The Safety Subsidy: How Safe Florida Drivers Subsidize High-Risk Motorists (2026)

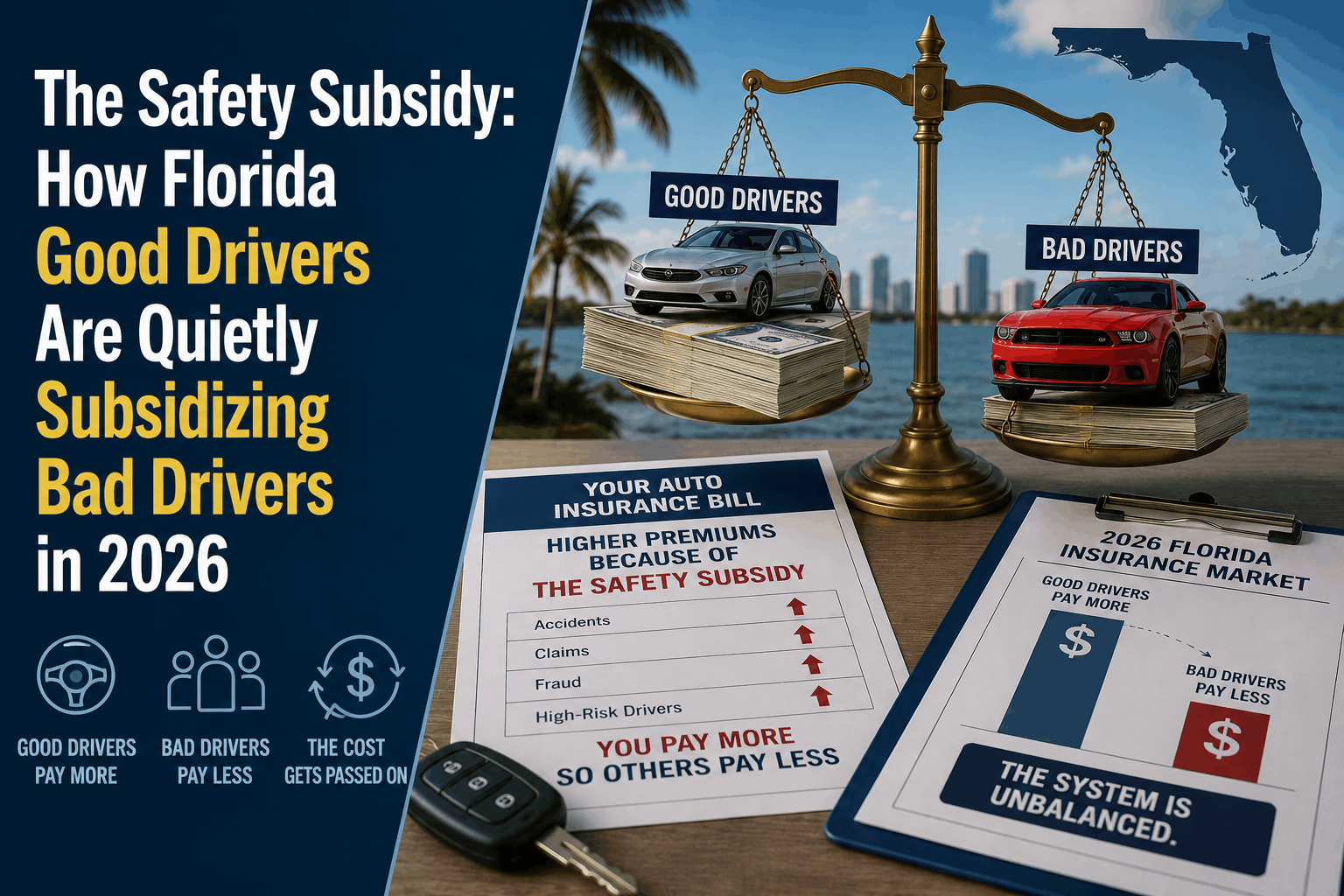

The Safety Subsidy: How Florida Good Drivers Are Quietly Subsidizing Bad Drivers in 2026

The Direct Answer: The "Safety Subsidy" is an insurance underwriting phenomenon where drivers with completely clean records pay artificially high premiums to absorb the financial losses caused by high-risk, accident-prone motorists. In 2026, this hidden tax is more transparent than ever. Following massive tort reforms, the Florida Office of Insurance Regulation (OIR) approved sweeping baseline rate rollbacks—including an 8% drop from Progressive, 10.1% from State Farm, and 7% from USAA.

However, because these rate cuts are applied across broad, generalized geographic risk pools, safe drivers who auto-renew without shopping are still overpaying. They are essentially funding the claims of the reckless drivers sharing their zip codes.

To achieve total visibility over your car expenses, you must realize that standard insurance pooling inherently penalizes your safe driving habits unless you actively force the system to unbundle your specific risk.

1. The Mechanics of the Hidden Subsidy

Insurance companies operate on the law of large numbers. They group drivers into broad risk pools based primarily on zip code, age, and vehicle type.

- The Problem: If you live in a high-traffic or flood-prone area of Florida, your premium is automatically dragged upward by the sheer volume of accidents, distracted driving citations, and fraud occurring around you.

