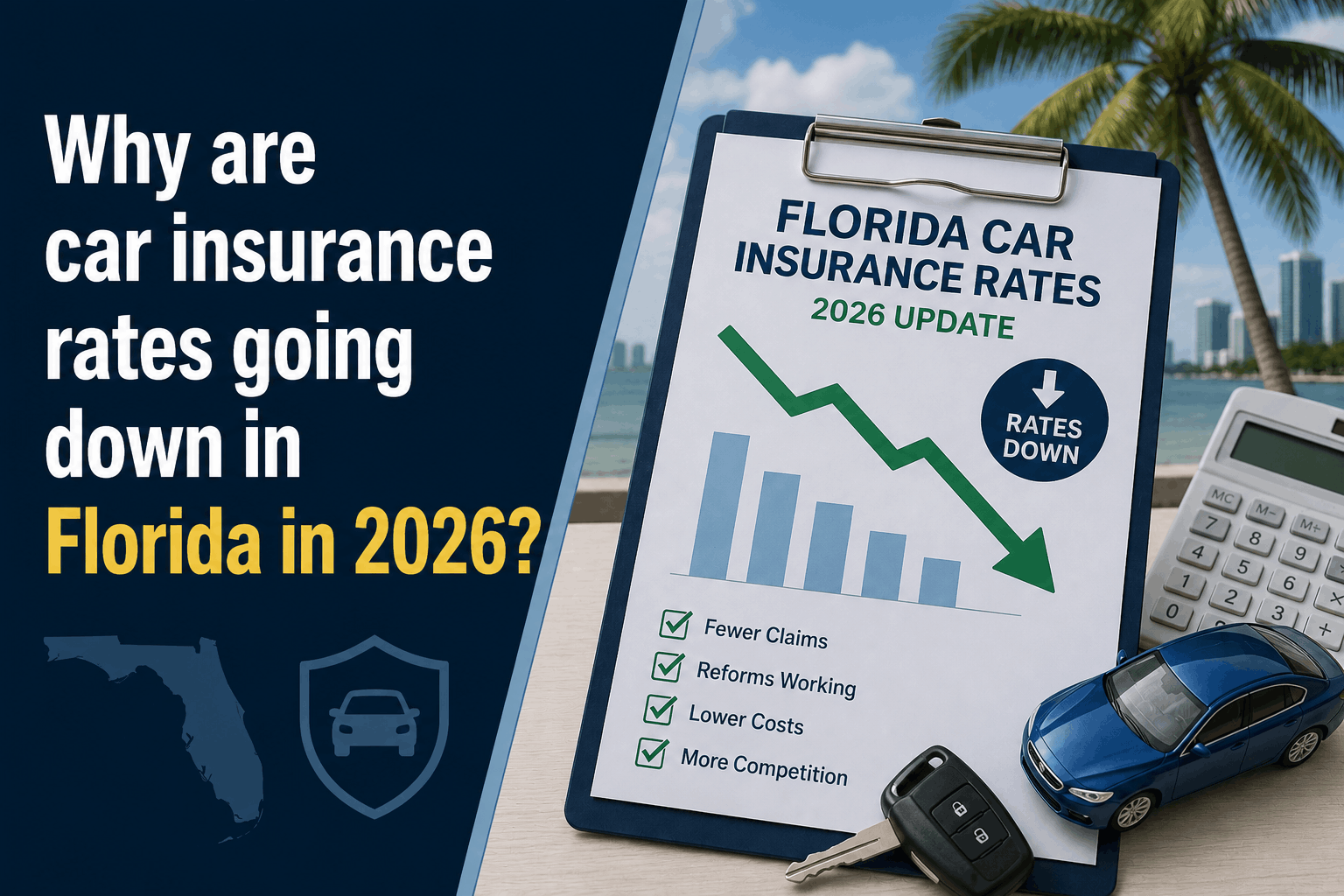

hy Are Florida Car Insurance Rates Going Down in 2026?

Why Are Car Insurance Rates Going Down in Florida in 2026?

The Direct Answer: Car insurance rates are dropping in Florida this year as a direct result of aggressive lawsuit abuse (tort) reforms and stabilized corporate loss ratios. According to data from the Florida Office of Insurance Regulation (OIR), 42 personal auto insurance carriers have filed for rate decreases. The state's five largest auto insurers—which represent nearly 80% of the market—are leading the market lower with an indicated average premium drop of 8%.

