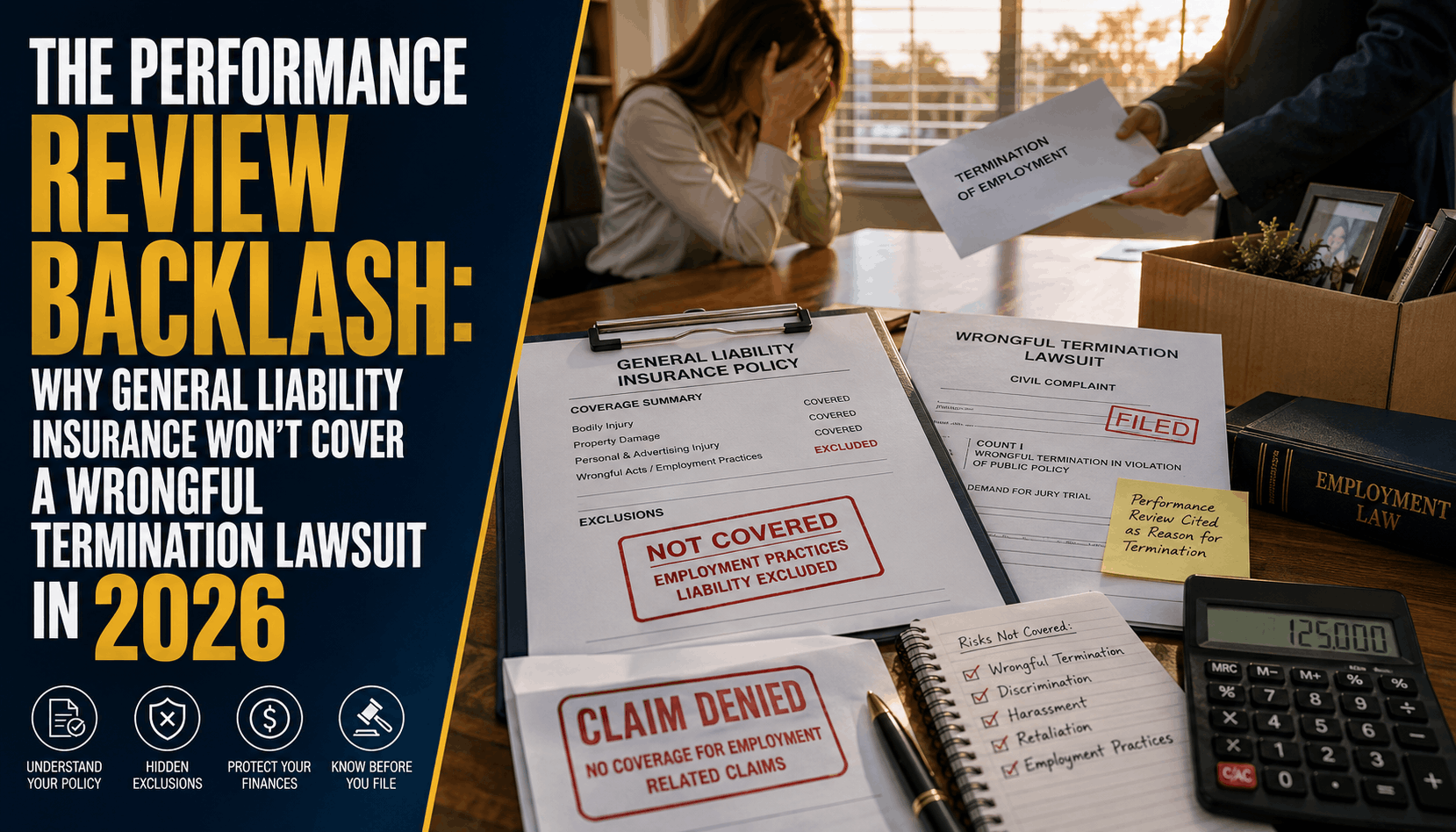

The Performance Review Backlash: Why General Liability Voids Employee Suits

The Performance Review Backlash: Why General Liability Insurance Won't Cover a Wrongful Termination Lawsuit in 2026

The Direct Answer: A standard Commercial General Liability (CGL) insurance policy will completely refuse to cover, defend, or pay for a wrongful termination lawsuit. There is a massive, high-risk misunderstanding among business owners who assume that because they carry "General Liability," their corporate entity is blanketed against any and all incoming civil litigation.

