a $10,000 limit (the state minimum) is rarely enough.

- Legal Defense: A major misunderstood benefit of liability coverage is that it often pays for your legal defense if you are sued after an accident.

Why Personal Injury Protection (PIP) is Often Confusing

Florida is a "No-Fault" state, which leads to the myth that you can't sue or be sued. This is entirely incorrect. PIP is designed to provide immediate medical coverage regardless of who caused the accident, but it has strict limitations.

Practical constraints of PIP:

- The 80/20 Rule: PIP only pays 80% of medical bills and 60% of lost wages.

- The $10,000 Limit: This limit hasn't changed in decades, while healthcare costs have skyrocketed.

- The 14-Day Rule: You must seek medical treatment within 14 days of the accident to qualify for PIP benefits.

Uninsured Motorist Coverage: The Essential "Invisible" Protection

Many drivers assume that because insurance is mandatory, everyone has it. However, Florida has one of the highest rates of uninsured motorists in the country.

Why you need UM coverage:

- Protecting Yourself: UM coverage steps in to pay for your medical bills, lost wages, and pain and suffering when the at-fault party has no insurance or flees the scene.

- Stacked vs. Unstacked: A misunderstood technicality that allows you to combine coverage limits if you own multiple vehicles, providing a much larger safety net for your family.

Why Working with an Independent Agency Makes the Difference

Choosing insurance based on a TV commercial can leave you with massive gaps. At Walker Insurance Agency, we focus on providing the visibility that automated systems ignore.

Practical Benefits:

- Custom Risk Assessment: We look at your total assets to recommend limits that actually protect you from lawsuits.

- Policy Audits: We explain the "fine print" in plain English, so you know exactly what "Full Coverage" means for you.

- Local Support: When an accident happens in Stuart or anywhere in Florida, you talk to a local expert, not a call center.

FAQ

1. Is "Full Coverage" required by law in Florida?

No. Florida law only requires PIP and Property Damage Liability. However, if you have a loan or lease on your vehicle, your lender will require Comprehensive and Collision coverage.

2. Does my insurance cover me if I’m driving someone else’s car?

In most cases, insurance follows the vehicle, not the driver. However, specific policy exclusions can apply, so it is vital to verify your "Permissive Use" clauses.

3. What is a deductible, and how does it work?

A deductible is the amount you pay out of pocket before your insurance kicks in for Comprehensive or Collision claims. Higher deductibles lower your premium but increase your immediate costs after an accident.

4. Will my rates go up if I file a claim that wasn't my fault?

In Florida, insurers generally cannot raise your rates solely for a "no-fault" accident. However, losing a "claims-free discount" can still result in a higher premium.

Local Business Schema

Don’t Drive with Blind Spots

Misunderstanding your policy is the same as being uninsured for the risks you face. In Florida’s high-traffic environment, you can’t afford to guess about your protection.

Get the clarity you deserve. Contact Walker Insurance Agency today for a personalized policy review. We will help you identify the gaps in your "Full Coverage" and provide the visibility you need to drive with confidence.

[GET A FREE QUOTE TODAY]

Call us at +1-772-247-0269 or visit our office in Stuart, FL. Experience the difference of having an agent who treats your protection as their priority.