Protecting American Consumers Together+ 2

Because historic legislative actions have successfully curbed frivolous legal battles, insurers are spending significantly less money defending claims. They are passing those massive mathematical savings directly back to Florida drivers.

Protecting American Consumers Together

To achieve total visibility over your household expenses, you must understand that the "litigation tax" that plagued Florida for a decade is breaking down, making 2026 the best environment to shop for a lower premium in over fifteen years.

1. The Death of the "Litigation Tax" (HB 837)

For years, Florida drivers paid some of the highest auto insurance premiums in the nation. This wasn't because Floridians were inherently worse drivers, but because the state's legal framework heavily favored billboard lawyers and predatory litigation mills.

The passage of comprehensive tort reform completely changed the playing field by eliminating one-way attorney fees and fixing "bad faith" loopholes.

Florida Insurance Agency

- Fewer Lawsuits: Lawsuit frequency has plummeted across the state, lowering administrative costs for carriers.

State Farm Newsroom - The Loss Ratio Miracle: Florida personal auto insurers recorded a personal auto liability loss ratio of 52.5%—the lowest level documented in the state in 15 years. Across the industry, a lower loss ratio means the market is highly stable, solvent, and primed for price competition.

Florida Office of Insurance Regulation+ 1

2. The May 2026 Carrier Price Drop Blueprint

Because insurance companies are no longer bleeding cash into the legal system, Commissioner Mike Yaworsky and the OIR have pushed carriers to return those savings to policyholders.

Florida Office of Insurance Regulation

| Insurance Carrier | 2026 Approved Rate Action | Total Statewide Consumer Impact |

|---|---|---|

| State Farm | -10.1% Decrease | Over 20% in cuts since 2024; $1B+ in total savings |

| Progressive | -8.0% Decrease | Paired with an additional $1 Billion policyholder refund |

| USAA | -7.0% Decrease | Fully implemented this month; $125M in senior/military relief |

| Allstate | -7.0% Decrease | Rates lowered immediately for 171,000 Florida drivers |

| AAA | -15.0% Total Drop | Achieved across three separate, consecutively approved cuts |

3. Sharp Declines in Vehicle Damage Claims

Beyond legal reforms, the actual physical costs of fixing cars have experienced a remarkable regulatory shift. In 2022, insurers' losses from physical vehicle damage claims sat at an unsustainable 112% (meaning carriers paid out more in repairs than they collected in premiums).

Florida Office of Insurance Regulation+ 1

By early 2026, the OIR confirmed physical damage loss ratios plummeted to 49.5%. Stabilizing supply chains for vehicle parts, combined with stricter anti-fraud parameters regarding glass and body shop billing, have made vehicle repairs far more predictable for underwriters.

Florida Office of Insurance Regulation

4. How to Capture the 2026 "Deflation Dividend"

While the data shows nearly 80% of Florida drivers will see rate relief this year, these drops do not always trigger instantly.

- The Renewal Gap: If you stay on autopilot, your current carrier may wait until your formal six-month policy renewal date to drop your premium.

- The Stacking Strategy: You can maximize this month's rate drops by piling on safe structural policy discounts. Stacking your base carrier rate rollback with an online 6-hour Mature Driver Course (for drivers 55+) or an EFT autopay enrollment can cut your final bill by up to 35% without compromising your core liability limits.

Why Working with an Independent Agency is Vital

When the insurance market shifts from a period of hyper-inflation to sudden deflation, buying insurance online through a generic search portal is a mistake. Portal algorithms are slow to update to fresh monthly rate filings. At Walker Insurance Agency, we provide the data-driven visibility you need to find the lowest premium floor today.

The Walker Advantage:

- Real-Time OIR Tracking: We monitor the OIR filing desk daily. The moment a carrier loads a 7% or 10% rate drop into the state database, we have it active in our quoting software.

- Replacement Cost Calibration: We use up-to-date regional labor data to ensure your comprehensive and collision coverages are perfectly balanced against current 2026 vehicle valuations.

- Cross-Market Portability: If your current carrier isn't passing down the full "Tort Reform Dividend," we will instantly move your profile to a hunger competitor that will.

FAQ

1. Why is my neighbor's auto insurance policy dropping but mine stayed the same? Rate decreases depend entirely on the specific insurance company and the tier of your policy. If your neighbor is with State Farm (-10.1%) or USAA (-7%) and you are with a non-standard carrier that hasn't updated its filings yet, your premium won't change until you shop the market.

