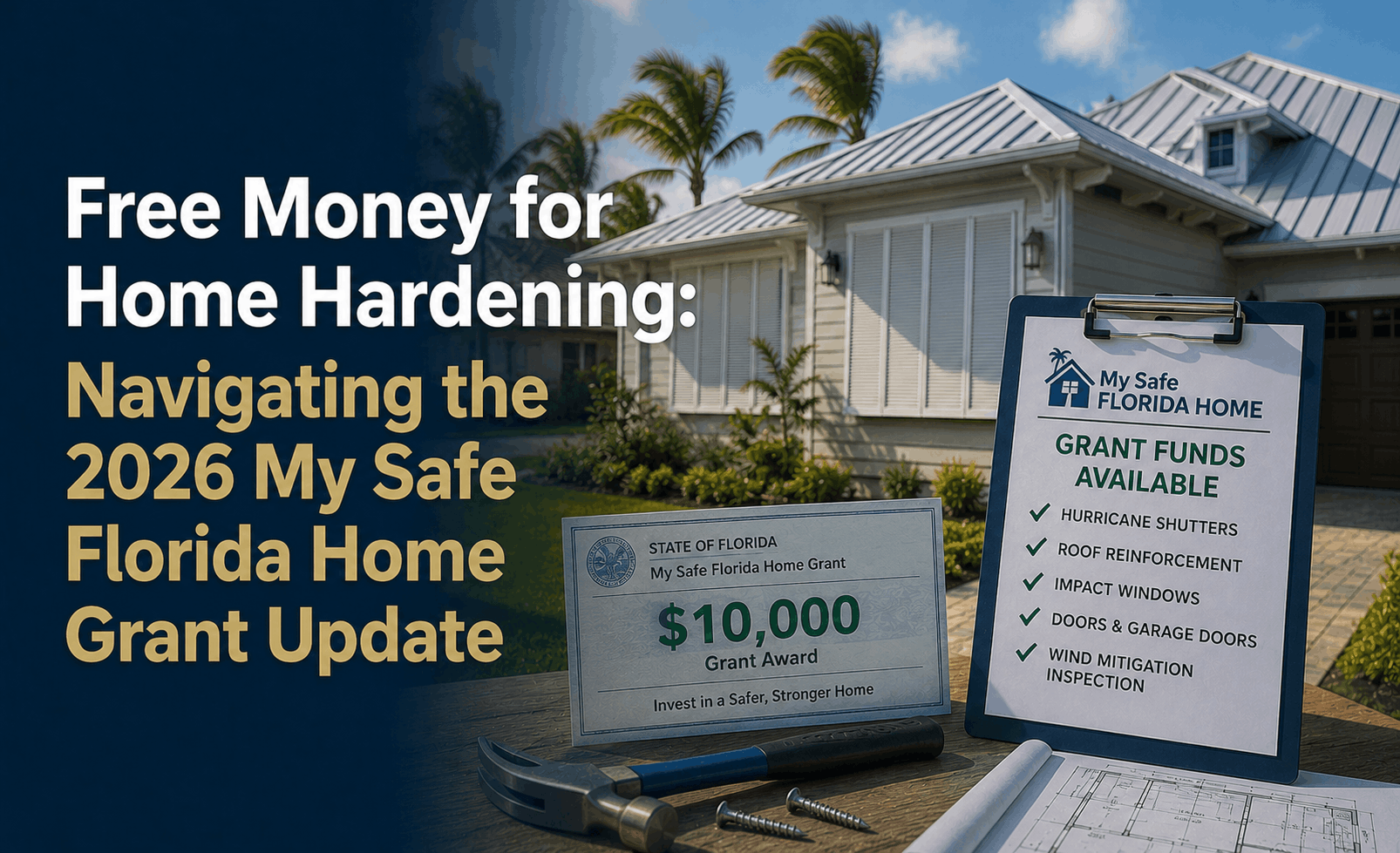

My Safe Florida Home Grant 2026 Update: How to Get $10,000

Free Money for Home Hardening: Navigating the 2026 My Safe Florida Home Grant Update

The Direct Answer: As of May 2026, the My Safe Florida Home (MSFH) program has been revitalized with over $600 million in new funding for the 2026-2027 cycle. Eligible homeowners can receive a matching grant of up to $10,000 (where the state pays $2 for every $1 you spend) to upgrade windows, doors, and roofs. Crucially, low-income homeowners now qualify for the full $10,000 with no matching required. In 2026, the program uses a strict prioritization schedule based on age and income, meaning the "free money" is now more accessible to those who need it most, provided you follow the precise eight-step application sequence.

