Hidden Costs of Low-Liability Insurance Florida | Asset Protection

The Hidden Costs of Low-Liability Insurance: Protecting Your Assets

In the state of Florida, many drivers focus solely on the "cheapest price" to stay legal on the road. However, there is a massive difference between being "legal" and being "protected." While Florida law currently requires only $10,000 in Personal Injury Protection (PIP) and $10,000 in Property Damage Liability (PDL), these minimums are among the lowest in the nation. In 2026, with the rising costs of medical care and vehicle technology, relying on these limits is no longer a budget-friendly choice—it is a significant financial gamble.

For homeowners and business owners in Stuart, an accident that exceeds your policy limits doesn't just end with an insurance claim; it can end in a courtroom. To achieve true financial visibility, you must understand how low-liability insurance can expose your personal assets to seizure and litigation.

The Problem: When "Minimum" Becomes a Liability

The primary problem with low-liability insurance is that it creates a false sense of security. If you are at fault in a serious accident and your insurance only pays $10,000 toward a $50,000 repair bill for a luxury SUV, you are personally responsible for the $40,000 gap.

The financial reality of a "gap":

In Florida, if your insurance limits are exhausted, the injured party’s legal team can pursue your personal assets to satisfy a judgment. This includes:

- Your Savings and Investments: Cash accounts are often the first target.

- Your Home Equity: While Florida has strong homestead protections, legal entanglements can complicate your property's title and future.

- Future Wages: In some cases, your future earnings can be garnished to pay off an accident debt.

H2: Factores that Make Low Limits More Dangerous in 2026

The Florida landscape has changed, and so has the cost of accidents. Several factors have made the $10,000 minimum limit obsolete for the modern driver:

- Vehicle Technology: Even a minor fender bender in a modern electric vehicle or a car equipped with advanced sensors (ADAS) can easily exceed $10,000 in repair costs.

- Rising Medical Inflation: Emergency room visits and specialized surgeries in 2026 frequently surpass the basic PIP and liability caps within hours of an incident.

- Litigation Trends: Florida has a high rate of insurance litigation. If you lack adequate Bodily Injury (BI) coverage, you become an easy target for lawsuits seeking compensation for "pain and suffering."

Comparing Minimum vs. Recommended Liability Limits

To protect your assets, you must move beyond the "10/10" mindset. Below is a comparison of how different levels of coverage protect your net worth:

| Coverage Type | Florida State Minimum | Recommended (Middle Class) | Asset Protection Level |

|---|---|---|---|

| Property Damage | $10,000 | $50,000 - $100,000 | High |

| Bodily Injury | $0 (Optional) | $100,000 / $300,000 | Essential |

| Personal Assets Risk | Extremely High | Low | Minimal |

When Should You Choose Higher Limits?

Choosing the right liability limit depends on your "exposure." You should significantly increase your coverage if:

- You Own a Home: Your home is your biggest investment; don't let a car accident put it at risk.

- You Have a High Net Worth: If you have more than $50,000 in liquid assets, you are a "target" for litigation.

- You Commute in High-Traffic Areas: If you drive on Florida's major highways (like I-95 or US-1), your statistical risk of a multi-vehicle accident is much higher.

- You Have Teen Drivers: Inexperienced drivers are more likely to be involved in high-impact collisions.

Why Working with an Independent Agency is Vital for Asset Protection

At Walker Insurance Agency, we don't just sell policies; we act as risk managers for your lifestyle. A generic online quote won't ask about your home equity or your retirement accounts, but we do.

The Walker Advantage:

- Custom Limit Scaling: We match your insurance limits to your actual net worth to ensure you are never "underinsured."

- Umbrella Policy Integration: For those with significant assets, we can provide Umbrella insurance that adds $1 million or more in extra protection.

- Florida-Specific Guidance: We understand the unique 2026 Florida statutes regarding "No-Fault" and how they intersect with your liability.

- True Visibility: We show you the "worst-case scenario" math so you can make a choice based on facts, not just a monthly premium.

FAQ

1. Is Bodily Injury (BI) insurance mandatory in Florida in 2026?

While it is not technically required for all drivers to register a car, it is effectively mandatory for anyone with assets to protect. Furthermore, if you’ve had a DUI or a serious accident, the state may legally require you to carry BI under the Financial Responsibility Law.

2. How much does it cost to increase my liability from $10k to $50k?

Surprisingly little. Often, doubling or tripling your liability limits adds only a few dollars to your monthly premium, providing a massive increase in financial safety.

3. What is an Umbrella Policy, and do I need one?

An Umbrella policy provides extra liability coverage above your auto and home insurance. If you own a home and have significant savings, an Umbrella policy is the ultimate tool for asset protection.

4. Can I be sued if I have the state-required insurance?

Yes. Having the legal minimum insurance does not prevent you from being sued for damages that exceed those limits.

