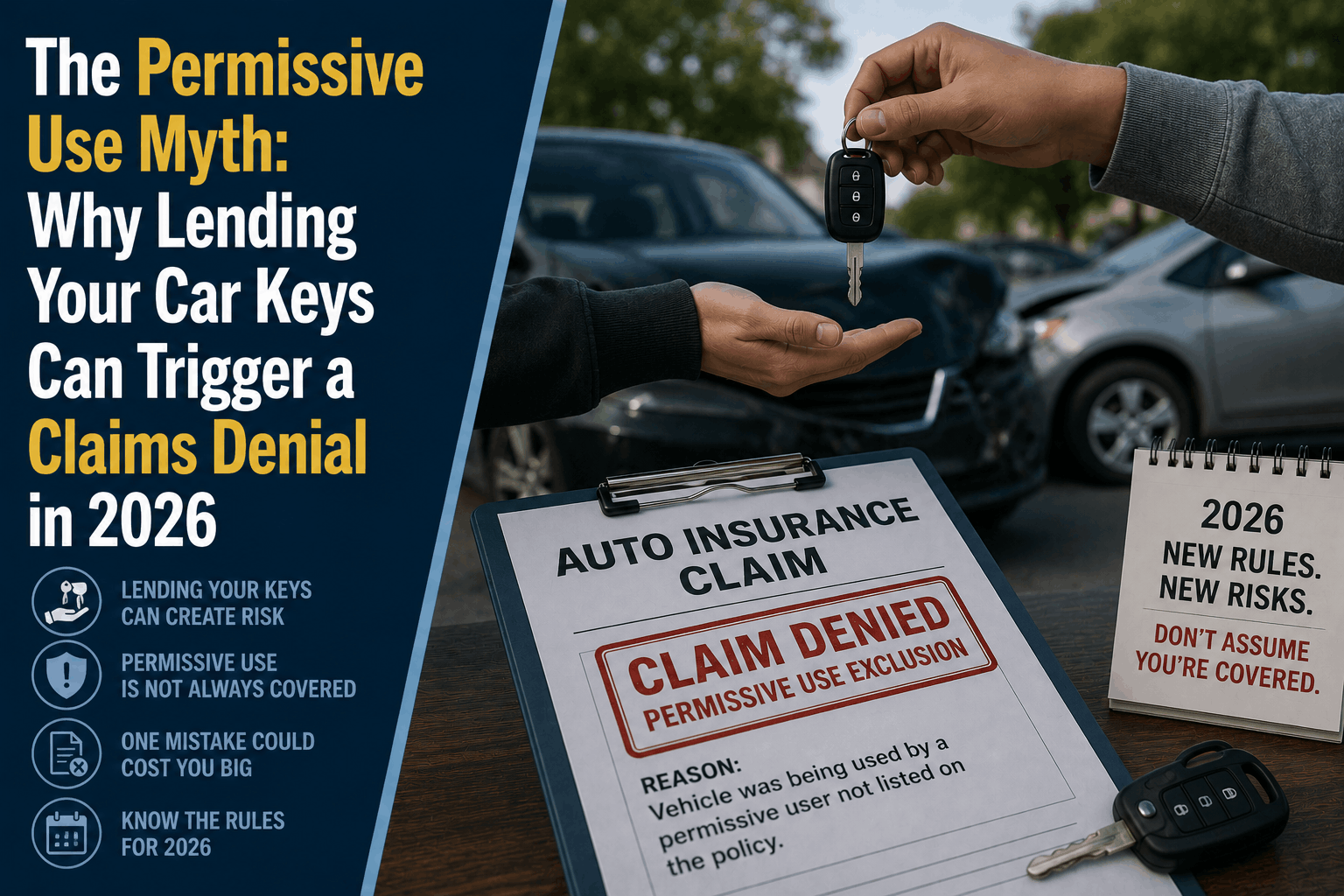

The Permissive Use Myth: Why Lending Your Car Keys Can Trigger a Claims Denial in 2026

The Permissive Use Myth: Why Lending Your Car Keys Can Trigger a Claims Denial in 2026

The Direct Answer: The "Permissive Use Myth" is the widespread belief that auto insurance automatically follows the vehicle, guaranteeing full coverage whenever you lend your car keys to a friend, neighbor, or extended family member. It does not. In 2026, as major carriers face rising claim payouts and aggressively tighten their policy loopholes, relying on unverified "permissive use" is one of the fastest ways to trigger an absolute claims denial.

A wave of landmark appellate court rulings has officially upheld an insurer's legal right to completely deny coverage if a permissive driver violates specific hidden exclusions—such as driving without a valid license, using the vehicle for an unlisted business purpose, or exceeding a strict "regular use" frequency threshold.