In 2026, as workplace dynamics grow increasingly complex and automated performance analytics trigger severe employee pushback, insurance carriers are holding an absolute, unyielding line: General Liability contracts are designed exclusively to protect your business against third-party claims of Bodily Injury (e.g., a customer slipping on a wet floor) and Property Damage (e.g., an employee accidentally breaking a client's equipment).

Workplace disputes, administrative firings, and performance review backlashes fall strictly into corporate management risks. If a terminated worker sues your company for wrongful dismissal, your standard CGL carrier will issue an immediate, automated Coverage Exclusion Denial, leaving your business to fund a multi-thousand-dollar legal defense entirely out of pocket.

1. The Anatomy of a CGL Employee Claim Denial

When an underperforming employee is let go following a negative performance evaluation, the resulting legal backlash rarely involves physical injuries. Instead, the ex-employee’s legal counsel drafts a civil complaint alleging emotional distress, breach of contract, discrimination, or unlawful retaliation.

When you forward this legal summons to your commercial general liability adjuster, they will systematically cross-examine the claim against the core definitions of your policy jacket:

[Claim: Client Breaks a Leg in Your Lobby] ───> 100% COVERED (True Bodily Injury Peril).

[Claim: Ex-Employee Sues for Wrongful Firing] ──> 100% DENIED via Employment Practices Exclusion.

The "Occurrence" Trap: For a CGL policy to trigger, the financial damage must stem from an "occurrence," which insurance law strictly defines as an accident. A termination, demotion, or disciplinary action is a deliberate, calculated corporate management decision executed by your leadership team. Because the termination was intentional, it fails the baseline contractual definition of an accident, allowing the carrier to instantly reject the defense.

2. The Modern Litigious Landscape: Why the Bill is a Business-Killer

Relying on a basic business policy while managing a workforce exposes your corporate cash reserves to highly elevated modern employment litigation costs. If a disgruntled worker files a lawsuit following a performance review backlash, your business faces immense out-of-pocket overhead:

- The Uninsured Defense Burn Rate: Employment defense attorneys do not operate on contingency. Win or lose, mapping out an answer to a civil complaint, executing digital discovery, and taking depositions averages $15,000 to $35,000 just to reach a summary judgment motion. If the case proceeds to a formal jury trial, defense bills routinely skyrocket past $100,000.

- The Statutory Fee-Shifting Penalty: Employment laws are uniquely sharp. Under federal and state statutes, if a court finds your business even partially liable for wrongful termination or retaliation, the judge can legally force your company to pay 100% of the plaintiff’s legal fees on top of your own defense bills and the core settlement judgment.

3. How to Erect a Secure Employment Shield

If your enterprise is operating on an off-the-shelf commercial general liability policy without custom employment endorsements, your company’s balance sheet is entirely exposed to your payroll roster.

To safely insulate your corporate assets, you must transition your protection framework to a dual-layer risk management shield:

Step 1: Audit Your Business Owner's Policy (BOP) for Active Employment Gaps

Step 2: Bind an Employment Practices Liability Insurance (EPLI) Policy or Rider

= Total Institutional Safety for Harassment, Retaliation, and Wrongful Discharge

- The Contractual Defense: You must formally purchase Employment Practices Liability Insurance (EPLI). This specialty professional line can be appended as an endorsement to an existing Business Owner’s Policy (BOP) for smaller firms or structured as a standalone corporate line for larger operations. EPLI explicitly steps in to fund your legal defense panel, pay for mandatory mediation, and settle judgments arising directly from wrongful termination, sexual harassment, discrimination, and negligent employee evaluations.