To achieve total visibility over these funds, you must act before the 2026-2027 appropriation is exhausted—which historically happens within weeks of the portal opening.

1. What’s New for 2026?

The Florida Legislature has significantly modified the program under HB 811 and subsequent 2026 budget approvals to address the massive backlog and skyrocketing insurance premiums.

- Expanded Eligibility: The maximum "Insured Value" (Coverage A) for a home has been raised to $700,000 (up from $500,000). Low-income applicants are exempt from this cap entirely.

- Prioritization Queue: Unlike previous years where it was a "free-for-all," 2026 applications are opened in staggered windows:

- Low-income homeowners age 60+.

- Low-income homeowners (any age).

- Moderate-income homeowners (below 120% AMI) age 60+.

- Moderate-income homeowners (below 120% AMI).

- Backlog Clearance: $480 million of the 2026 budget is specifically designated to fund the 45,000 homeowners stuck in the "Inspection Completed" phase from last year.

2. The Grant Math: 2-for-1 vs. 100% Free

Understanding the "2:1 Match" is vital to your 2026 budget planning.

- Standard Matching Grant: For most homeowners, the state reimburses $2 for every $1 spent. To get the maximum $10,000 grant, you must spend at least $15,000 on qualifying improvements. The state pays $10k; you pay $5k.

- Low-Income Grant: If your household income is at or below 80% of the county median, the state pays 100% of the cost up to $10,000. You pay $0 out of pocket.

3. Approved Improvements in 2026

The 2026 program is laser-focused on "Hardening" (wind mitigation). You cannot use these funds for aesthetic upgrades.

- Opening Protection: Impact-resistant windows, impact-rated exterior doors, and hurricane-rated garage doors.

- Roof Strengthening: Secondary water resistance (SWR), roof-to-wall attachments (straps/clips), and roof deck nailing upgrades.

- The "No-Swap" Rule: If you already have compliant hurricane shutters, the program will not pay for you to switch to impact windows.

4. The Golden Rule: Don't Start Work Early

The most common mistake Florida homeowners make is hiring a contractor before receiving an Award Letter.

- Step 1: Apply for the Free Inspection.

- Step 2: Get your Inspection Report (this tells you what you must fix).

- Step 3: Apply for the Grant in the portal.

- Step 4: Wait for the Grant Award Letter.

If you sign a contract or start work before Step 4, you are disqualified from receiving a single cent of the grant.

Why Working with an Independent Agency is Vital

The MSFH grant isn't just about a free window; it's about a lower insurance bill. At Walker Insurance Agency, we provide the visibility you need to maximize your Return on Investment (ROI).

The Walker Advantage:

- Premium Audit: We analyze your inspection report to show you which improvements (like a Secondary Water Barrier) will trigger the biggest Wind Mitigation Credits on your policy.

- 2026 Market Matching: While the state CFO reports an average savings of $981/year, we shop the 2026 private market to see if your upgrades allow you to move from Citizens to a lower-cost private carrier.

- Compliance Guidance: We ensure you don't lose your grant by accidentally violating the "homestead exemption" or "insured value" requirements.

FAQ

1. Who qualifies as "Low-Income" for the 2026 grant?

You qualify if your household income is 80% or less of your county’s median income. These residents receive first priority and require zero matching funds.

2. Can I use the grant for a new roof?

Yes, but only for the "hardening" components (straps, nails, and water barriers). The grant typically does not cover the cost of the shingles or tiles themselves unless they are part of a specific mitigation package.

3. I had an inspection in 2024. Do I need a new one?

Yes. For the 2026 funding cycle, you must use a new inspection requested through the official mysafeflhome.com portal to ensure it meets current 2026 hardening standards.

4. How long does the reimbursement take?

In 2026, once the final inspection is passed and the "Draw Request" is submitted, funds are typically disbursed within 45 to 60 days.

