Does Homeowners Insurance Cover a Sewer Backup or Drain Overflow? (2026 Rules)

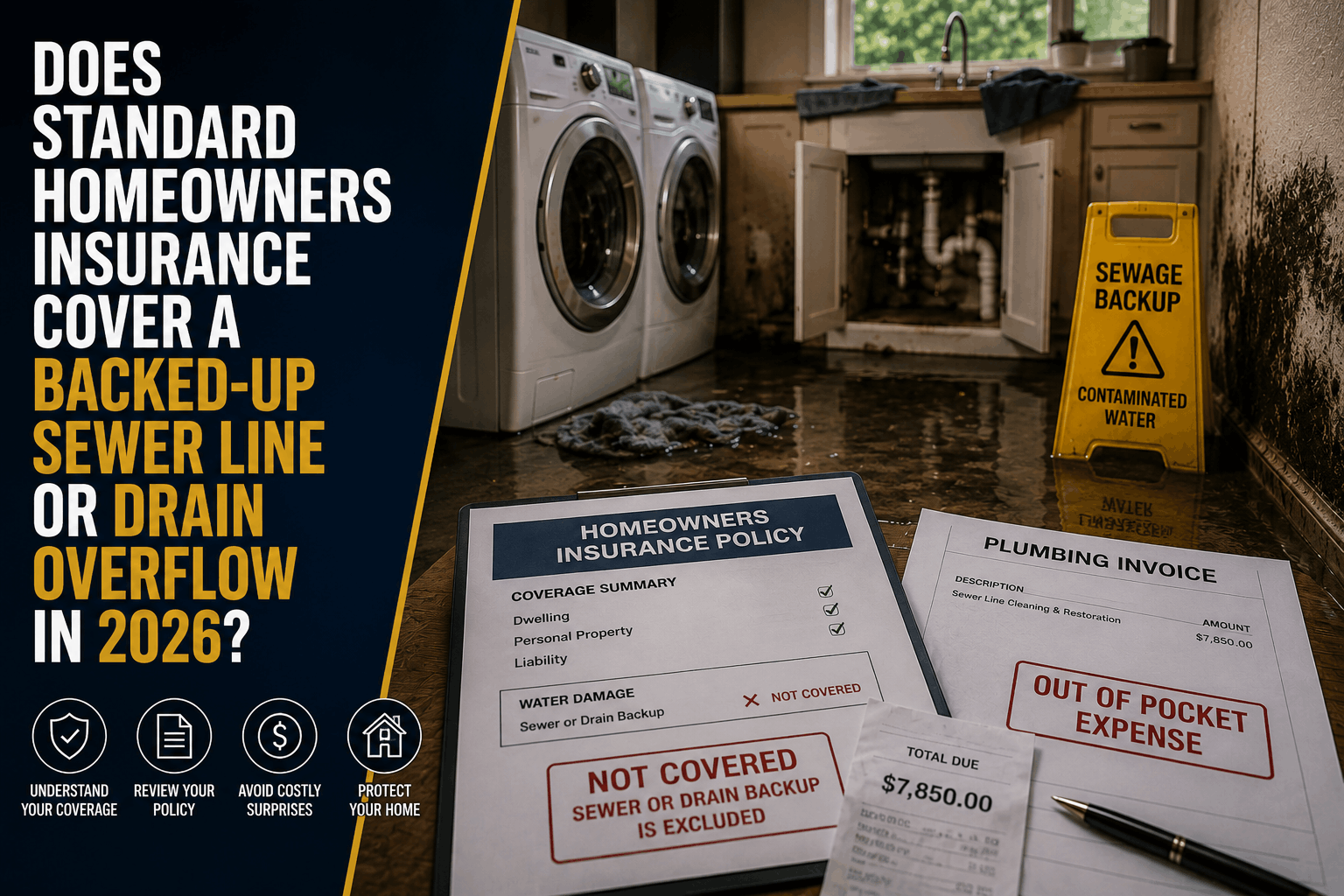

Does Standard Homeowners Insurance Cover a Backed-Up Sewer Line or Drain Overflow in 2026?