To achieve total visibility over your financial protection, you must realize that lending your keys is no longer a casual favor. If your borrower crashes your vehicle and triggers a policy exclusion, you can be held personally liable for 100% of the physical and medical damages.

1. The 2026 Legal Crackdown: "Permitted but Not Entitled"

For decades, the insurance industry leaned on standard "omnibus clauses" to cover occasional, authorized drivers. However, modern policies use highly technical gatekeeping language that fundamentally alters this dynamic:

- The "Reasonable Belief" Loophole: Standard policy language explicitly excludes liability coverage for any individual "using a vehicle without a reasonable belief that they are entitled to do so."

- The Unlicensed Driver Trap: In historic decisions handed down by state appellate courts, judges ruled that a driver cannot have a "reasonable belief of entitlement" if they do not possess a valid driver's license.

- The Fallout: If you lend your truck to a friend whose license is suspended, and they cause an accident, your carrier will legally deny the claim. It is legally irrelevant that you gave them explicit, verbal permission; the driver's lack of a valid license completely breaks the contract.

2. The 3 Structural Triggers of a Permissive Use Denial

In the current auto insurance climate, claims adjusters utilize advanced data-mining software to investigate the exact circumstances of a collision before paying out a dime. If an unlisted driver is behind the wheel, the insurer will aggressively audit three specific risk categories:

\[Unlisted Driver Collision\]

│

┌───────────────────────┼───────────────────────┐

▼ ▼ ▼

[The Frequency Trap] [The Household Rule] [The Commercial Box]

Borrowed > 12 times Lives with you but Used for rideshare,

per year? = DENIED. not listed? = DENIED. delivery, etc. = DENIED.

Trigger 1: The "Regular Use" Frequency Cap

Permissive use is contractually reserved for occasional or emergency borrowing. Most carriers now define "regular use" as borrowing a vehicle several times a month or more than 12 times in a single calendar year. If your babysitter or neighbor borrows your car every Friday to pick up groceries, they cross the line from a permissive user to a regular operator. If they crash on trip number 13, the insurer will deny the claim for failing to add them to the policy.

Trigger 2: The Unlisted Household Resident Violation

This is the number-one reason permissive use claims fail. If a driver lives under your roof—whether it is a roommate, a relative, or a teenager with a fresh permit—they cannot qualify for permissive use. Insurance contracts assume that anyone residing in the household has regular access to the keys. If a co-resident drives your vehicle but isn't explicitly named as an active or excluded driver on your policy declarations page, an accident claim will face an immediate, automated denial for rate evasion.

Trigger 3: The Commercial Use Exclusion

If your friend borrows your vehicle for an afternoon, but uses that time to log into a gig-economy app like Uber, Lyft, DoorDash, or a mobile detailing business, your personal auto insurance is entirely void. Standard policies carry absolute commercial exclusions. The second your car is used to transport goods or passengers for profit, the baseline policy shuts down completely.

3. The Financial Danger: Step-Down Limits

Even if your carrier approves a permissive use claim, you may still face massive out-of-pocket exposure due to a mechanism known as Step-Down Limits:

The Rule: Many modern non-standard and preferred policies dictate that when an unlisted permissive driver operates the vehicle, your custom liability limits (e.g., $100,000/$300,000) instantly "step down" to the state's absolute minimum financial responsibility limits.

If your policy drops to minimum state limits while your unlisted driver causes a multi-car collision, your insurance carrier will pay out to the lower threshold and stop completely. Any excess medical judgments or vehicle repair costs will fall squarely on your shoulders, threatening your home, savings, and future wages.

Why Working with an Independent Agency is Vital

Allowing your auto policy to sit on autopilot with a faceless digital application leaves your household entirely exposed to modern underwriting traps. At Walker Insurance Agency, we provide the data-driven visibility you need to understand the true legal boundaries of your coverage.

The Walker Advantage:

- Policy Endorsement Audits: We meticulously analyze your policy jacket to identify hidden step-down limits or absolute unlicensed-driver exclusions before you ever lend your keys.

- Household Composition Syncing: We help you properly structure your named, deferred, or excluded driver lists to prevent automated resident denials in Stuart.

- Umbrella Safety Layering: We design Personal Umbrella Policies (PUP) that sit on top of your primary auto lines, expanding your liability shield to $1 million or more to defend against catastrophic, multi-driver litigation.

