How Much Does a $1 Million Umbrella Policy Cost in Florida? (2026)

How Much Does a $1 Million Umbrella Policy Cost in Florida?

The Direct Answer: In 2026, the average cost of a $1 million umbrella policy in Florida ranges between $425 and $950 per year. While these policies used to be under $300, increased litigation costs and "nuclear verdicts" in Florida have pushed premiums upward. For most standard households (two cars, one home, no teen drivers), the median cost is approximately $585 annually (about $49 per month).

The price fluctuates significantly based on your "risk exposures." For instance, adding a swimming pool, a rental property, or a high-speed boat can push your premium toward the $850 - $1,100 range. To achieve total financial visibility, you must understand that the first million of coverage is the most expensive; each additional million after that usually costs only $100 to $200 more.

2026 Estimated Cost Breakdown in Florida

Umbrella insurance offers the highest level of protection per dollar spent. Here is what you can expect to pay for different levels of coverage:

| Coverage Limit | Annual Cost Range (FL) | Estimated Monthly Cost |

|---|---|---|

| $1 Million | $425 – $950 | $35 – $79 |

| $2 Million | $550 – $1,100 | $46 – $92 |

| $5 Million | $1,200 – $2,500 | $100 – $208 |

Key Factors That Increase Your Florida Premium

In 2026, Florida insurers are more selective than ever. Your costs will rise if you have:

- Teenage Drivers: Adding a driver under 25 is the single biggest factor that can double an umbrella premium.

- Additional Properties: Each rental unit or vacation home increases the statistical likelihood of a liability claim.

- Watercraft & Toys: High-powered boats, Jet Skis, and ATVs carry higher injury risks and require higher premiums.

- Driving Record: Speeding tickets or at-fault accidents in the last 3–5 years will impact both your eligibility and your price.

Underlying Requirements: The "Floor" You Need

You cannot buy an umbrella policy without first having high "base" limits. If you lower your auto or home limits below these requirements, your umbrella policy may not trigger, leaving you with a massive out-of-pocket gap.

Standard 2026 requirements for Florida:

- Auto (Bodily Injury): $250,000 per person / $500,000 per accident.

- Auto (Property Damage): $100,000.

- Homeowners (Liability): $300,000.

How to Lower Your Umbrella Costs

Even in Florida’s 2026 market, there are ways to find a better deal:

- Bundle Everything: Purchasing your umbrella with your auto and home carrier can result in a 10% to 15% discount.

- Safety & Security: Monitored alarms and water-leak detection systems sometimes trigger small secondary credits.

- Maintain a Clean Record: In 2026, many carriers offer "Safe Driver" discounts that extend to the umbrella layer.

Why Working with an Independent Agency is the Best Strategy

At Walker Insurance Agency, we know the Florida umbrella market inside and out. Some carriers in 2026 refuse to cover homes with pools or specific dog breeds—we know who is "risk-friendly" and who isn't.

The Walker Advantage:

- Standalone Options: If your current carrier won't write an umbrella, we have access to independent markets that can sit on top of your existing policies.

- Exposure Audit: We look for "invisible" risks, like serving on a board or your social media presence, to ensure your policy covers defamation and libel.

- Maximized Visibility: We show you the math on how increasing your underlying auto limits might actually lower your umbrella cost by moving you into a better risk tier.

FAQ

1. Why is umbrella insurance more expensive in Florida?

Florida is a "litigation-heavy" state. High settlement awards and laws that make vehicle owners strictly liable for accidents (Dangerous Instrumentality Doctrine) make insurance risks higher here than in other states.

2. Does a $1M umbrella cover damage to my own house?

No. Umbrella insurance is strictly third-party liability coverage. It pays for damage you cause to others. Your own home and car are covered by your property and collision policies.

3. Is $1 million enough coverage for 2026?

It is a great starting point, but if your net worth (including home equity and retirement) is over $1 million, or if you have a high future earning potential, you should consider $2M or $5M limits to fully shield your assets.

4. Can I get an umbrella policy if I have a DUI?

In 2026, it is extremely difficult to find an umbrella carrier for drivers with a DUI in the last 5–7 years. You may need to look at "Excess & Surplus" (E&S) lines, which carry much higher premiums.