Don’t Leave Your $10,000 on the Table

The 2026-2027 funding cycle is the largest in Florida history, but the demand is even higher. If you wait until a storm is in the Gulf, the money will be gone.

Start your application today. Contact Walker Insurance Agency to review your current Wind Mitigation credits. We provide the visibility you need to turn a state grant into a lifetime of insurance savings in Stuart.

[GET A FREE QUOTE TODAY]

Call us at +1-407-977-7100 or visit our office in Stuart, FL. Let us help you harden your home for free.

Related Articles

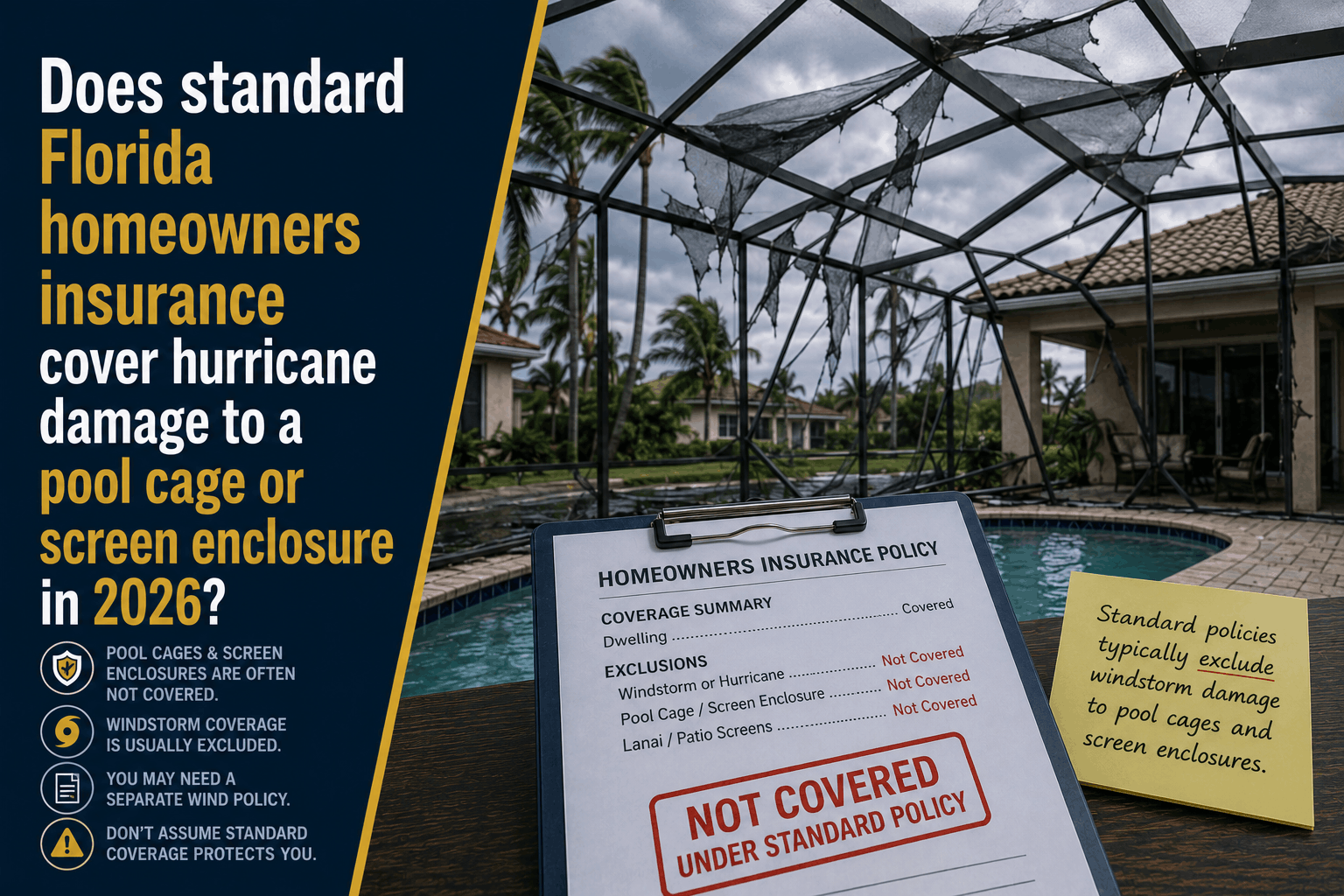

Does Florida Homeowners Insurance Cover a Pool Cage in 2026?

