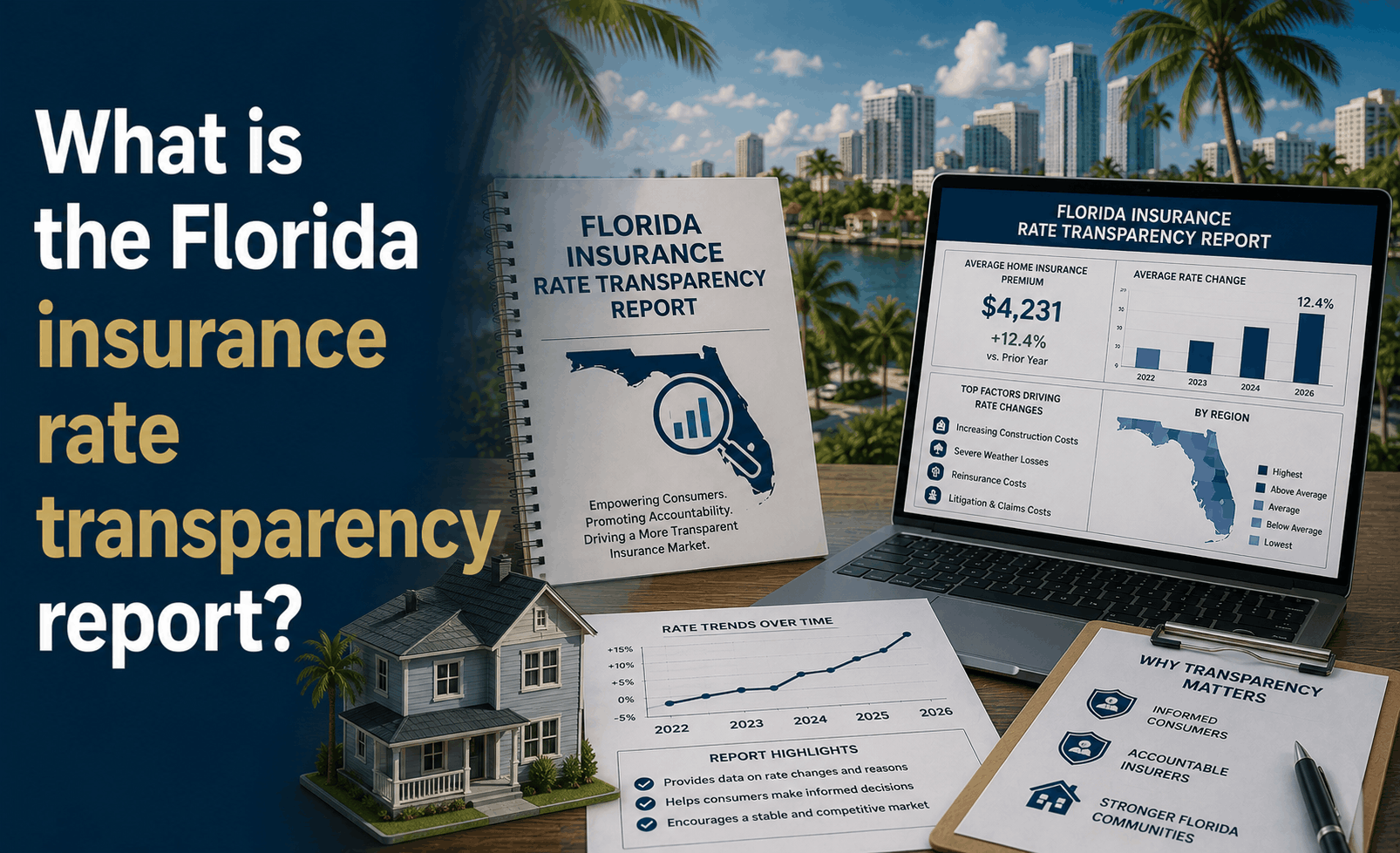

Understanding the Florida Insurance Rate Transparency Report (2026)

What is the Florida Insurance Rate Transparency Report?