- The Baseline Trap: Even though successful 2023–2024 legal reforms slashed Florida's personal auto liability loss ratio to a stable 52.5%—the lowest level in 15 years—the resulting premium drops are being distributed evenly across renewal brackets.

- The Reality: If you have zero accidents and zero tickets over the past 3 to 5 years, you are historically highly profitable for an insurer. Your premium is being used as a cash buffer to offset the soaring costs of repairing tech-heavy vehicles wrecked by high-risk drivers.

2. Breaking the Pool: Telematics and Personal Pricing

In 2026, the only way to stop paying the Safety Subsidy is to legally demand personalized pricing. The technology to do this has fully matured through carrier telematics programs (user-based insurance apps).

[Standard Risk Pool] ──> You pay the average zip code rate (Subsidizing bad drivers).

[Telematics Track] ──> You pay ONLY for your actual braking, speed, and mileage data.

By opting into safe-driving monitoring programs—such as Progressive's Snapshot, State Farm's Drive Safe & Save, or GEICO's DriveEasy—you pull your profile completely out of the generalized pool. In 2026, Florida carriers are offering up to 10% to 15% in immediate sign-up discounts, with top-tier safe drivers capturing permanent premium reductions of up to 30% at renewal. If you drive carefully and preserve your clean record, hiding your data is actively costing you money.

3. Stacking the 2026 Deflation Dividend

Because 42 auto insurance companies in Florida have filed for rate decreases over the last year, safe drivers have unprecedented leverage. You can compound these market rollbacks by constructing a safe, structural "Discount Stack":

- The Market Base: Capture the active 7% to 10.1% premium cuts hitting major carriers this month.

- The Mature Driver Course (Ages 55+): Completing a state-approved, 6-hour online accident prevention course legally guarantees an extra 3% to 10% statutory reduction under Florida law.

- The Low-Mileage Adjustment: If you work remotely or have retired, updating your annual mileage parameters below 7,500 miles can shave an additional 10% off your liability lines.

- Administrative Credits: Layering paperless billing and EFT automatic monthly payments strips out administrative surcharges, saving another 5%.

Why Working with an Independent Agency is Vital

Allowing your policy to auto-renew on a smartphone application guarantees you will continue paying the Safety Subsidy. Automated carrier software is built to protect the average profitability of the pool, not your individual wallet. At Walker Insurance Agency, we provide the data-driven visibility you need to isolate your safe driving record and purchase coverage at its true mathematical cost.

The Walker Advantage:

- Carrier Quoting Arbitrage: We cross-reference your clean record against the entire 2026 Florida marketplace to locate the specific carriers currently offering the highest credits for low-risk drivers.

- Telematics Neutrality: We help you evaluate different carrier tracking apps to ensure you pick a program that rewards your specific driving route without hitting you with unfair penalties.

- Comprehensive Risk Optimization: We ensure your falling auto premiums are correctly balanced with your home insurance credits, securing maximum multi-policy bundling savings in Stuart.

FAQ

1. Is my insurance company allowed to raise my rate if a telematics app records a hard brake?

Under 2026 Florida insurance regulations, a single hard-braking incident will not spike your baseline rate. Telematics programs analyze long-term, aggregated behavior patterns over a 90-day window. While poor driving can result in losing your optional safe-driving discount, carriers use this data primarily to calculate premium reductions, not surcharges.

2. Why should I shop my policy if the state says rates are dropping by 8% anyway?

An 8% average drop is a statewide figure. Some individual carriers have cut rates by as much as 16.5%, while others are holding lines flat. If your current carrier filed a minor rate adjustment but a competitor just introduced an aggressive rollback for safe drivers, staying put means you are overpaying.

3. Does my credit score impact the Safety Subsidy?

Yes. Florida law allows insurers to utilize a credit-based insurance score. Drivers with excellent financial histories are statistically proven to file fewer claims. If your credit score has improved recently, an independent agent can re-run your profile to unlock hidden tier discounts.

Stop Funding the Mistakes of Careless Drivers

The 2026 Florida insurance market has finally turned a corner, and pricing control has shifted back to the consumer. If you have maintained a clean record, you have earned the right to the lowest premium floor allowed by state law.

Reclaim your safe driver bonus today. Contact Walker Insurance Agency for a comprehensive 2026 Premium Audit. We provide the visibility you need to isolate your profile, break free from high-risk pools, and secure the true value of your safe driving habits in Stuart.

[GET A FREE QUOTE TODAY]

Call us at +1-407-977-7100 or visit our office in Stuart, FL. Let us lower your premium today.

Related Articles

Does Homeowners Insurance Cover Trampolines or Pool Slides? (2026)

Planning summer fun in Stuart, FL? Discover why trampolines and pool slides are major homeowners insurance liability traps that can lead to dropped coverage.

Read More →

Does Home or Auto Insurance Cover Boating Accidents? (2026)

Planning a boat day in Stuart? Learn why relying on your home or auto insurance policies for watercraft liability is a dangerous financial gap.

Read More →

Why Home and Auto Insurance Won't Cover Boat Accidents (2026)

Planning a July boat day in Stuart, FL? Discover why relying on your home or auto insurance policies for watercraft liability is a dangerous financial blindspot.

Read More →