2. Do these 2026 auto insurance cuts mean home insurance is dropping too? While auto lines have responded faster to tort reform, the home insurance market is stabilizing simultaneously. The OIR has received more than 185 residential filings requesting rate decreases or flat renewals, showing broad relief across all Florida property lines.

PrimeGroup Insurance

3. What happens to my rate if I have a clean driving record? Drivers with completely clean records stand to gain the most from the 2026 drops. Since you pose zero structural risk, carriers are aggressively under-pricing each other to win your business.

Don't Let Your Insurance Company Pocket Your Reform Savings

The numbers do not lie: Florida's car insurance crisis is officially receding. If your current policy auto-renewed recently without showing a significant drop in price, you are actively overpaying under the state's new rate structures.

Claim your 2026 market price rollback. Contact Walker Insurance Agency for an immediate, data-driven premium audit. We provide the visibility you need to take back your hard-earned cash in Stuart.

[GET A FREE QUOTE TODAY] Call us at +1-407-977-7100 or visit our office in Stuart, FL. Let us find your savings today.

Related Articles

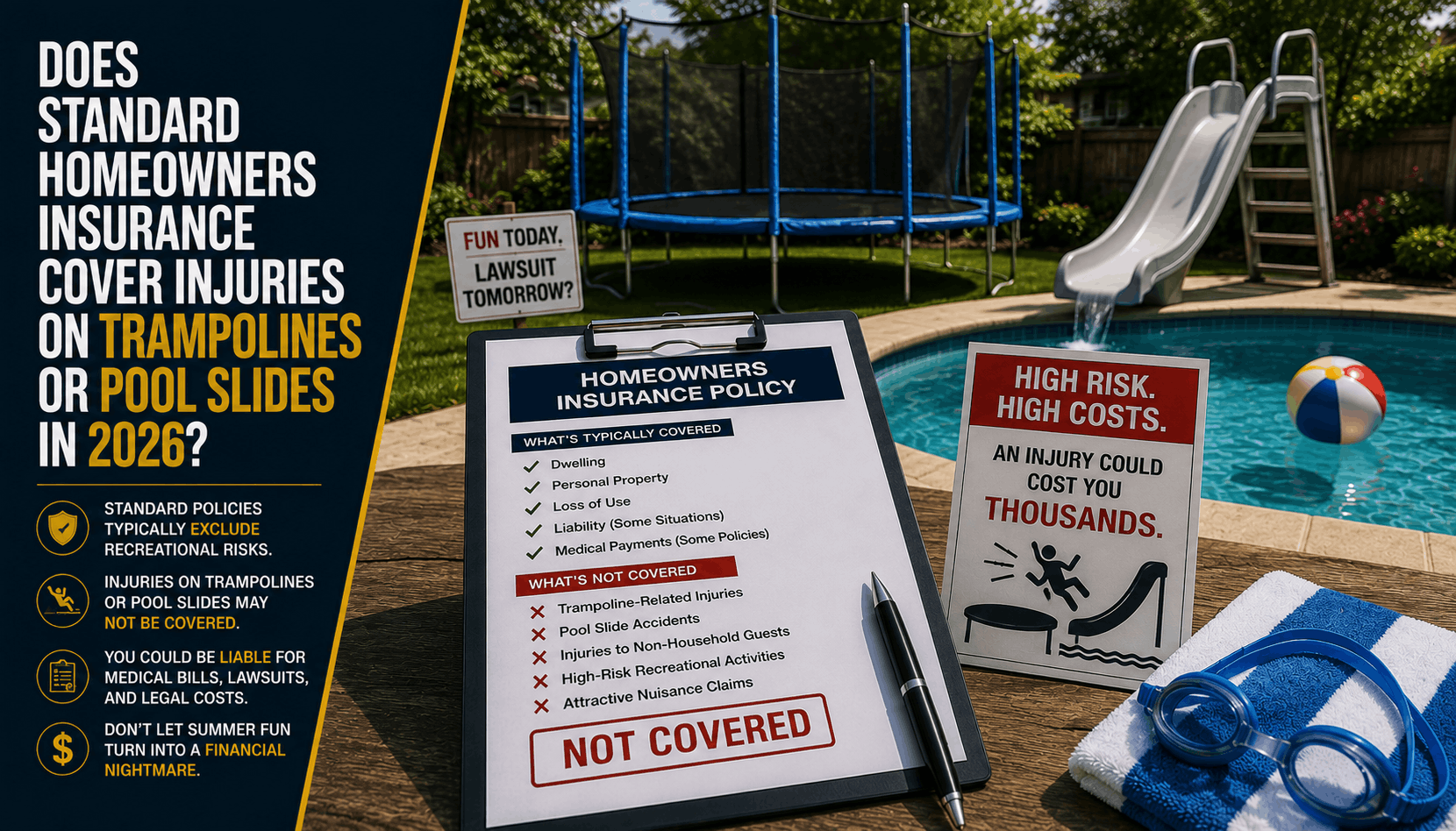

Does Homeowners Insurance Cover Trampolines or Pool Slides? (2026)

Planning summer fun in Stuart, FL? Discover why trampolines and pool slides are major homeowners insurance liability traps that can lead to dropped coverage.

