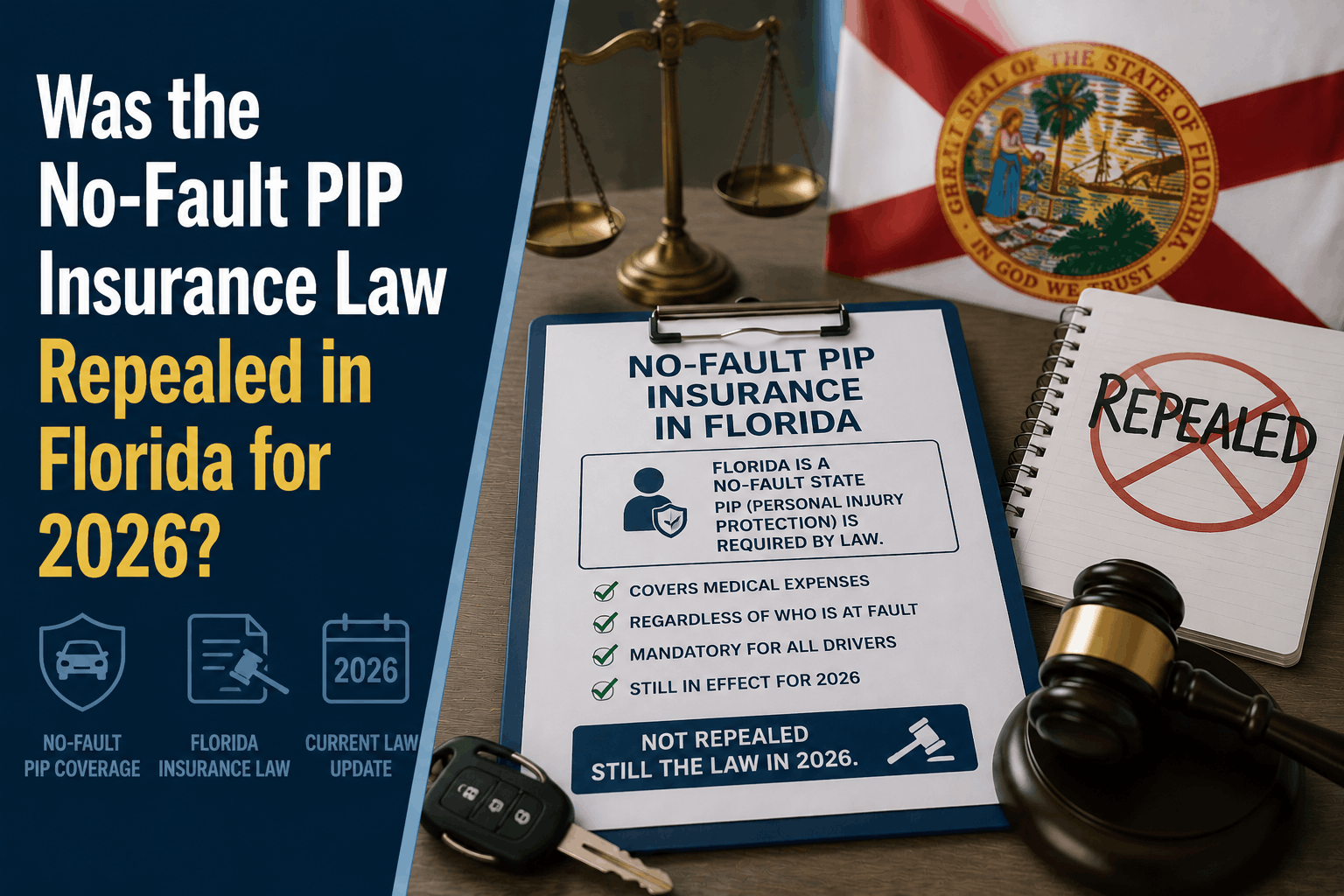

Was PIP Repealed in Florida for 2026? Fact-Checking the Rumors

Was the No-Fault PIP Insurance Law Repealed in Florida for 2026?

The Direct Answer: No, Florida’s 55-year-old no-fault auto insurance law has NOT been repealed. Despite a flood of viral headlines, law firm blog posts, and incorrect AI-generated search summaries claiming that Personal Injury Protection (PIP) is ending, the law remains fully active.

SandStone Insurance Partners

During the legislative session, lawmakers introduced Senate Bill 522 and House Bill 769, which aimed to completely eliminate PIP and transition Florida to a traditional at-fault liability system. However, both of these bills officially died in committee.