The Direct Answer: The Florida Insurance Rate Transparency Report is a comprehensive data publication released by the Florida Office of Insurance Regulation (OIR). Its purpose is to provide homeowners with visibility into how insurance companies are pricing their policies across different counties. In 2026, this report has become the primary tool for consumers to verify the "Tort Reform Dividend"—the expected decrease in premiums following the 2023 legislative changes. It breaks down average premiums, the frequency of rate filings, and the impact of mitigation credits (like new roofs or impact windows) on your final bill.

Essentially, it is the state’s way of ensuring that insurance companies aren't "hiding" savings that should be passed on to you.

1. Why Was This Report Created?

For years, the Florida insurance market was a "black box." Homeowners saw their rates double without knowing if they were being treated fairly compared to their neighbors.

- Accountability: The report forces carriers to justify rate increases in a public forum.

- Market Competition: In 2026, with over 15 new companies entering Florida, the report helps you see which carriers are actually offering lower rates and which are still pricing "high-risk."

- Impact Tracking: It tracks how much the 2023-2024 legislative reforms have actually lowered the "litigation tax" in each zip code.

2. Key Metrics Found in the 2026 Report

When you look at the 2026 data, you will find several key indicators that directly affect your wallet:

- Average Premium by Zip Code: A baseline to see if your current bill is "mathematically fair."

- Rate Filing Frequency: Shows how often a company has requested a price hike in the last 24 months.

- Mitigation Credit Utilization: Reports on how much homeowners are saving by using the My Safe Florida Home grants for home hardening.

- Combined Ratio: A technical stat showing a company's profitability. In 2026, a healthy combined ratio means your company is stable and less likely to leave the state.

3. How to Use the Report to Your Advantage

You shouldn't just read the report; you should use it as leverage.

- The "Benchmark" Strategy: If the transparency report shows the average premium for a $400k home in Stuart is $3,500 and you are paying $5,200, it’s a clear signal to shop.

- Carrier Health Check: The report highlights companies with high consumer complaint ratios. In 2026, "cheap" is only good if the company actually pays claims.

- Legislative Savings: In 2026, the report specifically identifies the "Reinsurance Credit." If your carrier isn't lowering your rate despite lower reinsurance costs, the report will highlight that discrepancy.

4. The 2026 "Stabilization" Trend

According to the latest 2026 OIR data, the Transparency Report indicates that for the first time in a decade, Florida’s statewide average rate increase has dropped below 3%. In some inland counties, the report actually shows a net decrease in premiums—a direct result of the reduced litigation and increased competition tracked by the OIR.

Why Working with an Independent Agency is Vital

The Rate Transparency Report is massive and full of complex data. At Walker Insurance Agency, we translate that data into real-world savings for you.

The Walker Advantage:

- OIR Data Integration: We cross-reference your quote with the OIR’s transparency data to ensure you are getting the most competitive rate in Florida.

- Carrier Stability Analysis: We don't just look at the price; we use the report’s financial data to ensure we only place you with carriers that have a "long-term" commitment to Florida.

- Mitigation Maximization: We show you exactly which credits the OIR report says are yielding the biggest discounts right now.

FAQ

1. Where can I find the Florida Insurance Rate Transparency Report? It is available on the Florida Office of Insurance Regulation (OIR) website. It is updated quarterly to reflect new rate filings and market shifts.

2. Does the report tell me exactly what my rate will be? No. It provides averages. Your specific rate depends on your home’s age, roof condition, distance to the coast, and your personal credit-based insurance score.

3. Does the report cover Flood Insurance? Primarily, the report focuses on property and casualty (Homeowners). Private flood insurance data is increasingly included, but NFIP (federal) rates are governed separately.

4. Why is my rate still high if the report says the market is stabilizing? Market stabilization takes time to reach every renewal. Additionally, if your Coverage A (Rebuild Cost) increased due to 2026 inflation, your premium may rise even if the "rate" per thousand dollars of coverage stayed flat.

Don’t Overpay in a Stabilizing Market

Knowledge is power in the Florida insurance market. The 2026 Transparency Report shows that savings are possible—but only if you know where to look.

Get a Data-Driven Quote today. Contact Walker Insurance Agency for a 2026 Market Review. We provide the visibility you need to ensure your rate matches the current reality of the Florida market.