Read More →

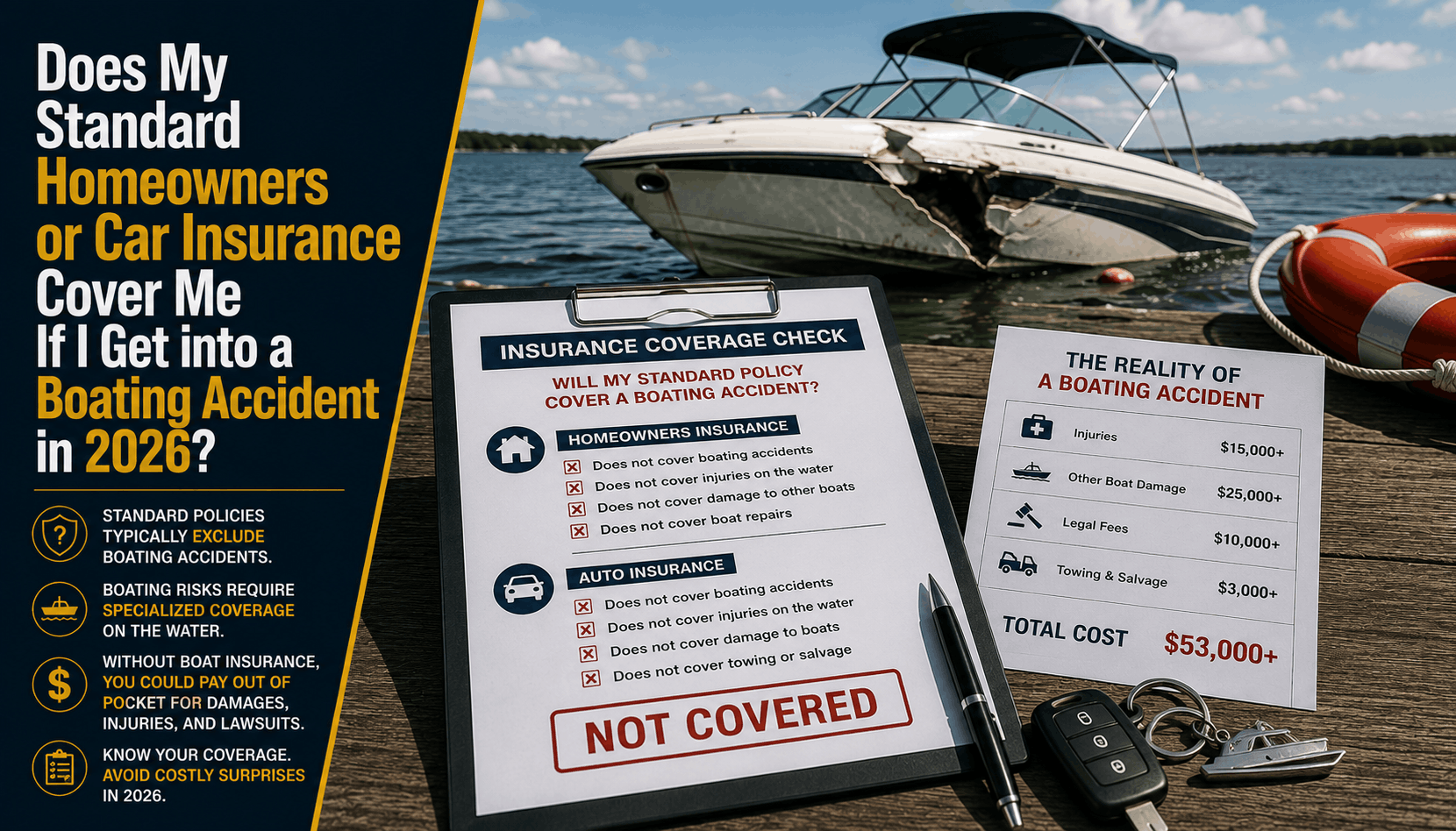

Does Home or Auto Insurance Cover Boating Accidents? (2026)

Planning a boat day in Stuart? Learn why relying on your home or auto insurance policies for watercraft liability is a dangerous financial gap.

