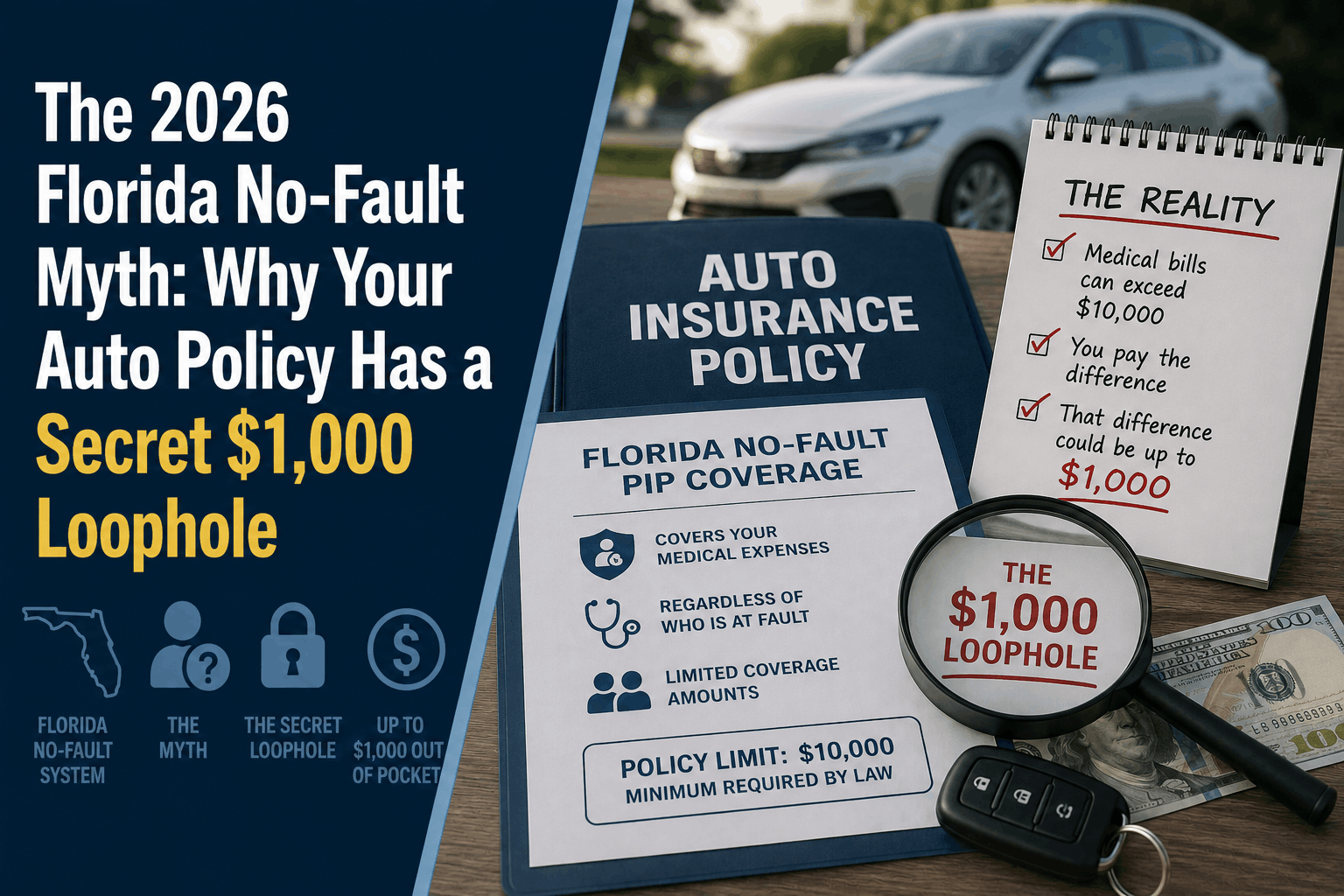

The 2026 Florida No-Fault Myth: The Secret $1,000 PIP Deductible Loophole

The 2026 Florida No-Fault Myth: Why Your Auto Policy Has a Secret $1,000 Loophole

The Direct Answer: The myth of Florida's "No-Fault" auto insurance is the belief that your mandatory $10,000 Personal Injury Protection (PIP) coverage will automatically step in to pay 100% of your initial medical bills after a crash. It does not. The "secret loophole" catching drivers completely off guard in 2026 is the combination of standard $1,000 policy deductibles and PIP's statutory 20% co-insurance gap.

Under Florida Statute § 627.736, PIP only covers 80% of reasonable medical expenses. If you selected a $1,000 deductible to lower your monthly premium, you must pay that first $1,000 out of pocket, plus 20% of all remaining medical bills.

To achieve total visibility over your financial safety net, you must realize that a standard "minimum coverage" policy can easily leave you holding thousands of dollars in medical collection notices—even when the accident wasn't your fault.

1. The Anatomy of the $1,000 Loophole

When shopping for car insurance in Florida’s hyper-competitive 2026 market, online portals love to cross-sell policies with a $1,000 PIP deductible to make the monthly quote look cheaper. It looks great on paper, but the actual claims math is brutal.