- The Operational Defense: EPLI underwriters require active loss-control mitigation. Your business must maintain an updated, legally vetted employee handbook. Performance reviews must feature clear, objective metrics, and every verbal warning, disciplinary write-up, and performance improvement plan (PIP) must be digitally documented and signed by management to create an unassailable paper trail.

Why Working with an Independent Agency is Vital

Attempting to manage complex corporate liability risks through a faceless online insurance portal ensures you will miss the critical, industry-specific endorsements needed to survive a workforce dispute. At Walker Insurance Agency, we provide the data-driven visibility you need to defend your business lines.

The Walker Advantage:

- Employment Risk Alignment: We analyze your employee count, turnover metrics, and historical payroll structures to scale an EPLI policy with deductibles that match your liquid corporate cash flow.

- Exclusion Dissection: We audit your commercial umbrellas and excess liability layers to guarantee that your employment practices defense extends seamlessly into higher liability limits.

- Market Stabilization Sweeps: We continuously shop your business profile across premier commercial underwriters to capture the highest employment defense limits at the absolute lowest available premium floors in Stuart.

FAQ

1. Does a General Liability policy cover a lawsuit if a former employee accuses management of slander or libel during a performance review?

No. While standard CGL policies do feature a section called Personal and Advertising Injury—which covers third-party defamation, libel, and slander claims—this section contains a strict, universal Employment-Related Practices Exclusion. If the alleged defamation happens within the context of hiring, evaluating, disciplining, or firing a member of your workforce, it is completely excluded from general liability and can only be covered via an EPLI policy.

2. What is the difference between Workers' Compensation and EPLI?

Workers' Compensation covers physical, on-the-job bodily injuries and medical recovery costs regardless of fault (e.g., an employee falling off a ladder). EPLI covers non-physical, administrative lawsuits brought against management alleging violations of civil rights, labor laws, or employment contracts (e.g., an employee claiming they were fired as retaliation for reporting a safety violation).

3. If an employee's wrongful termination claim is entirely frivolous and fake, will my General Liability policy at least pay to throw it out of court?

No. A general liability carrier has zero duty to defend a claim that falls squarely within an explicit policy exclusion. Even if the ex-employee's allegations are completely fabricated, malicious, or factually impossible, your standard CGL company will completely decline to provide a corporate attorney, leaving your business to fund the initial defense counsel out of pocket just to file a motion to dismiss.

Insulate Your Corporate Balance Sheet Before the Next Exit Interview

Terminating an underperforming worker is a necessary operational step to protect your business growth, but leaving your management decisions exposed to a baseline general liability policy is an administrative gamble that can instantly drain your corporate reserves. True business security requires aligning your insurance portfolio with the modern realities of employment law.

Lock in your corporate defense shield today. Contact Walker Insurance Agency for a comprehensive business risk audit. We provide the visibility you need to erase hidden employment loopholes, deploy high-limit EPLI policies, and protect your company's hard-earned wealth safely in Stuart.

[GET A FREE COMMERCIAL QUOTE TODAY]

Call our commercial division at +1-407-977-7100 or visit our office in Stuart, FL. Let us safeguard your business boundaries today.