Related Articles

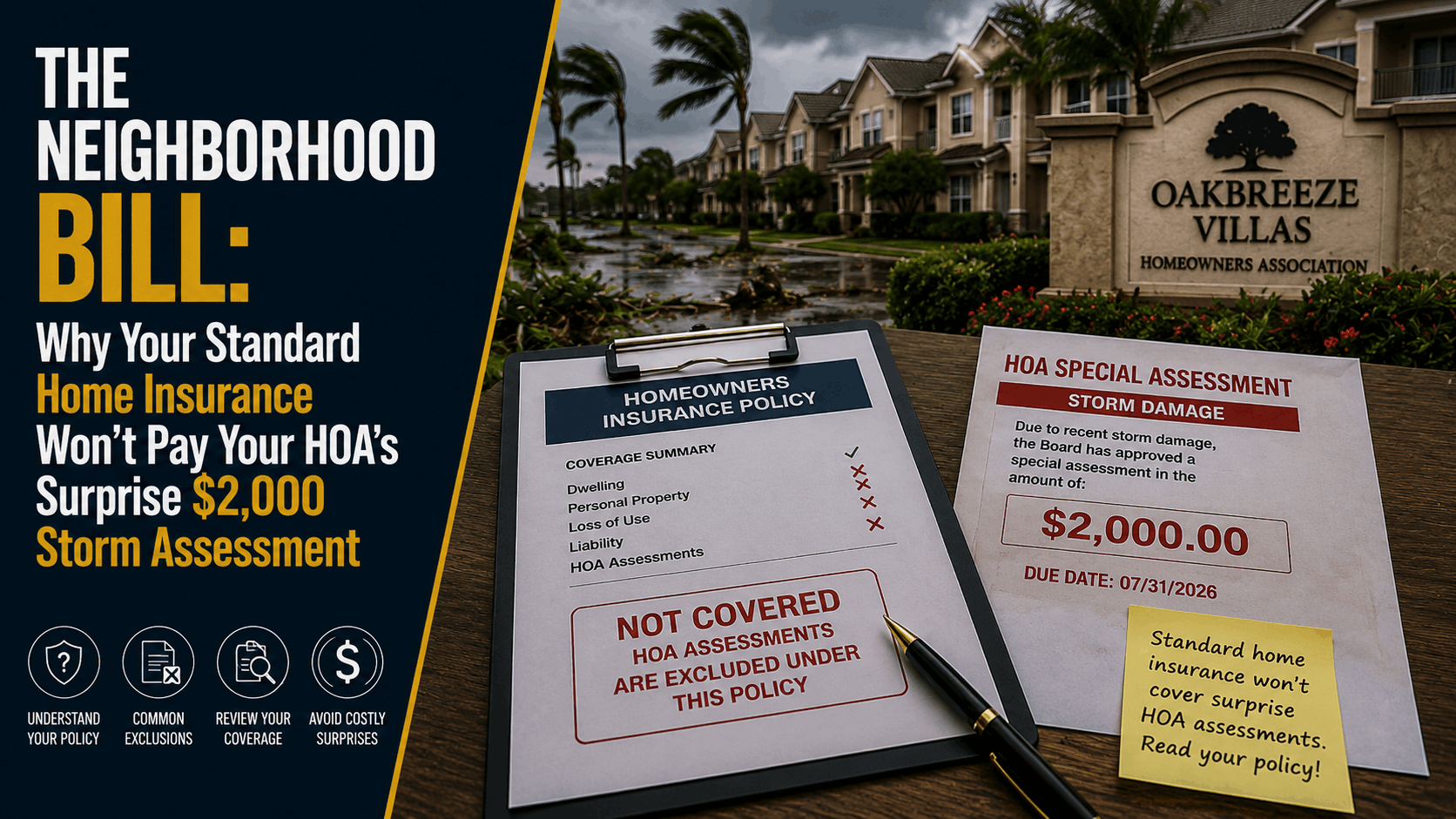

Why Home Insurance Won't Pay Your HOA Storm Assessment (2026)

Received a surprise HOA special assessment after a storm? Discover the critical loss assessment loopholes leaving Stuart homeowners completely exposed in 2026.