SandStone Insurance Partners

If you own or operate a registered motor vehicle in Florida, you are still legally mandated under Florida Statute § 627.736 to carry a minimum of $10,000 in PIP coverage and $10,000 in Property Damage Liability (PDL).

SandStone Insurance Partners

To achieve total visibility over your auto policy, you must look past the internet rumors. Canceling your PIP coverage or failing to follow its strict post-accident rules based on online myths will result in an immediate driver's license suspension and a total denial of medical benefits if you crash.

1. Debunking the 2026 "July 1st Repeal" Myth

If you have searched for Florida insurance updates recently, you may have read that the no-fault system is expiring on July 1, 2026. Here is exactly why that rumor is spreading—and why it is wrong:

Alpha Law Group

- The Origin of the Misinformation: Several plaintiff law firms and automated content sites published "predictive" articles in late 2025, assuming that the 2026 legislative push to kill PIP would easily pass.

- The Legislative Reality: When the Florida Legislature adjourned, both repeal bills were officially dead. The House Civil Justice Subcommittee and the Senate Banking and Insurance Committee chose not to advance the measures to a floor vote.

SandStone Insurance Partners - The Historical Context: The closest Florida ever came to a repeal was in 2021 (SB 54), which successfully passed both chambers but was ultimately vetoed by Governor Ron DeSantis, who cited concerns that forcing a mandatory bodily injury liability framework would spike premium costs for low-income drivers. No repeal bill has reached his desk since.

SandStone Insurance Partners

2. The Active 2026 PIP Rules You Must Follow

Because the no-fault framework remains the law of the land, you are still subject to the rigid "gatekeeping" rules designed by insurers to manage claims:

- The 14-Day Treatment Window: You must seek initial medical care within exactly 14 calendar days of an auto accident. If you wait until day 15, your carrier will legally deny your medical benefits entirely.

SandStone Insurance Partners - The Emergency Medical Condition (EMC) Rule: Your initial $10,000 limit is automatically capped at $2,500 unless a primary qualifying physician documents that you suffered an Emergency Medical Condition (EMC).

SandStone Insurance Partners - The 80/60 Payout Split: PIP does not pay your full bill; it only reimburses 80% of reasonable medical expenses and 60% of documented lost wages.

SandStone Insurance Partners

[LEGISLATION CHECK]

✕ SB 522 (PIP Repeal) ──> DIED IN COMMITTEE

✕ HB 769 (Companion) ──> DIED IN COMMITTEE

[CURRENT MANDATE]

✓ Minimum $10,000 PIP ──> STILL REQUIRED BY LAW

✓ 14-Day Medical Rule ──> STILL ENFORCED

3. The Real 2026 Shift: Falling Rates, Not Repeals

While PIP wasn't repealed, the Florida auto insurance market is experiencing a massive transformation. Following highly successful tort (lawsuit abuse) reforms, carrier litigation expenses have plummeted across the state.

Instead of a law change, Florida drivers are seeing a "Deflation Dividend":

- Progressive implemented a statewide average 8% premium drop.

- State Farm rolled back rates by an average of 10.1%.

- USAA and Allstate both introduced fresh 7% price reductions.

The market is stabilizing rapidly, meaning you can easily lower your premium right now by shopping your policy—without having to wait for a structural change to the no-fault system.

Why Working with an Independent Agency is Vital

When false insurance news circulates online, managing your coverage through an automated smartphone app or an unmonitored portal exposes you to severe legal gaps. At Walker Insurance Agency, we provide the data-driven visibility you need to navigate verified Florida statutes.

The Walker Advantage:

- Statutory Compliance Verification: We audit your active policy declarations page to ensure your PIP and Property Damage limits comply perfectly with current highway mandates.

- Deductible Exposure Management: We identify hidden $1,000 PIP deductibles that online portals use to artificially lower quotes, replacing them with safe, $0-deductible options that won't break your budget after an accident.

- MedPay Stacking: We help you layer Medical Payments (MedPay) on top of your mandatory PIP to completely erase the 20% co-insurance gap, creating a seamless 100% out-of-pocket medical shield.

FAQ

1. What happens if I cancel my PIP coverage thinking the law changed? If you cancel your PIP, the insurance company will automatically notify the Florida Department of Highway Safety and Motor Vehicles (FLHSMV). The state will immediately suspend your driver’s license, registration, and license plate, and you will face a reinstatement fee of up to $500.

2. Will Florida try to repeal the no-fault law again next year? It is highly likely. Trial lawyers and certain consumer groups introduce a PIP repeal bill nearly every legislative session. However, until a bill passes both the House and Senate and is officially signed into law by the governor, the current $10,000 PIP mandate remains active.