Related Articles

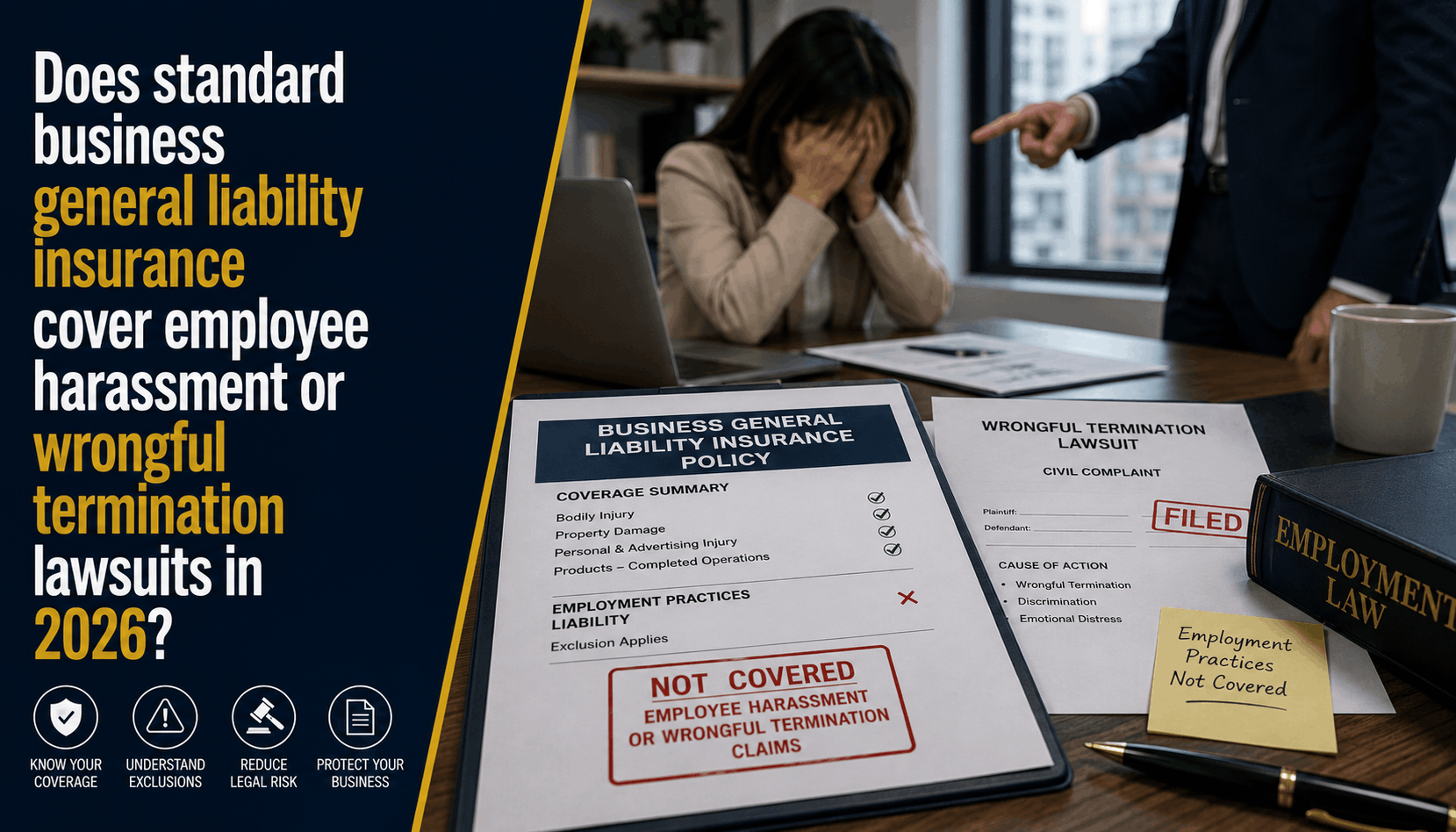

Does General Liability Cover Employee Harassment or Wrongful Termination? (2026 Rules)

Relying on standard Commercial General Liability to protect your business from employee lawsuits? Discover why CGL excludes wrongful termination and harassment in 2026.