Read More →

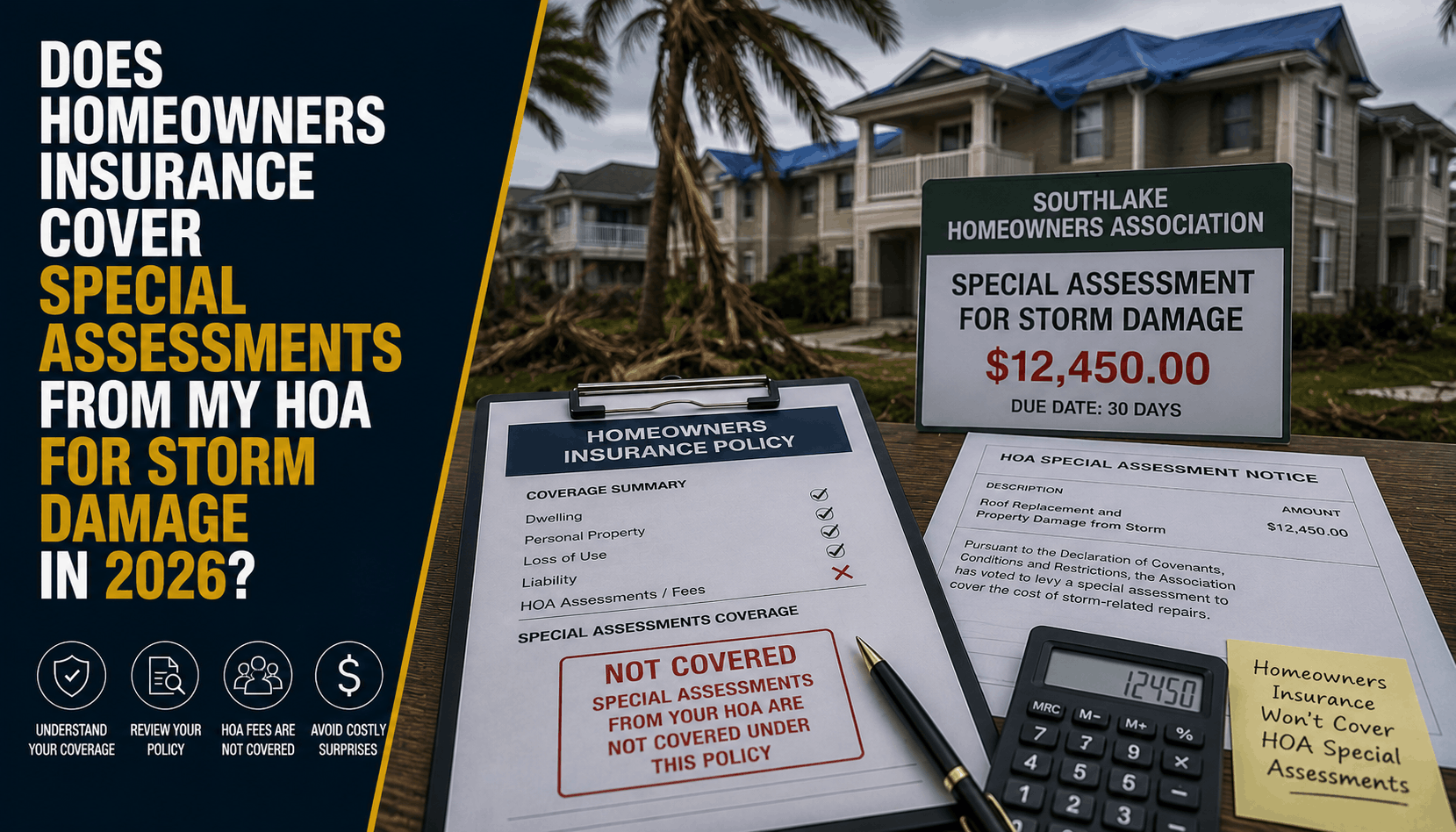

Does Florida Home Insurance Cover HOA Storm Special Assessments? (2026)

Think your Stuart home or condo insurance automatically covers an HOA special assessment after a hurricane? Discover the loss assessment limits leaving local owners exposed.