The Direct Answer: No, a standard homeowners insurance policy will pay exactly $0 to clean up or repair the damage caused by a backed-up sewer line, overflowing toilet, or failed sump pump. There is a massive, high-risk misconception that "water damage is water damage." It isn't. Standard insurance policy forms treat clean water from a sudden, burst internal pipe completely differently than reverse-flow wastewater originating from beneath your floors.

In 2026, as severe summer thunderstorms and flash floods put historic stress on aging municipal sewer mains, this hidden exclusion is triggering devastating claims denials across the country.

Unless you have explicitly paid for an optional, add-on policy endorsement titled Water Backup and Sump Pump Failure Coverage, 100% of the cost to extract toxic black water, gut contaminated drywall, and replace ruined flooring must come entirely out of your own personal savings.

1. The Contractual Technicality: The Flow Direction Rule

To understand why your insurer will issue a total denial after a subterranean disaster, you must understand how insurance adjusters legally define water movement. The industry-standard HO-3 and HO-5 policy jackets contain a universal, absolute Water Damage Exclusion that relies strictly on the direction of the flow:

- Outward or Falling Flow (Covered): If water escapes from a burst pipe or a ruptured water heater, the damage is 100% covered by a standard policy because the event originates from your internal plumbing systems.

- Inward or Rising Flow (Excluded): If water or sewage flows backward into your home through a drain, toilet, or sump pump pit, the damage is 100% denied by default because it originates from subterranean municipal lines or external groundwater.

The ISO Standard Form Reality: The Insurance Services Office (ISO), which blueprints the standard insurance contracts used by nearly every major carrier, explicitly carves out and excludes water or sewage that backs up through sewers, drains, sump pumps, or sump-pump-related equipment. This exclusion applies automatically, regardless of whether the backup was caused by a massive municipal sewer main surcharge down the street or a severe clog inside your private lateral line.

2. The Summer Threat: Why Heat and Storms Trigger the Trap

Summer represents peak vulnerability for subterranean water backups due to two seasonal catalysts hitting your plumbing system simultaneously:

- Flash Flood Surcharges: Torrential summer downpours dump inches of water in a matter of minutes. When municipal storm sewers are overwhelmed, the excess volume has nowhere to go but backward. It forces its way up through the lowest available opening—which is typically the floor drain, toilet, or shower stall in a residential basement or ground-floor bathroom.

- The Power Outage Sump Pump Failure: Severe summer storms routinely knock out regional power grids. If your home relies on a sump pump to evacuate rising groundwater from around your foundation, a grid failure cuts the electrical supply. The pump dies, the pit overflows, and your lower level is flooded within hours. Because a power outage isn't an accident on your property, a standard policy will not cover the resulting destruction.

3. The 2026 Cost Reality: Why Black Water Claims Hurt Most

Attempting to handle a sewer backup out of pocket is an expensive, hazardous nightmare. Wastewater backups are classified as Category 3 (Black Water) losses, meaning the liquid contains raw sewage, pathogenic bacteria, and chemical contaminants.

Because of the extreme biohazard risks, cleanup costs in 2026 have skyrocketed across three critical phases:

- Professional Mitigation ($3,000 – $7,000): Requires industrial water extraction, chemical biocide sanitization, and specialized commercial structural drying equipment to eliminate toxic microbes.

- Hazardous Tear-out ($2,500 – $5,000): All porous materials—including carpeting, padding, baseboards, and the bottom feet of drywall—cannot be saved or washed. They must be entirely gutted and disposed of as biohazardous waste.

- Structural Reconstruction ($5,000 – $20,000+): Hanging new drywall, painting, and rebuilding a finished space using modern contractor labor rates and replacement materials.

How to Build a Subterranean Safety Shield

If your home is currently sitting on an unmodified baseline property contract, your household budget is completely exposed to the sewer grid. At Walker Insurance Agency, we advise clients to execute a precise, two-part risk-mitigation strategy:

Step 1: Install a Mechanical Backwater Valve & Battery Sump Backup (Physical Defense)

Step 2: Formally Bind a Water Backup and Sump Pump Endorsement (Contractual Defense)

= 100% Comprehensive Safety From Toxic Black Water Floods and Pump Grid Failures

- The Contractual Shield: Contact your independent agent and ask to formally add a Water Backup Endorsement to your policy. This rider completely deletes the standard exclusion. For an incredibly affordable cost of $50 to $250 per year, it unlocks $10,000 to $25,000 of dedicated clean funding to pay for hazardous extraction, structural drying, mold remediation, and personal property replacement following a backup, subject to a standard $1,000 deductible.