Consider a standard emergency room visit after a local collision totaling $4,000 in medical bills:

| Expense Breakdown | With a $1,000 PIP Deductible | With a $0 PIP Deductible |

|---|---|---|

| Total Medical Bill | $4,000 | $4,000 |

| Your Deductible (Paid by You) | $1,000 | $0 |

| Remaining Bill Insured | $3,000 | $4,000 |

| What PIP Pays (80%) | $2,400 | $3,200 |

| Your 20% Co-insurance Share | $600 | $800 |

| Total Out-of-Pocket Cost | $1,600 | $800 |

The Blindspot: In the exact same accident, with the exact same medical bills, selecting that $1,000 deductible option instantly doubles your out-of-pocket exposure.

2. Setting the Record Straight on the "2026 PIP Repeal"

If you have browsed the internet recently, you have likely run into viral headlines or AI summaries claiming that Florida completely repealed its 55-year-old No-Fault system.

This is entirely false. While bills like Senate Bill 522 and House Bill 769 were aggressively pushed by trial attorneys to transition Florida to a fault-based system, both measures died in committee.

Personal Injury Protection (PIP) remains mandatory for all registered vehicles operating in Florida. Because the no-fault system is here to stay, managing your deductible limits remains your primary line of financial defense.

3. The Double-Whammy: Gated Limits & Timelines

The deductible isn't the only trap inside your 2026 PIP policy. To even access your coverage, you must clear two structural hurdles:

- The 14-Day Initial Treatment Rule: You must seek professional medical treatment within exactly 14 days of the accident. If you wait until day 15 because you thought your neck stiffness would go away, your insurer has the statutory right to deny your PIP claim entirely.

- The Emergency Medical Condition (EMC) Gate: Even if you see a doctor within two weeks, your PIP medical benefit is strictly capped at $2,500 unless a licensed MD, DO, or chiropractor explicitly documents that you suffered an Emergency Medical Condition (EMC).

If you are capped at $2,500 and carry a $1,000 deductible, your policy will only pay out a maximum of $1,200, leaving you to handle the rest of your hospital bills entirely on your own.

How to Safely Close the No-Fault Loophole

You should absolutely exploit the 8% average auto rate cuts hitting the Florida market this month, but do not do it by watering down your medical protections.

At Walker Insurance Agency, we advise Florida drivers to close the no-fault gap using a two-step structural layout:

Step 1: Reduce Your PIP Deductible to $0

Step 2: Stack Medical Payments (MedPay) Coverage

================================================

= 100% Out-of-Pocket Medical Protection

By adding Medical Payments (MedPay) coverage to your policy, you create a seamless shield. MedPay is designed to step in and pay that missing 20% co-insurance gap that standard PIP leaves behind. If you carry a $0 PIP deductible paired with MedPay, your out-of-pocket exposure for an accidental medical bill drops to exactly zero.

Why Working with an Independent Agency is Vital

In a legal environment where insurance carriers use automated software to look for technical exclusions, buying a policy off a faceless smartphone application is an unnecessary financial gamble. At Walker Insurance Agency, we provide the data-driven visibility you need to stay protected.

The Walker Advantage:

- Deductible Exposure Audits: We review your current auto declarations page to expose hidden PIP deductibles that could compromise your savings.

- MedPay Stacking Optimization: We cross-reference quotes from the top private carriers in Florida to find companies that bundle MedPay affordably.

- Fault-Law Integration: We ensure your policy limits are balanced against Florida’s updated Modified Comparative Negligence (51% fault) laws, keeping your family safe from third-party liability exposure.

FAQ

1. If the accident wasn't my fault, can't I make the other driver's insurance pay my $1,000 deductible?

Eventually, yes. You or your medical providers can pursue a bodily injury liability claim against the at-fault driver to recover your out-of-pocket deductible and co-insurance. However, those liability settlements can take months or years to resolve. Your hospital bills will arrive in your mailbox within 30 days.

2. Can I change my PIP deductible to $0 in the middle of my policy term?

Yes. You do not have to wait for your formal six-month policy renewal. An independent agent can log into your carrier portal and update your deductible lines instantly, which usually only adds a few dollars to your monthly premium.

3. Does health insurance cover what PIP doesn't pay?

If you have private health insurance or Medicare, it can act as secondary coverage to pay for the 20% co-insurance gap or expenses that exceed your PIP limits. However, your health insurance will still apply its own standard deductibles and copays to the bill.

Don't Let a Cheap Policy Break Your Retirement Budget

In the modern Florida market, an auto policy configured with incorrect deductibles isn't a safety net—it's a financial trap waiting to spring during a highway emergency.

Expose your policy gaps today. Contact Walker Insurance Agency for a comprehensive 2026 Rate and Coverage Audit. We provide the visibility you need to eliminate hidden deductibles, maximize current market rate rollbacks, and drive with absolute peace of mind in Stuart.

[GET A FREE QUOTE TODAY]

Call us at +1-407-977-7100 or visit our office in Stuart, FL. Let us safeguard your wallet today.

Related Articles

Does Homeowners Insurance Cover Trampolines or Pool Slides? (2026)

Planning summer fun in Stuart, FL? Discover why trampolines and pool slides are major homeowners insurance liability traps that can lead to dropped coverage.

Read More →

Does Home or Auto Insurance Cover Boating Accidents? (2026)

Planning a boat day in Stuart? Learn why relying on your home or auto insurance policies for watercraft liability is a dangerous financial gap.

Read More →

Why Home and Auto Insurance Won't Cover Boat Accidents (2026)

Planning a July boat day in Stuart, FL? Discover why relying on your home or auto insurance policies for watercraft liability is a dangerous financial blindspot.

Read More →