Read More →

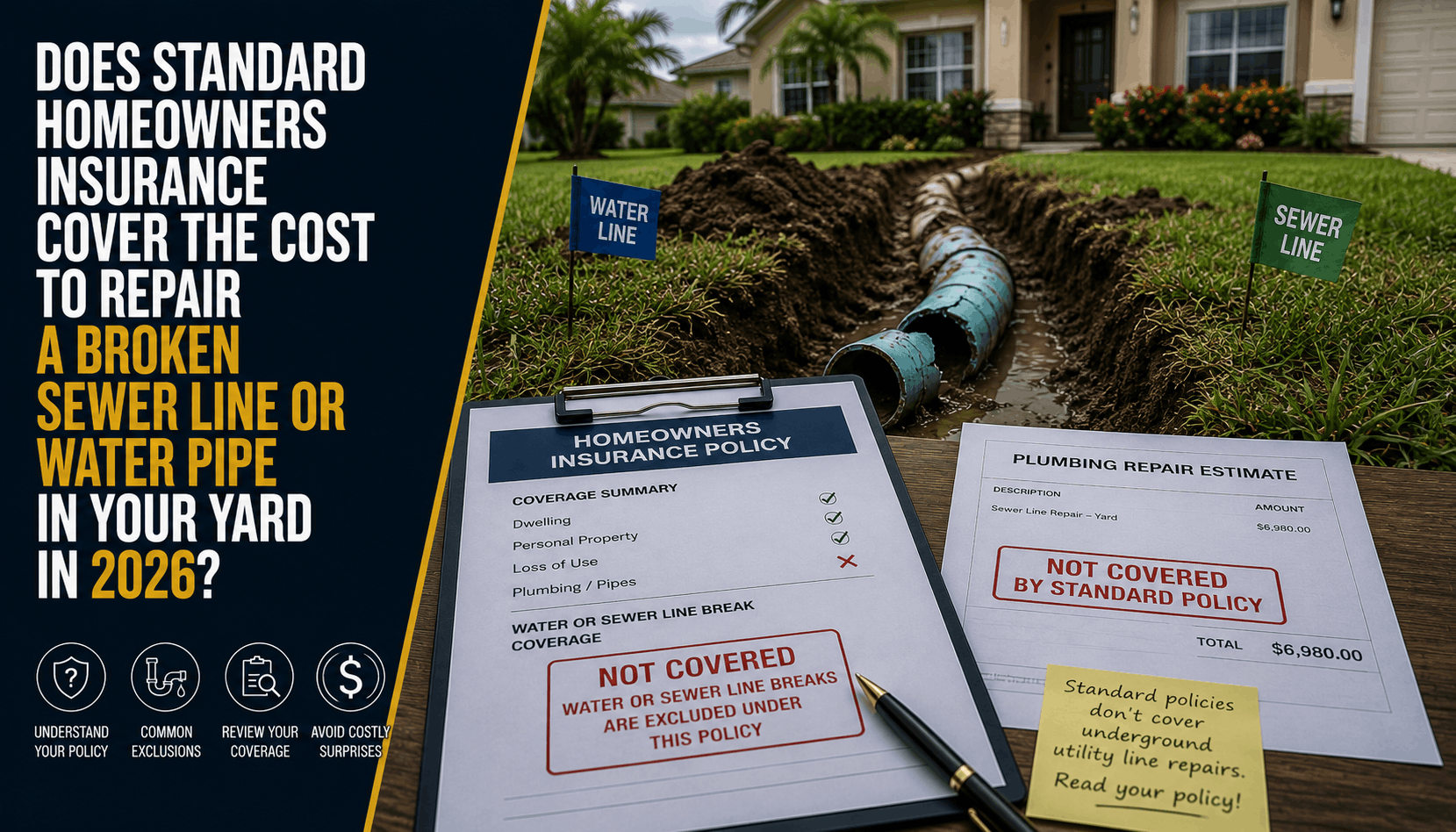

Does Home Insurance Cover Broken Pipes in the Yard? (2026)

Discover why standard homeowners insurance completely denies the cost to repair a broken sewer line or water main in your yard, and how Stuart homeowners can fix this gap.

Read More →