FAQ

1. Does my car insurance cover my teenager who is driving on a learner's permit?

While common practice assumes a learner's permit is covered under parental supervision, it is not a structural contractual guarantee in standard policies. To protect your coverage, you must formally notify your independent agent the moment your teen receives their permit to ensure they are properly rated and recognized by the carrier.

2. What happens if someone takes my car without permission and crashes it?

This is legally classified as "non-permissive use" or theft. If a vehicle is taken unlawfully, your liability coverage will not pay for the other party's damages because you did not authorize the operation. Your vehicle's physical damage will be handled strictly through your policy's Comprehensive coverage, provided you file a formal police report against the driver.

3. If my friend has excellent auto insurance, does their policy apply if they borrow my car?

In most jurisdictions, auto insurance follows the vehicle first. Your policy acts as the primary insurance to cover the damages. If the total destruction exceeds your maximum policy limits, your friend’s personal auto insurance may step in as secondary coverage to bridge the financial gap.

Protect Your Wealth Before You Hand Over the Keys

In the modern insurance environment, a casual favor can transform into a life-altering financial liability in a matter of seconds. Real peace of mind requires knowing exactly who is contractually protected by your premium before an emergency occurs on the highway.

Verify your permissive use terms today. Contact Walker Insurance Agency for a comprehensive 2026 Policy Review. We provide the visibility you need to eliminate hidden step-down limits, secure your household driver tiers, and shield your investments safely in Stuart.

[GET A FREE QUOTE TODAY]

Call us at +1-407-977-7100 or visit our office in Stuart, FL. Let us safeguard your assets today.