Read More →

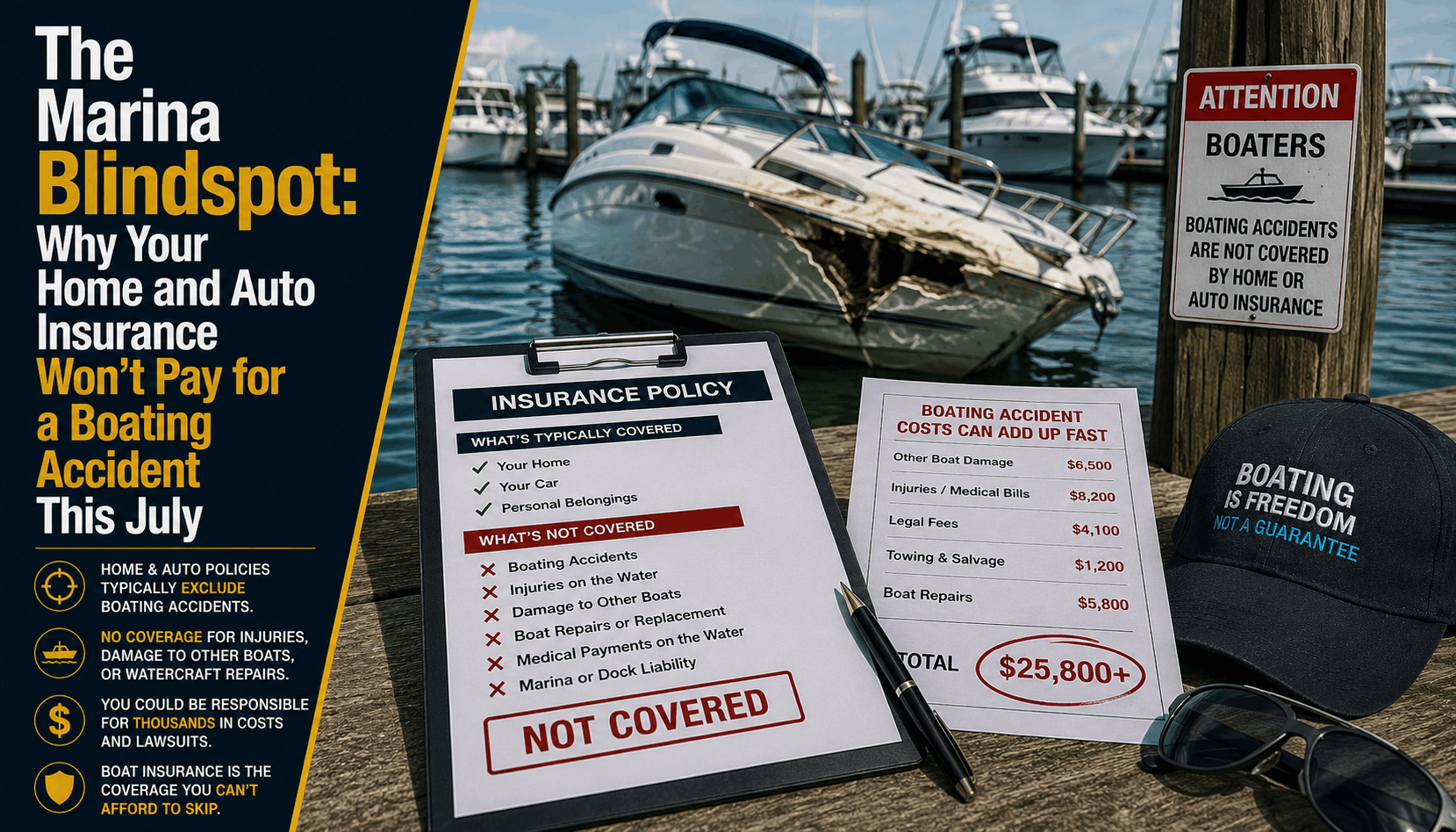

Why Home and Auto Insurance Won't Cover Boat Accidents (2026)

Planning a July boat day in Stuart, FL? Discover why relying on your home or auto insurance policies for watercraft liability is a dangerous financial blindspot.

Read More →