Learn about the "Lanai Loophole" in Florida. Discover why standard homeowners insurance excludes or limits hurricane damage to pool cages and screen enclosures.

Read More →

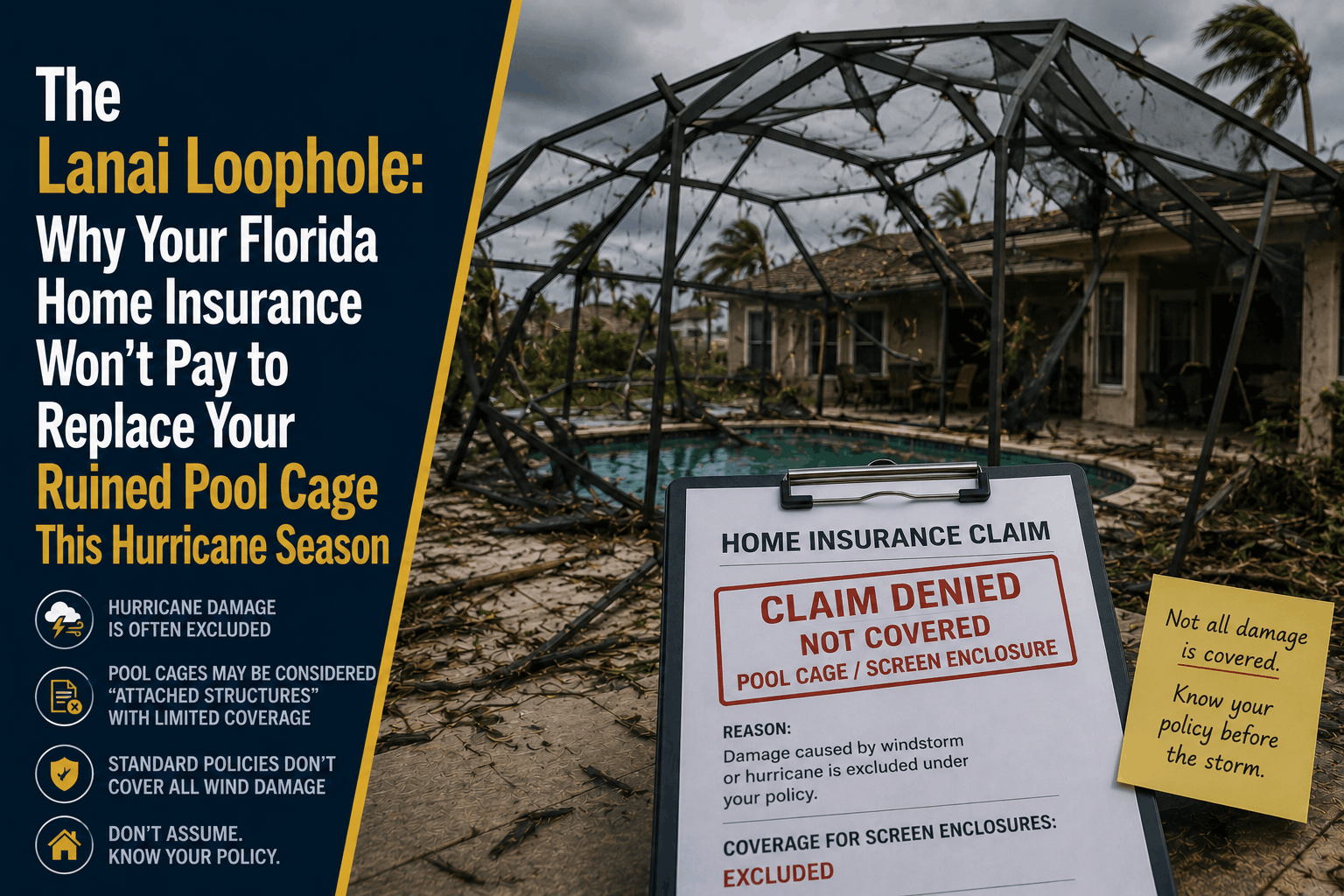

The Lanai Loophole: Why Home Insurance Won't Fix Your Pool Cage

Discover how Florida’s strict "Lanai Loophole" can completely exclude or limit your pool cage and screen enclosure coverage this hurricane season.