Related Articles

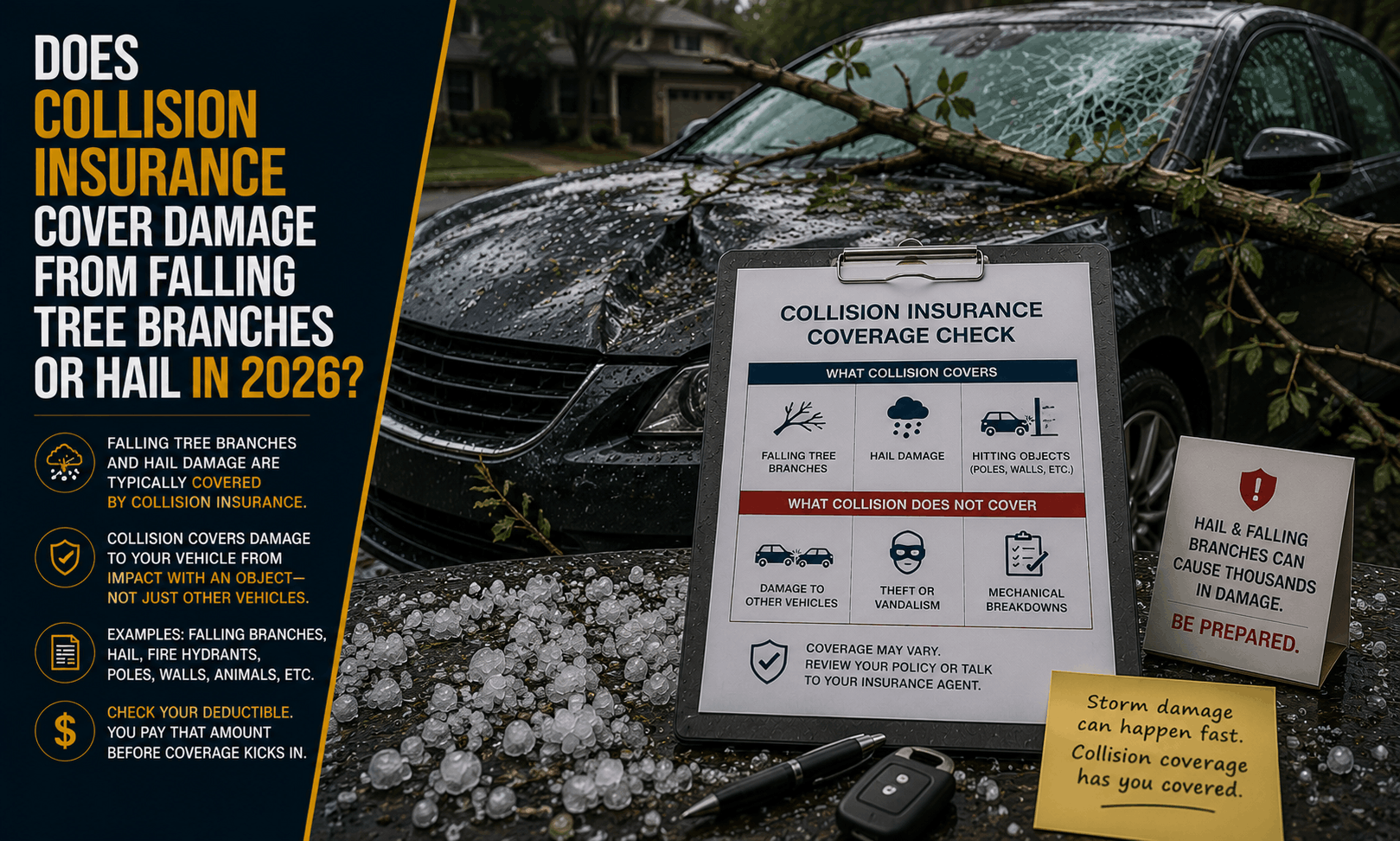

Does Collision Insurance Cover Hail & Tree Damage in 2026?

Did hail or a falling tree branch damage your car? Learn why collision auto insurance won't pay for storm damage and how comprehensive coverage protects you.

Read More →

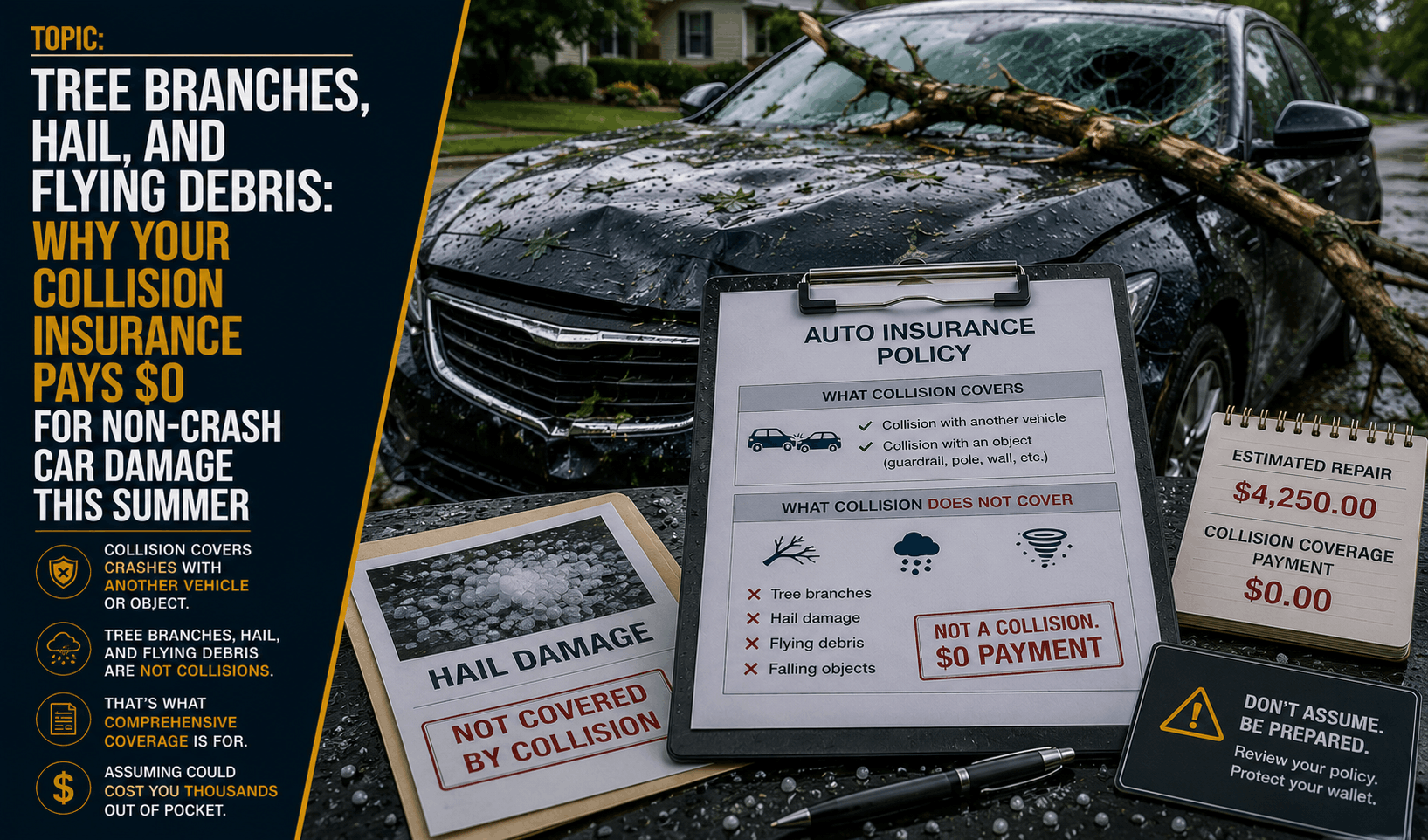

Why Collision Insurance Pays $0 for Non-Crash Summer Damage (2026)

Did a tree branch, hail storm, or flying road debris hit your car this summer? Discover why collision auto insurance pays $0 and how comprehensive coverage protects you.