[GET A FREE QUOTE TODAY] Call us at +1-407-977-7100 or visit our office in Stuart, FL. Let us help you protect your home for less.

Related Articles

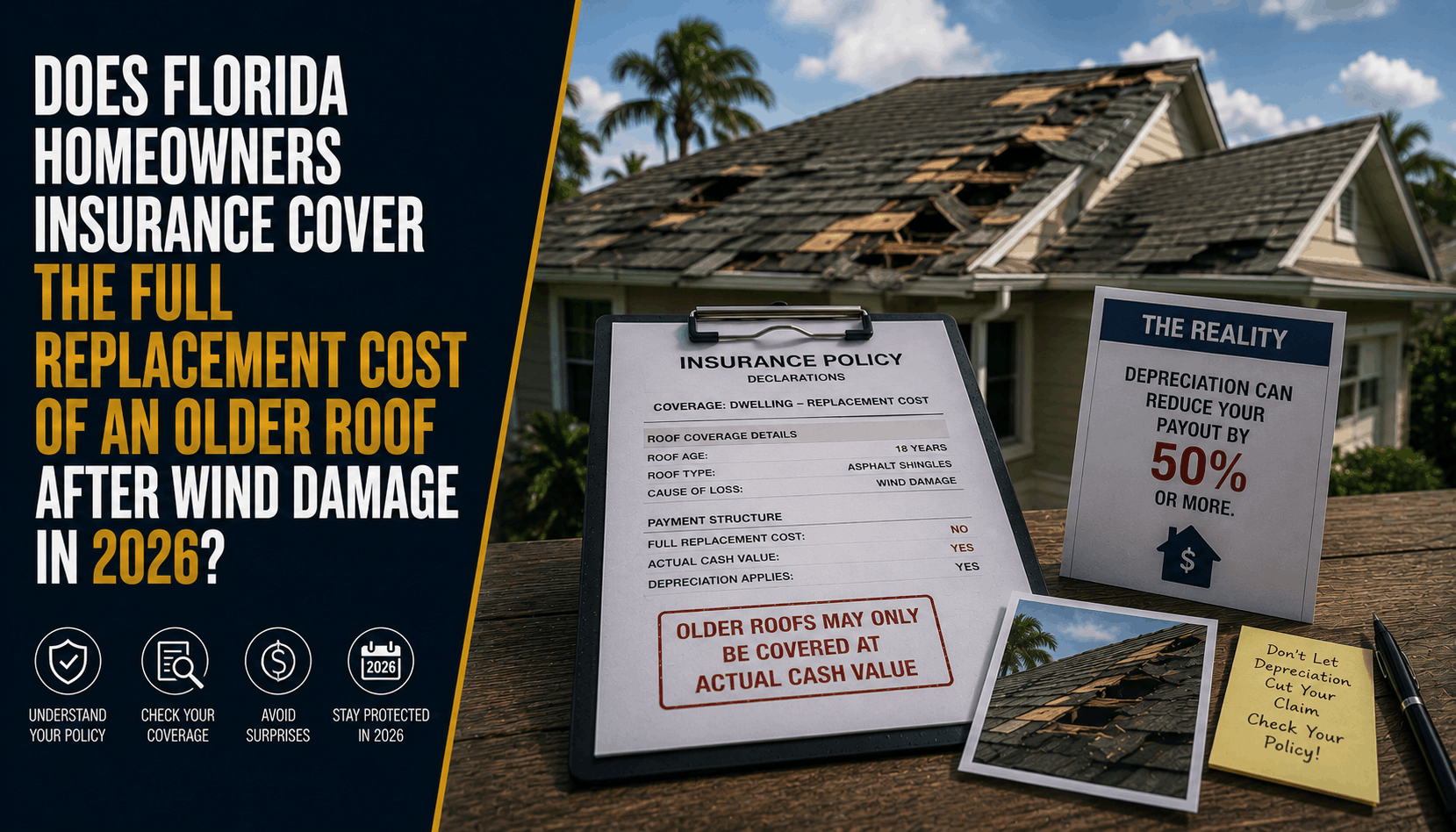

Does Florida Home Insurance Cover Roof Replacement Cost in 2026?

Think your Florida home insurance covers 100% of a new roof after wind damage? Learn how new 2026 guidelines leave Stuart homeowners paying out of pocket.