- The Physical Shield: Have a licensed plumber install a backwater valve on your main sewer lateral line. This mechanical valve allows wastewater to exit your home but automatically clamps shut if sewage attempts to flow backward into your drains. Additionally, equip your sump pump with a dedicated marine-grade battery backup system to ensure continuous operation even if a summer storm drops the local electrical grid.

Why Working with an Independent Agency is Vital

Managing your primary residential assets through a generic smartphone application or automated online form ensures you will miss the fine-print exclusions that cause catastrophic claims denials. At Walker Insurance Agency, we provide the personalized, data-driven visibility you need to defend your property line.

The Walker Advantage:

- Custom Risk Scaling: We evaluate your home's foundation—whether you have a finished basement, storage space, or are built on a concrete slab—to scale your endorsement limits to match actual 2026 reconstruction costs.

- The Flood vs. Backup Distinction: We meticulously audit your portfolio to ensure you don't confuse water backup endorsements with a separate National Flood Insurance Program (NFIP) policy. Flood lines cover rising surface waters coming from outside your home; backup riders cover reverse-flow coming from inside your drains. You need both to be fully safe.

- Strategic Carrier Matching: We cross-reference your property against the underwriting guidelines of top-tier private carriers to capture the highest backup limits at the absolute lowest available premium floors in Stuart.

FAQ

1. If the municipal sewer main on the street clogs and backs up into my house, shouldn't the city pay for the damage? In the vast majority of cases, no. Municipalities enjoy strong sovereign immunity protections. To force a city or county government to pay for a residential sewer backup, you must legally prove that the city was aware of an ongoing structural defect or blockage in their line and completely neglected to fix it over an extended period. If a sudden rainstorm overwhelms the grid, the city is legally cleared of liability, leaving you completely on your own if you don't carry the proper insurance endorsement.

2. Does a water backup rider pay to replace my broken sump pump motor? No. A standard water backup endorsement is designed to cover the ensuing damage caused by the escaping water (drywall, floors, cleanup costs). It does not cover the cost to physically repair or replace the mechanical pump unit itself. To protect the actual machinery against electrical or mechanical failure, you must pair your backup rider with an Equipment Breakdown Endorsement.

3. What should I do immediately if raw sewage begins backing up through my basement floor drain? Evacuate children and pets from the lower level immediately due to biohazard risks. Stop using all running water, sinks, showers, and washing machines inside the house to prevent feeding more volume into the system. Call a licensed plumber to clear your lateral line or identify the block, and contact your independent insurance agent right away to document the occurrence. Take high-resolution photographs of the water source and surrounding damage before any remediation crew begins tearing out materials.

Insulate Your Balance Sheet Before the Storm Clouds Gather

A sewer or drain backup is one of the most destructive, expensive, and stressful events a homeowner can experience. Leaving the financial survival of your property to a basic, off-the-shelf insurance contract is an administrative gamble that can instantly wipe out your emergency funds in a single afternoon.

Lock in your protection before the next summer storm rolls in. Contact Walker Insurance Agency today for a comprehensive property risk assessment. We provide the visibility you need to eliminate hidden drainage loops, deploy high-limit backup endorsements, and protect your family's hard-earned wealth safely in Stuart.

[GET A FREE QUOTE TODAY]

Call us at +1-407-977-7100 or visit our office in Stuart, FL. Let us safeguard your home boundaries today.

Related Articles

Does Personal Car Insurance Cover Delivery Accidents? (2026)

Driving for DoorDash, Instacart, or Amazon Flex in Stuart? Discover why your personal auto policy won't pay a single dollar for a delivery crash this year.

Read More →

The Delivery Car Side Hustle Trap: Personal Auto Exclusions in 2026

Thinking of driving for DoorDash, Uber Eats, or Instacart in Stuart this summer? Learn why your personal car insurance will completely deny a delivery accident claim.

Read More →

The Florida Sinkhole Loophole: Why Home Insurance Fails in July 2026

Think your Florida "full coverage" home insurance handles foundation cracks? Discover the Catastrophic Ground Cover Collapse loophole hitting Stuart homeowners.

Read More →