Read More →

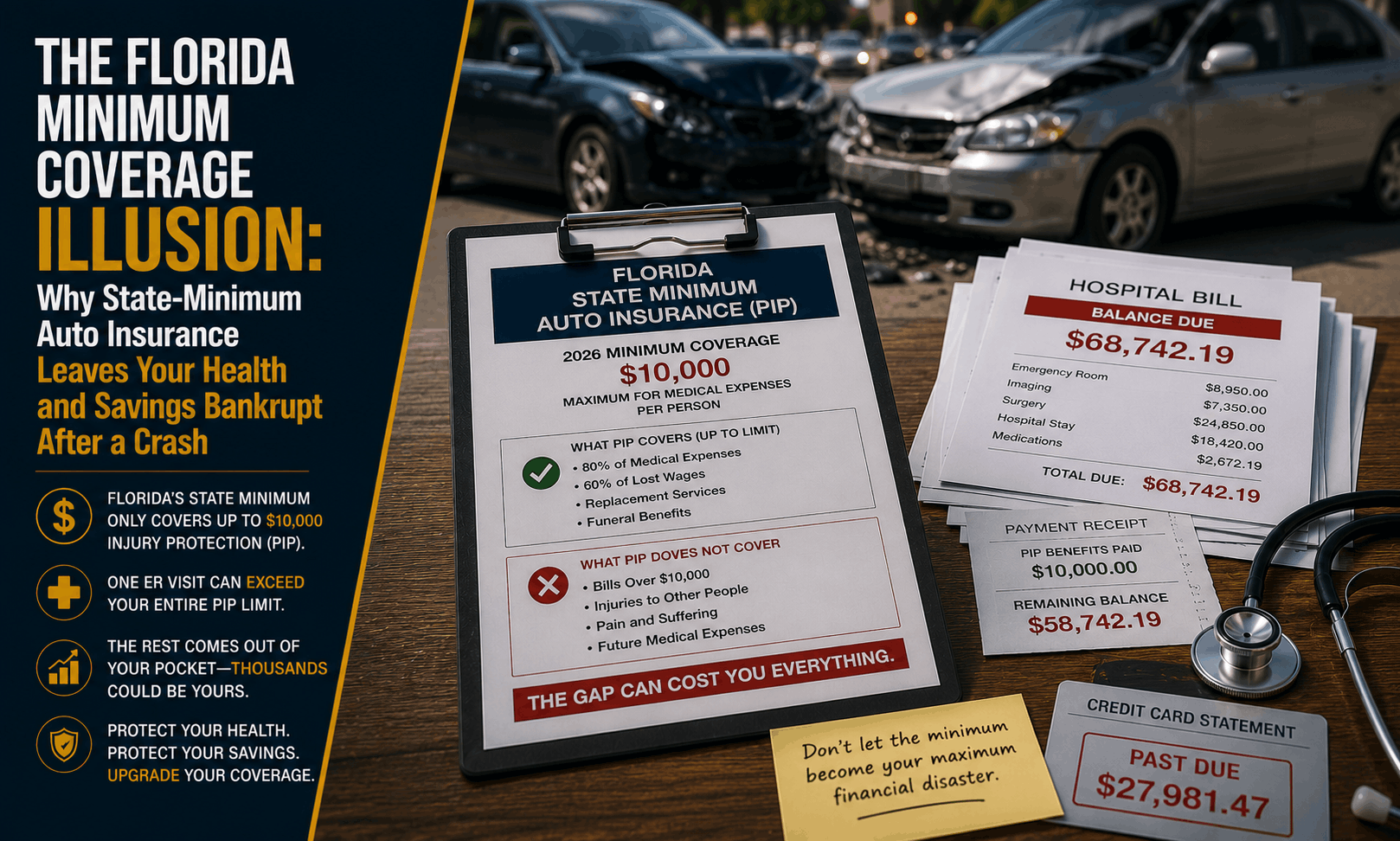

Florida Minimum Auto Insurance Coverage Illusion (2026)

Driving with state-minimum auto insurance in Florida? Learn why carrying only PIP and PDL leaves your health and personal savings vulnerable after a crash.

Read More →