Read More →

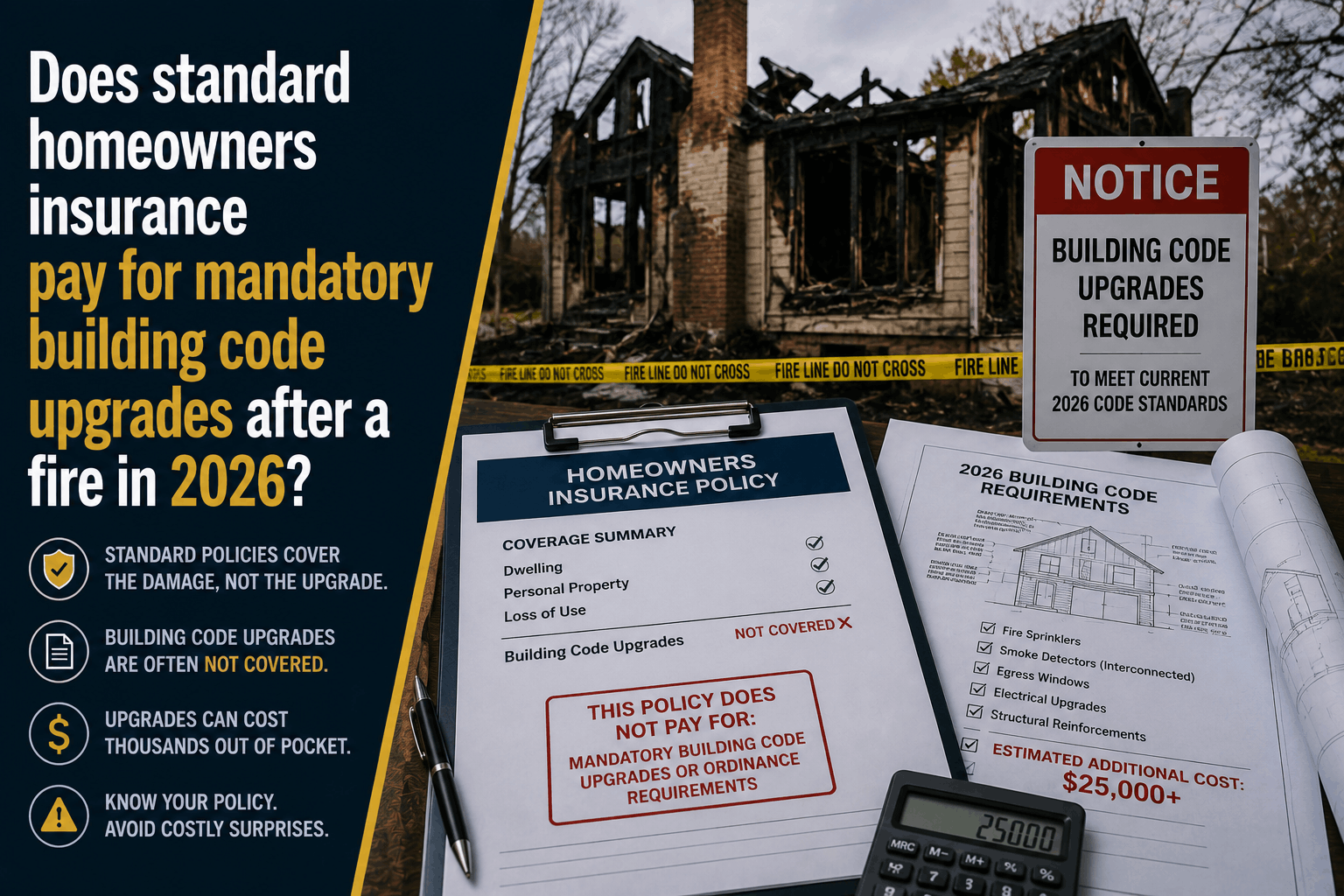

Does Homeowners Insurance Pay for Code Upgrades After a Fire?

A standard home insurance policy won't cover mandatory building code upgrades after a fire. Learn about the Ordinance or Law trap and how to protect your home.