Local Business Schema

Protect Your Life’s Work Today

In Florida, one legal judgment can wipe out your entire financial portfolio. Paying less than $2 a day for $1 million in protection is the smartest financial move you can make in 2026.

Get your protection audit today. Contact Walker Insurance Agency for a complimentary market comparison. We provide the visibility you need to ensure your wealth is shielded at the best possible price in Stuart.

[GET A FREE QUOTE TODAY]

Call us at +1-407-977-7100 or visit our office in Stuart, FL. Let us help you safeguard your legacy.

Related Articles

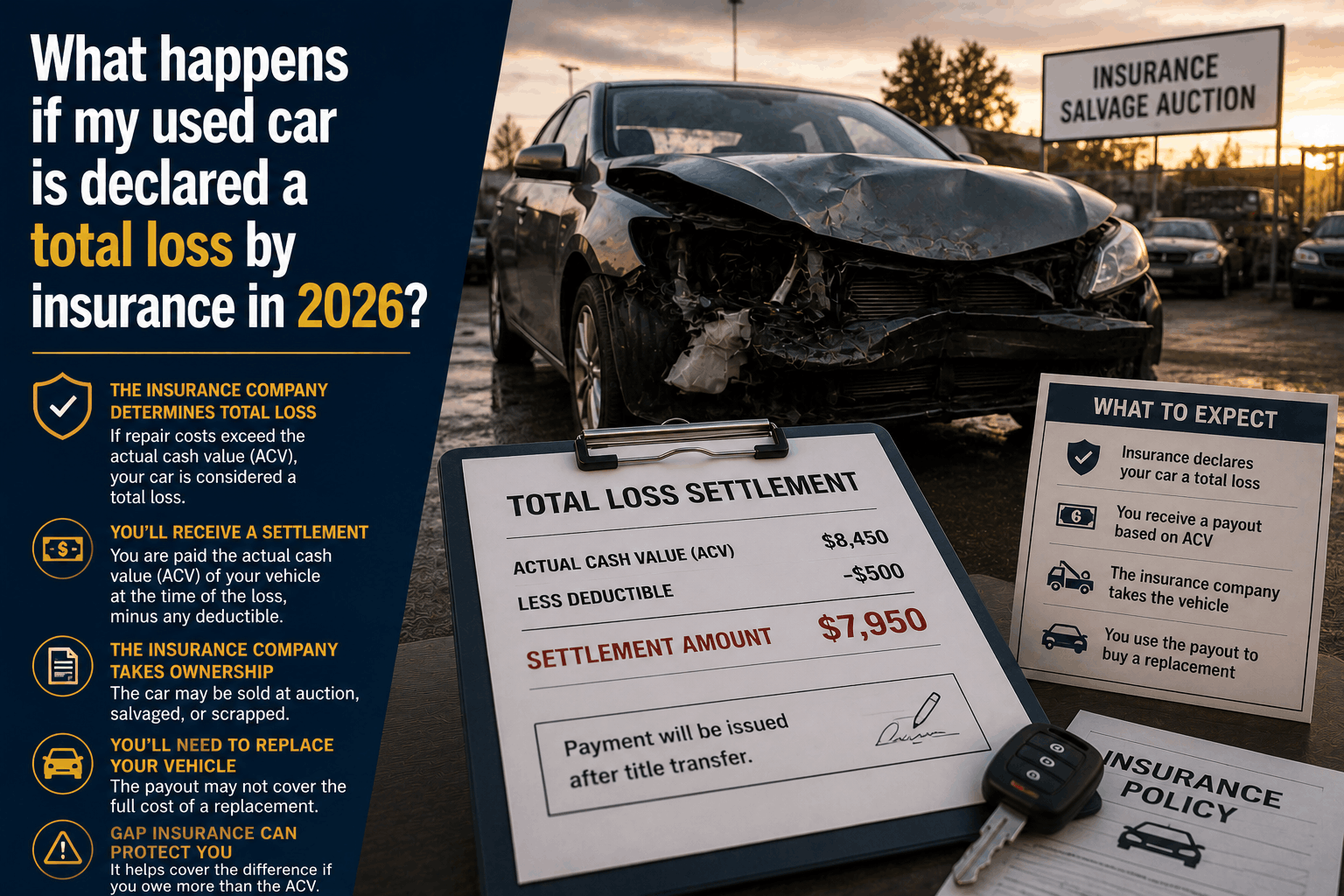

What Happens If Your Used Car Is Totaled by Insurance in 2026?