Read More →

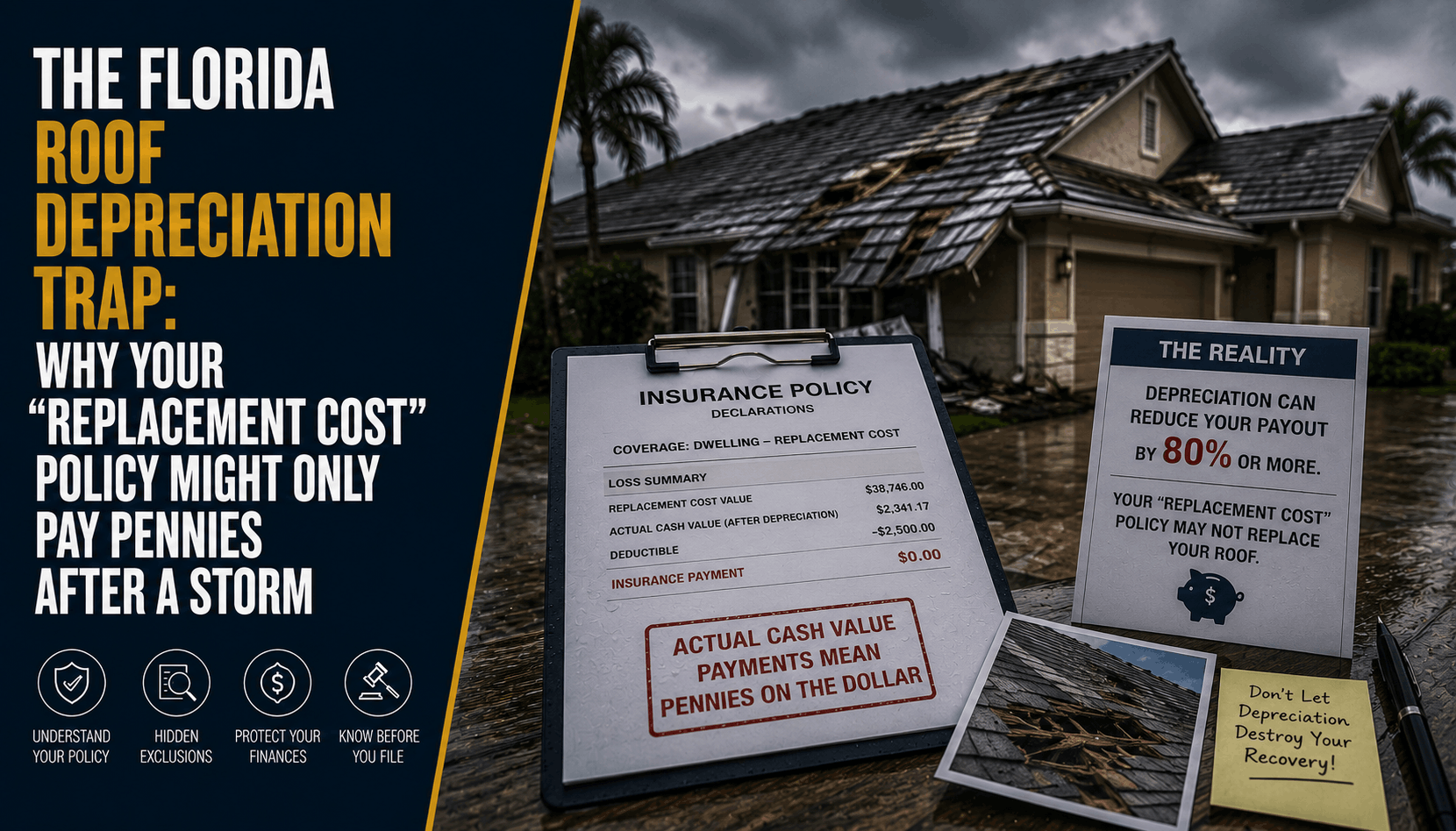

The Florida Roof Depreciation Trap: Why RCV Policies Fail in 2026

Think your Florida home insurance covers 100% of a new roof after a hurricane? Discover the "Roof Surface Payment Schedule" trap leaving Stuart homeowners exposed.