Read More →

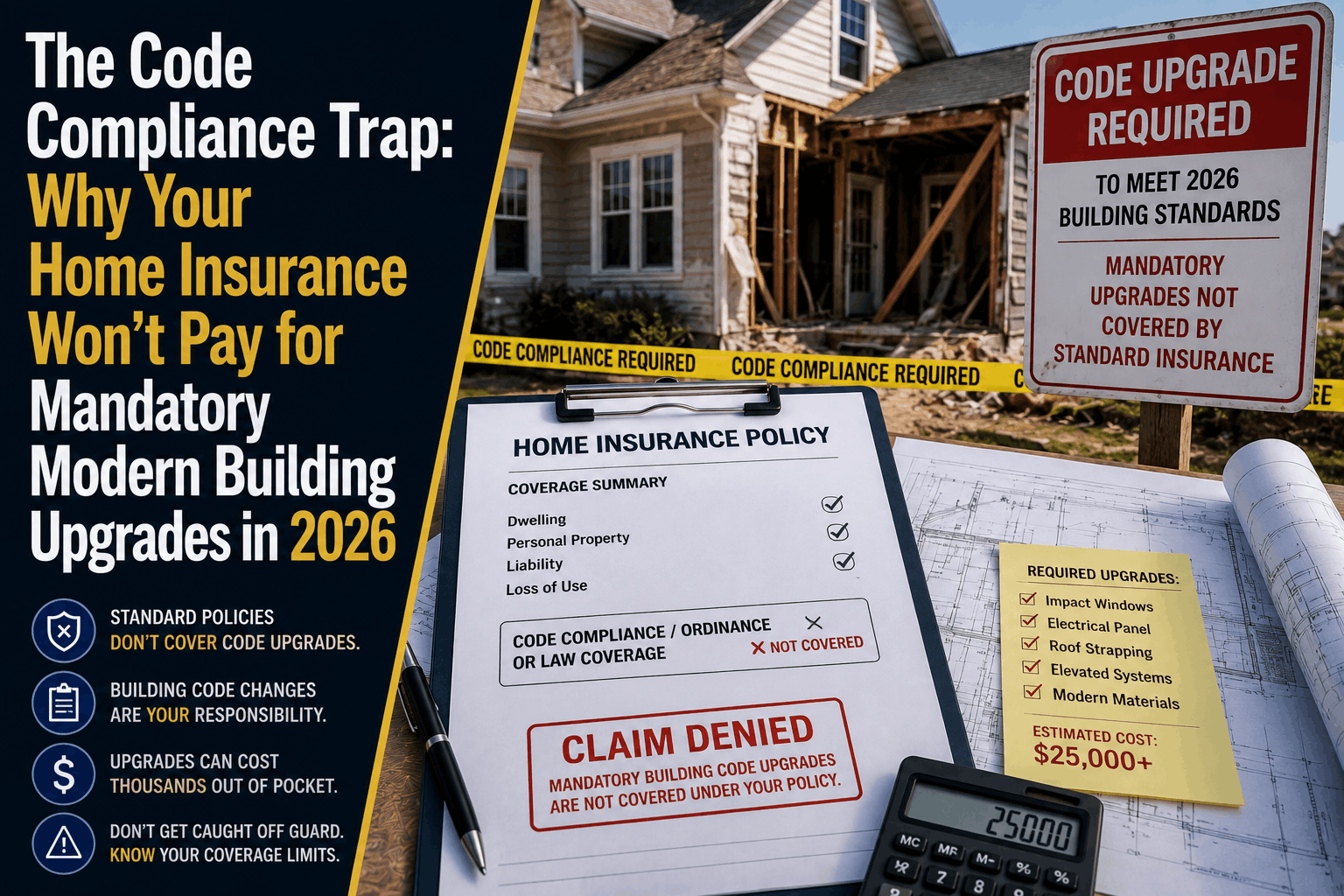

The Code Compliance Trap: Why Home Insurance Won't Pay for Upgrades

Discovered a massive gap in your property insurance after a disaster? Learn why standard home insurance completely denies mandatory building code upgrades in 2026.

Read More →