Navigating a totaled used car claim? Discover the step-by-step insurance process, how Actual Cash Value (ACV) is calculated, and how to dispute a low valuation.

Read More →

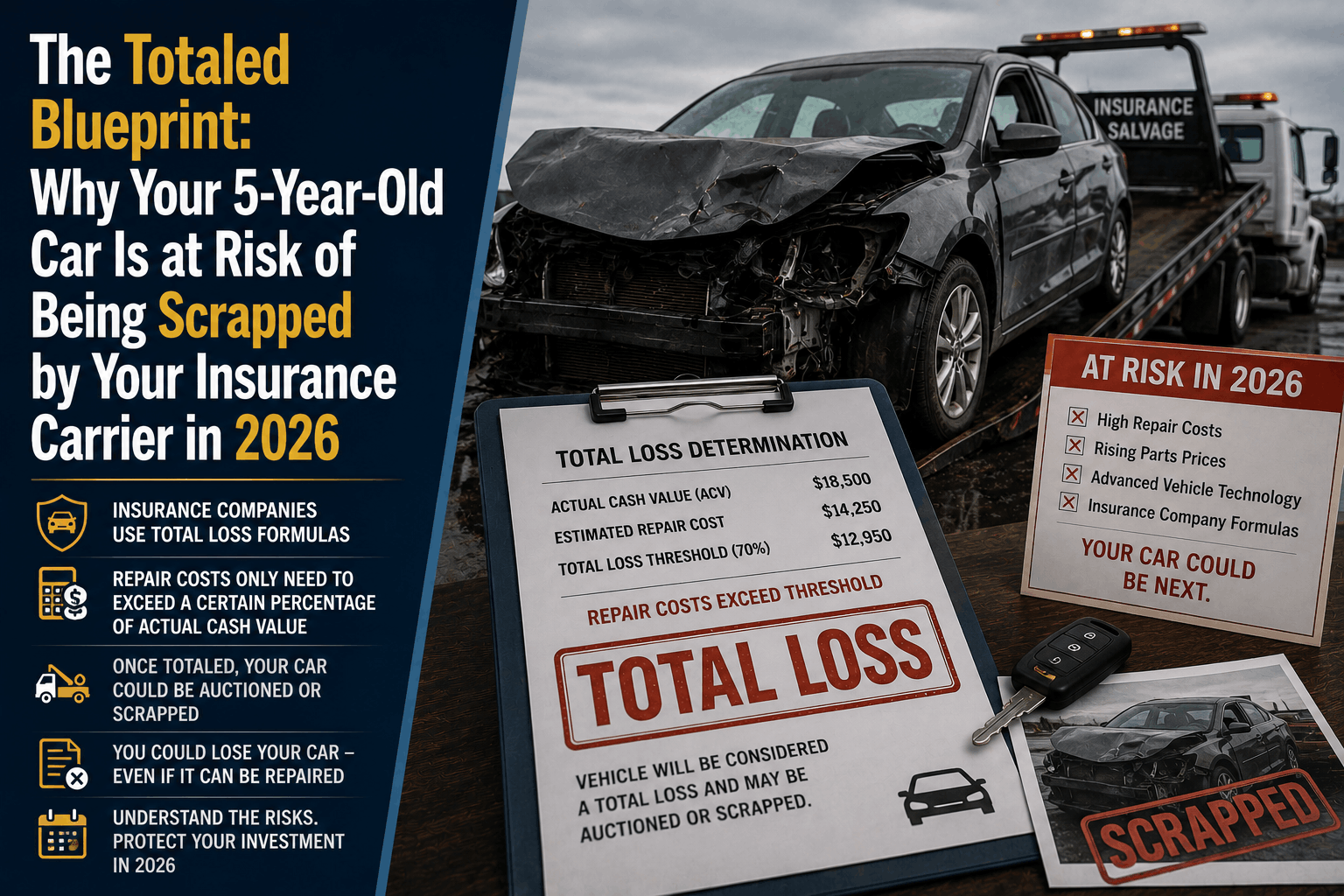

The Totaled Blueprint: Why Insurers Are Scrapping 5-Year-Old Cars in 2026

Discover why insurance companies are declaring 5-year-old cars a total loss in 2026\. Learn how ADAS technology and high salvage values trigger the "Totaled Blueprint."