Greene & Associates Insurance

3. Does Florida's 51% Modified Comparative Negligence law affect my PIP? No. Florida's updated 51% fault rule (which bars you from recovering money if you are mostly to blame for a crash) only applies to third-party liability lawsuits. Because PIP is a "No-Fault" benefit, your own insurer will still pay your medical bills up to your policy limit even if you were 100% at fault for the accident.

Greene & Associates Insurance

Base Your Policy on Facts, Not Internet Rumors

Don't let misleading online headlines compromise your legal standing or your financial security on the road. The Florida no-fault system is alive and well, and protecting your family requires setting up your policy coverages correctly under current 2026 rules.

Alpha Law Group

Get a verified policy audit today. Contact Walker Insurance Agency for a comprehensive rate and statute review. We provide the visibility you need to maximize the current market rate drops while maintaining an ironclad shield around your assets in Stuart.

[GET A FREE QUOTE TODAY] Call us at +1-407-977-7100 or visit our office in Stuart, FL. Let us shop the real market for you today.

Related Articles

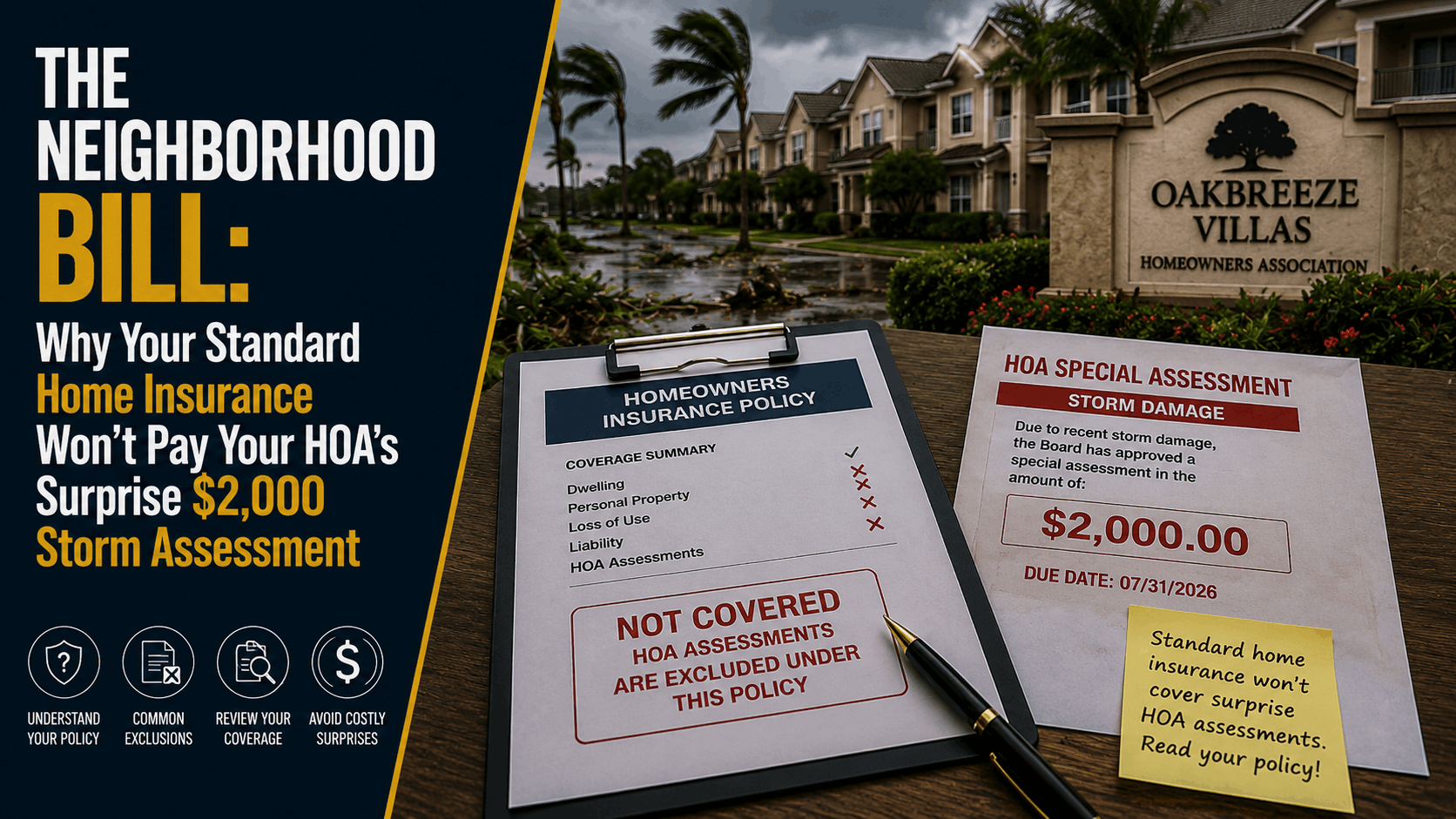

Why Home Insurance Won't Pay Your HOA Storm Assessment (2026)