Read More →

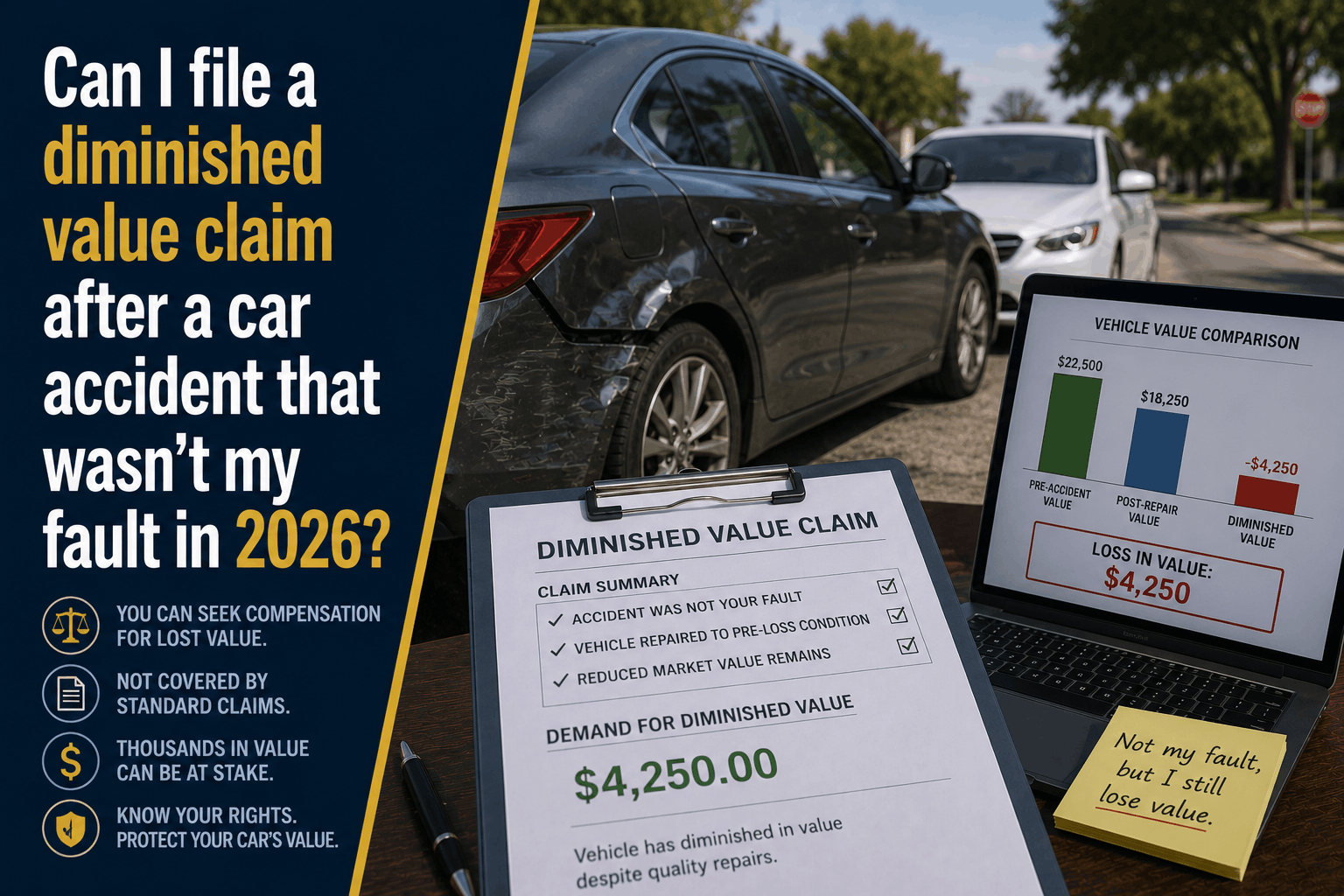

Can I File a Diminished Value Claim in 2026? (Not At-Fault Guide)

If you were involved in a car accident that wasn't your fault, discover how to file a Diminished Value claim to recover your vehicle's lost resale value.

Read More →