Read More →

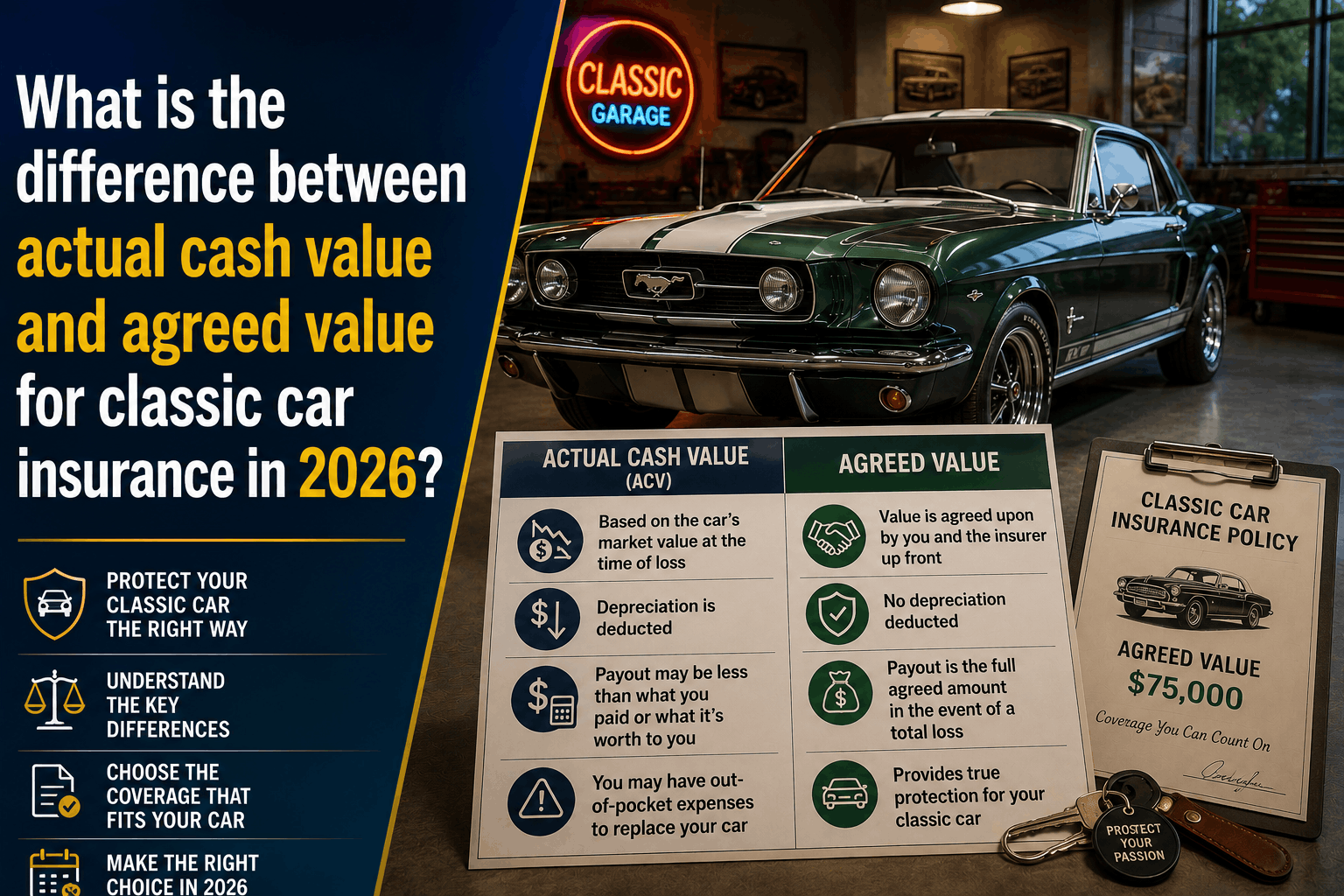

ACV vs. Agreed Value: Classic Car Insurance Guide (2026)

What is the difference between Actual Cash Value and Agreed Value for classic cars? Discover why 2026 market trends make traditional policies highly risky.

Read More →