The Delivery Car Side Hustle Trap: Personal Auto Exclusions in 2026

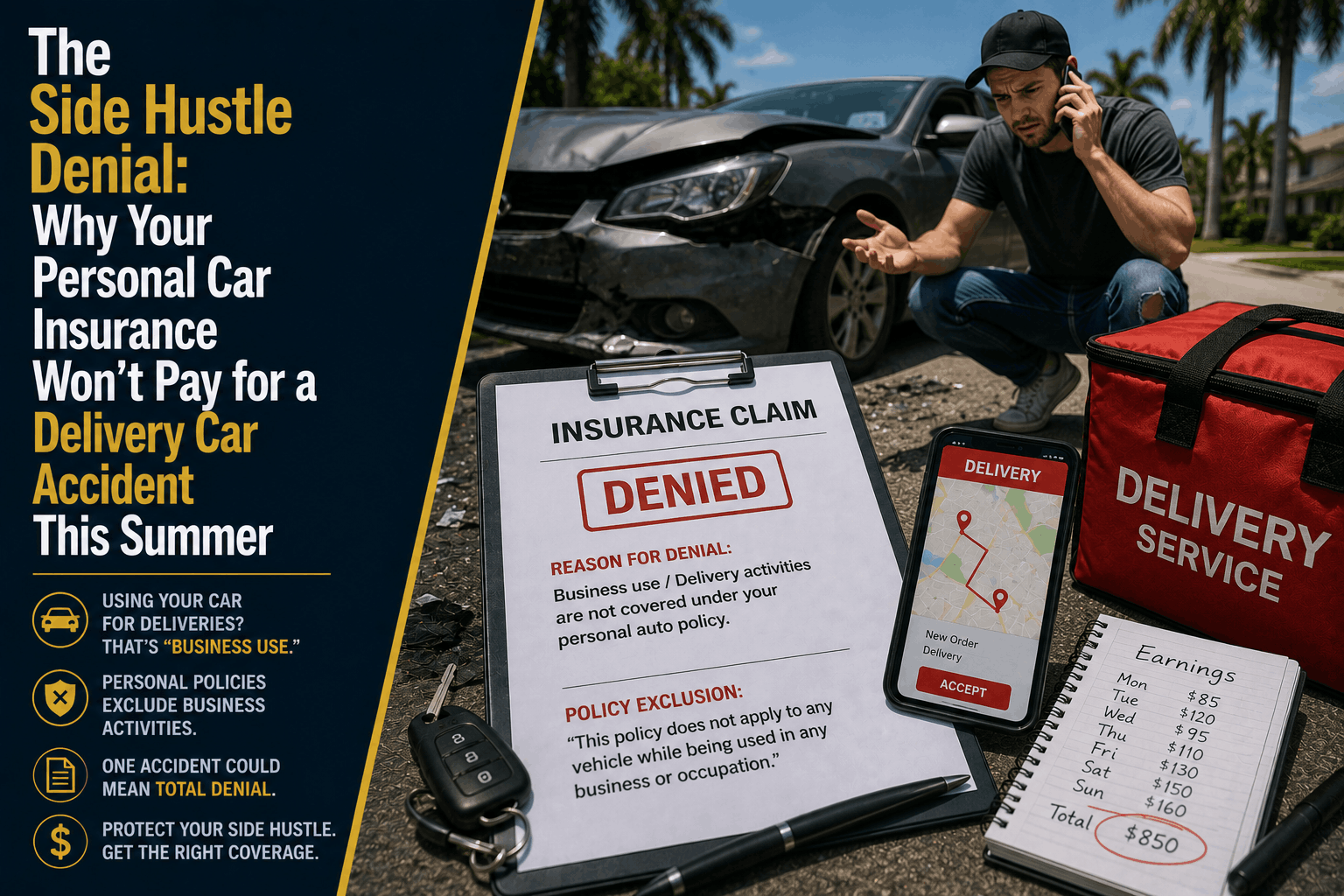

The Side Hustle Denial: Why Your Personal Car Insurance Won't Pay for a Delivery Car Accident This Summer

The Direct Answer

The short answer is no, your personal policy will not pay a single dime. In 2026, the moment you log into a delivery app like DoorDash, Uber Eats, Instacart, or Amazon Flex to start a summer side hustle in Florida, your personal auto insurance policy completely stops protecting you. Every standard personal auto contract features a strict Business Use or Commercial Use Exclusion. This clause explicitly states that the insurance carrier is legally allowed to deny any claims for vehicle damage, medical liabilities, or third-party injuries if the vehicle is being used to transport goods or passengers for financial gain. If you get into a fender bender or cause an intersection collision while chasing a surge delivery fee, your personal insurer will deny the claim entirely, drop your policy, and leave you to pay thousands of dollars completely out of pocket.