Read More →

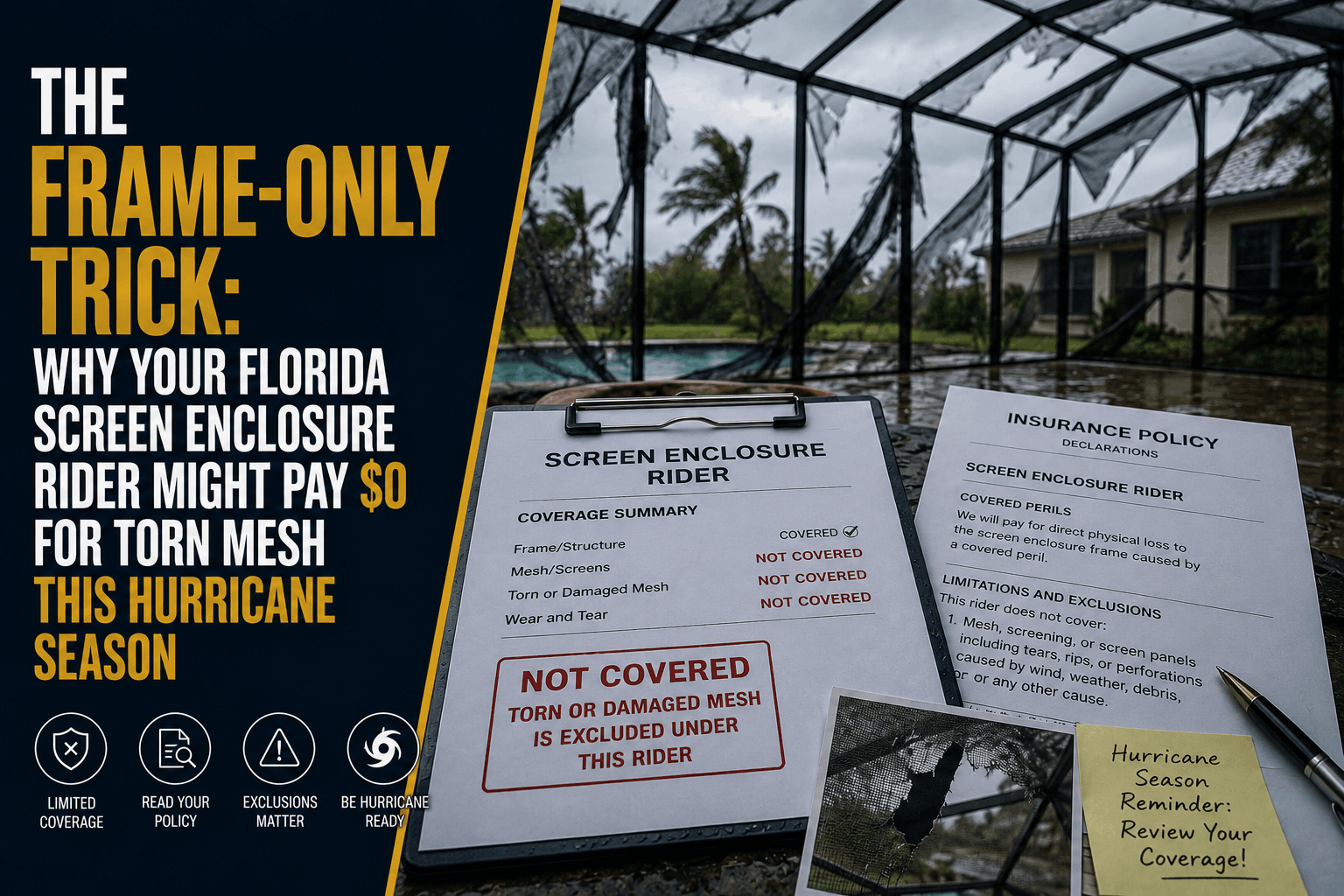

The Frame-Only Trick: Why Pool Enclosure Insurance Fails in 2026

Think your Florida screen enclosure rider covers everything? Discover "The Frame-Only Trick" that leaves homeowners paying 100% out of pocket for torn mesh this hurricane season.

Read More →