Received a surprise HOA special assessment after a storm? Discover the critical loss assessment loopholes leaving Stuart homeowners completely exposed in 2026.

Read More →

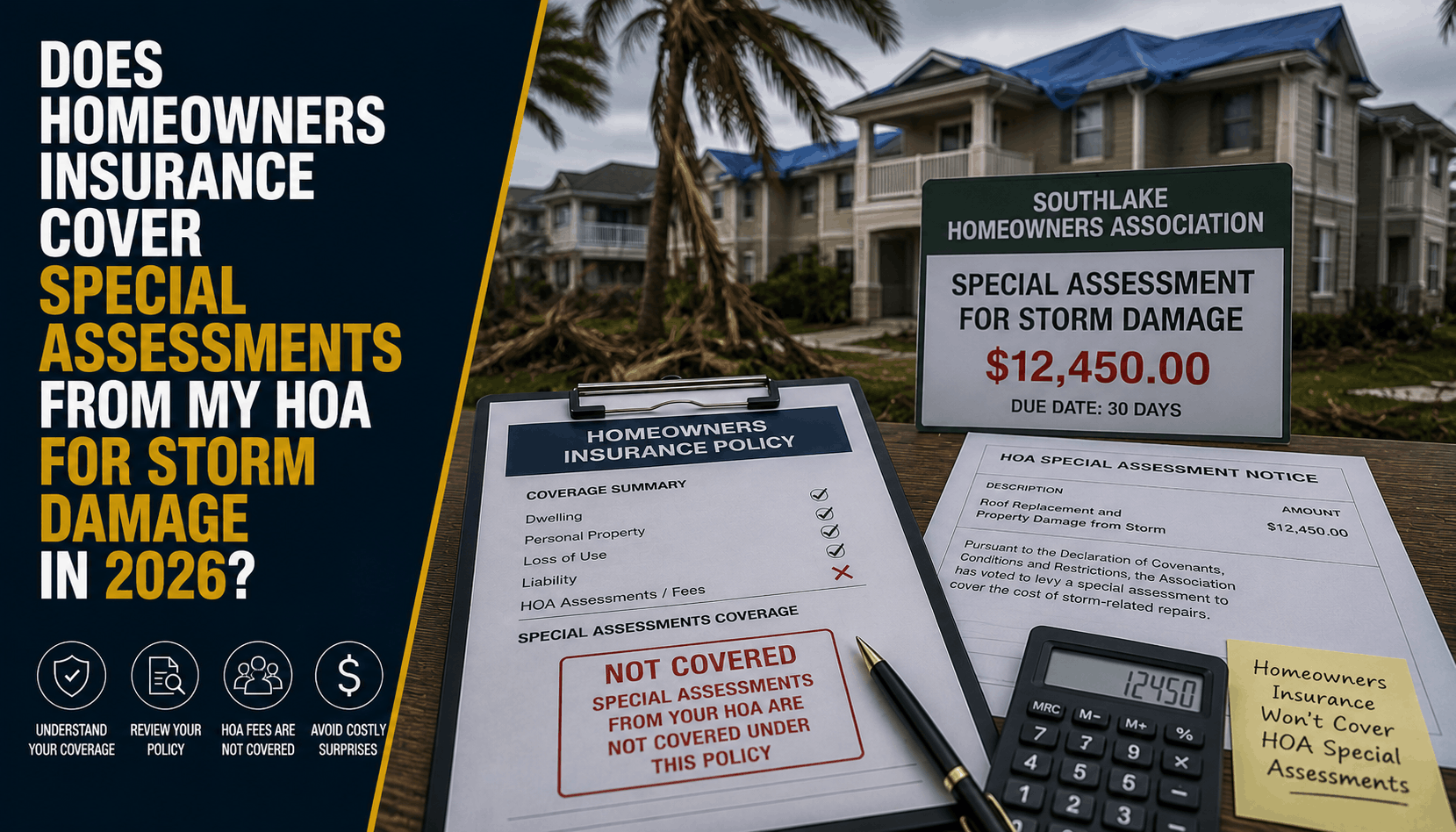

Does Florida Home Insurance Cover HOA Storm Special Assessments? (2026)

Think your Stuart home or condo insurance automatically covers an HOA special assessment after a hurricane? Discover the loss assessment limits leaving local owners exposed.