For thousands of drivers across Stuart and the Treasure Coast looking for flexible hours and quick cash, this contractual firewall is catching people completely off guard. To minimize their risk exposure in a high-inflation auto market, private car insurance companies are using advanced digital claims tracking to enforce these exclusions aggressively, shifting the massive overhead of commercial accidents directly onto the gig worker's shoulders.

1. The Complex App Reality: Navigating the Three Phases of Coverage

Many delivery drivers operate under the dangerous assumption that the gig platform's corporate insurance policy automatically protects them. While major apps do provide commercial coverage, this protection is highly restricted and changes completely based on what you are doing at the exact split-second of a crash.

The delivery window is legally divided into three separate phases, each carrying severe gaps:

- Phase 1: The App is Open, Waiting for a Ride or Order. You are driving around local Stuart streets waiting to accept a delivery job. During this time, your personal insurance will issue an immediate denial because your vehicle is active for business use. Meanwhile, the gig platform's corporate policy only offers bare-minimum, secondary third-party liability coverage. If you cause an accident during Phase 1, the app will pay exactly $0 to repair your own vehicle, exposing your personal savings to the full cost of the damage.

- Phase 2: The Order is Accepted, En Route to Pick Up. You have accepted a delivery request and are driving to a local restaurant or store. While the gig company's higher liability limits activate here, their physical damage coverage (comprehensive and collision) is highly conditional. Many platforms will completely refuse to fix your car during Phase 2 unless you already carry a specific commercial endorsement on your personal baseline policy.

- Phase 3: The Goods are in the Car, En Route to Drop Off. This represents the highest tier of corporate app coverage, providing up to $1 million in third-party liability. However, a major trap remains regarding your own vehicle. If you carry a high deductible on your personal policy, the gig app's commercial policy will force you to pay a massive, flat corporate deductible—routinely $1,000 to $2,500—before they will release a dollar to fix your car.

2. The Real Cost Breakdowns of a Side Hustle Accident Denial

Attempting to hide your delivery activity from your insurance company after an accident is a severe risk that carries immediate financial ruin. If a claims adjuster discovers you were active on a delivery network, the out-of-pocket trajectory scales rapidly across multiple fronts:

- Minor Fender Benders and Bumper Repairs: If you suffer a minor rear-end collision while looking down at your phone for navigation instructions, replacing a modern bumper with built-in parking sensors and radar components routinely costs $3,500 to $5,500 at local Martin County body shops. Because your personal policy denies the business use, you must pay this entire bill out of pocket just to get your vehicle back on the road.

- Severe Multi-Vehicle Collisions: If you push through an intersection to meet a strict app delivery deadline and cause a moderate two-car accident, vehicle replacement costs and property damage easily climb to $25,000 to $45,000. Without active insurance coverage, the other party's insurance provider will pursue your personal assets, garnish your future wages, and place liens on your property to recover their losses.

- The Post-Denial Insurance Penalty: Failing to disclose commercial side hustles constitutes a major breach of contract. Once your insurer discovers the delivery activity, they will not only deny the claim, but they will also issue an immediate, non-voluntary Policy Cancellation. Being dropped for non-disclosure places you permanently into the high-risk driver pool, causing your future auto insurance premiums to skyrocket by 60% to 120% across any company in Florida.

3. How to Secure Your Income and Vehicle This Summer

You do not have to give up your delivery side hustle, but you must align your insurance contract with the physical reality of how you use your vehicle. At Walker Insurance Agency, we advise Stuart drivers to protect their mobile assets using a clear, three-step defensive layout:

- Step 1: Dissect Your Policy’s "Exclusions" Subsection. Pull your complete auto insurance policy packet and search specifically for the terms "Public or Livery Conveyance Exclusion" or "Business Pursuits Limitation." Understand exactly where your personal coverage ends.