Read More →

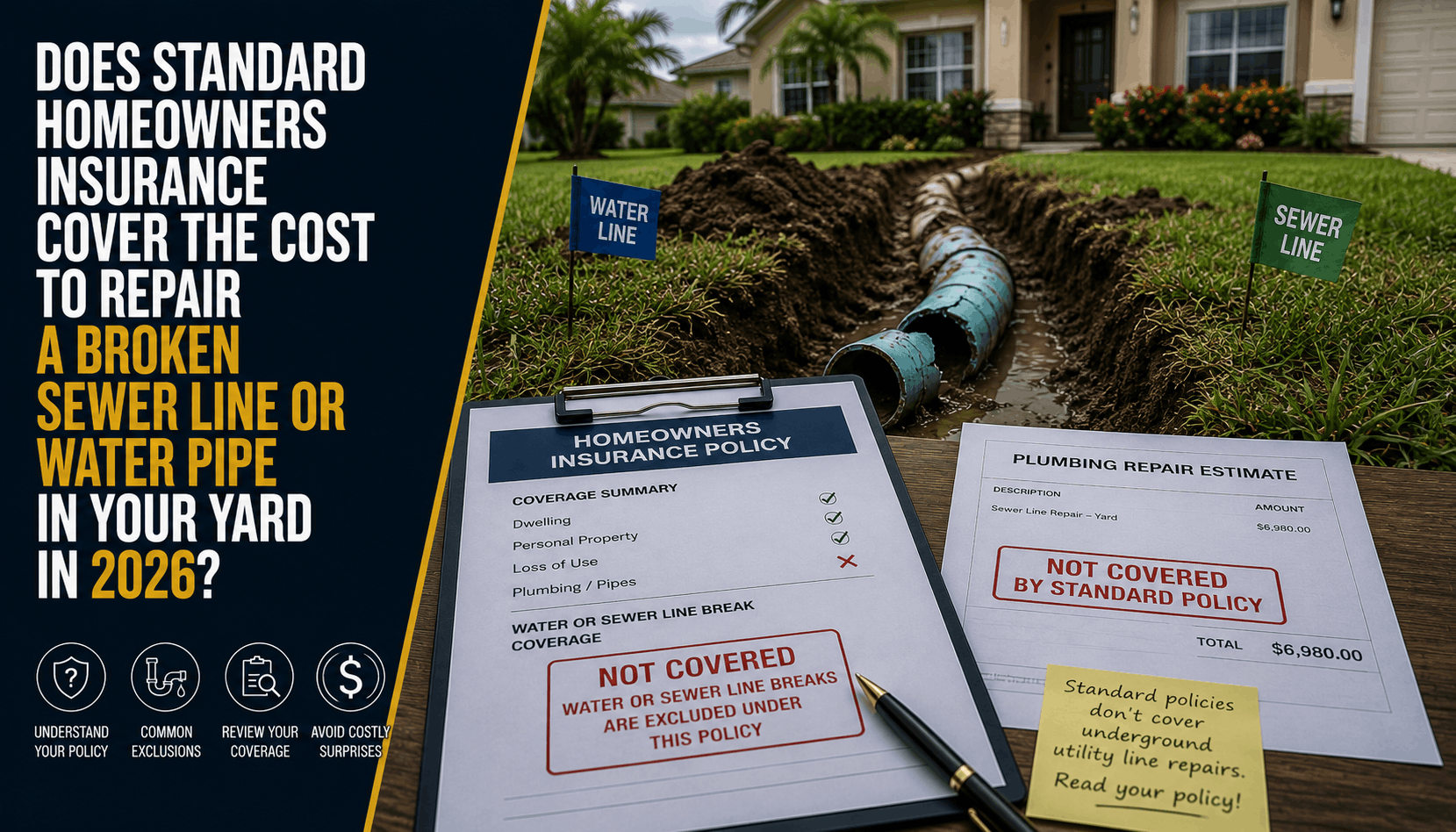

Does Home Insurance Cover Broken Pipes in the Yard? (2026)

Discover why standard homeowners insurance completely denies the cost to repair a broken sewer line or water main in your yard, and how Stuart homeowners can fix this gap.

Read More →