- Step 2: Bind a Dedicated Rideshare or Delivery Endorsement. Request an independent broker to attach a specialized gig-work rider directly to your personal policy. This affordable add-on explicitly permits app delivery use, fills the gaps during Phase 1 and Phase 2, and protects you from policy cancellation for a minimal monthly premium adjustment.

- Step 3: Preserve Immediate Digital Evidence. If you are involved in a collision while driving, take instant screenshots of your delivery app status before closing the application or turning off your phone. Documenting whether you were waiting for an order, picking up, or dropping off is vital evidence required to force the corporate gig app to honor their property liabilities.

Why Working with an Independent Agency is Vital

Attempting to manage complex commercial auto risks through a generic smartphone application or an automated online form ensures you will miss the fine-print exclusions that lead to total claims denials. At Walker Insurance Agency, we provide the personalized, data-driven visibility you need to protect your vehicle and your income.

The Walker Advantage:

- Exclusion Form Dissection: We thoroughly analyze your underlying auto policies to expose hidden commercial restrictions before you accept your next delivery order.

- Gig Market Premium Matching: We continuously shop your profile across Florida's expanding independent market to locate specialized carriers that include affordable rideshare and delivery riders without forcing you into expensive, full-scale commercial lines.

- Local Rate Scaling: We align your policy limits with the actual reality of local Stuart medical inflation and vehicle repair overhead so your hard-earned wealth is completely protected.

FAQ

1. If I only deliver food or groceries and never carry passengers, does the business exclusion still apply?

Yes, absolutely. The standard Florida auto insurance exclusion applies to the commercial transport of any property, goods, or passengers for compensation. It does not matter if you are carrying a human passenger in an Uber or a bag of groceries for Instacart; from an underwriting standpoint, you are operating a commercial delivery vehicle.

2. Can the insurance company actually find out I was delivering if I don't tell them?

Yes, easily. In 2026, insurance claims adjusters routinely check accident locations, review local traffic camera footage, request cell phone records, and directly cross-reference state accident reports with known gig-economy databases. Furthermore, if a restaurant worker or the person receiving the delivery mentions the app to responding police officers, it will be noted on the official crash report, triggering an automatic denial.

3. Does the gig app's insurance cover my medical bills if I am hurt while delivering?

Rarely. Most delivery platforms provide third-party liability coverage (to pay for the other person's car and injuries), but they offer minimal to zero personal protection for your own bodily injuries or lost wages. To ensure your medical bills are handled after a severe commercial accident, you must carry a personal policy that explicitly allows for delivery use or carries a matching medical payment rider.

Insulate Your Side Hustle Income Before Your Next Delivery

Your car is the engine of your independent summer income, but leaving its protection to a basic, un-vetted personal auto policy is an administrative gamble that can instantly wipe out your bank account. True peace of mind requires pulling back the curtain on your policy’s exclusions and ensuring your written contract matches the professional reality of your driving habits.

Take control of your auto protection today. Contact Walker Insurance Agency for a comprehensive portfolio evaluation. We provide the visibility you need to eliminate hidden side hustle loopholes, deploy high-limit comprehensive delivery riders, and protect your family's hard-earned wealth safely in Stuart.

[GET A FREE QUOTE TODAY]

Call our personal lines division at +1-407-977-7100 or visit our office in Stuart, FL. Let us safeguard your property boundaries today.

Related Articles

Does Personal Car Insurance Cover Delivery Accidents? (2026)

Driving for DoorDash, Instacart, or Amazon Flex in Stuart? Discover why your personal auto policy won't pay a single dollar for a delivery crash this year.

Read More →

The Florida Sinkhole Loophole: Why Home Insurance Fails in July 2026

Think your Florida "full coverage" home insurance handles foundation cracks? Discover the Catastrophic Ground Cover Collapse loophole hitting Stuart homeowners.

Read More →

Does a Florida Screen Endorsement Cover Mesh Damage? (2026 Rules)

Think your pool enclosure insurance covers everything? Discover "The Frame-Only Trick" that leaves Florida homeowners paying 100% out of pocket for torn mesh in 2026.

Read More →