Local Business Schema

Don’t Bet Your Home on a Cheap Policy

A low premium might save you $20 a month, but it could cost you your entire life savings in a single second. In Florida, you need more than just a piece of paper that says you are "legal"—you need a shield that protects everything you've worked for.

Secure your legacy today. Contact Walker Insurance Agency for a comprehensive asset protection audit. We will help you see through the "cheap insurance" myths and provide the visibility you need to ensure you're truly covered.

[GET A FREE QUOTE TODAY]

Call us at +1-407-977-7100 or visit our office in Stuart, FL. Let us build a wall of protection around your assets.

Related Articles

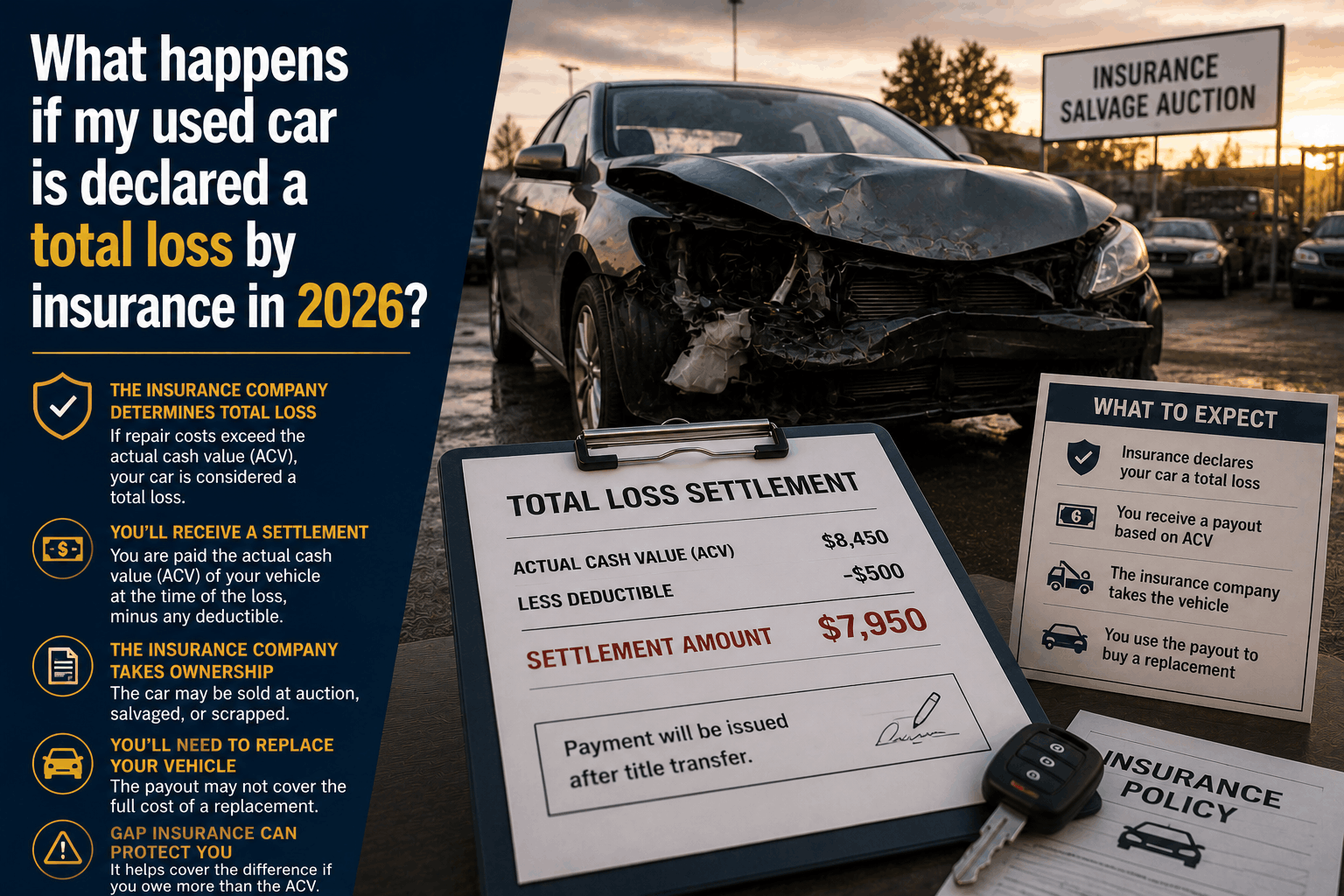

What Happens If Your Used Car Is Totaled by Insurance in 2026?

Navigating a totaled used car claim? Discover the step-by-step insurance process, how Actual Cash Value (ACV) is calculated, and how to dispute a low valuation.

Read More →

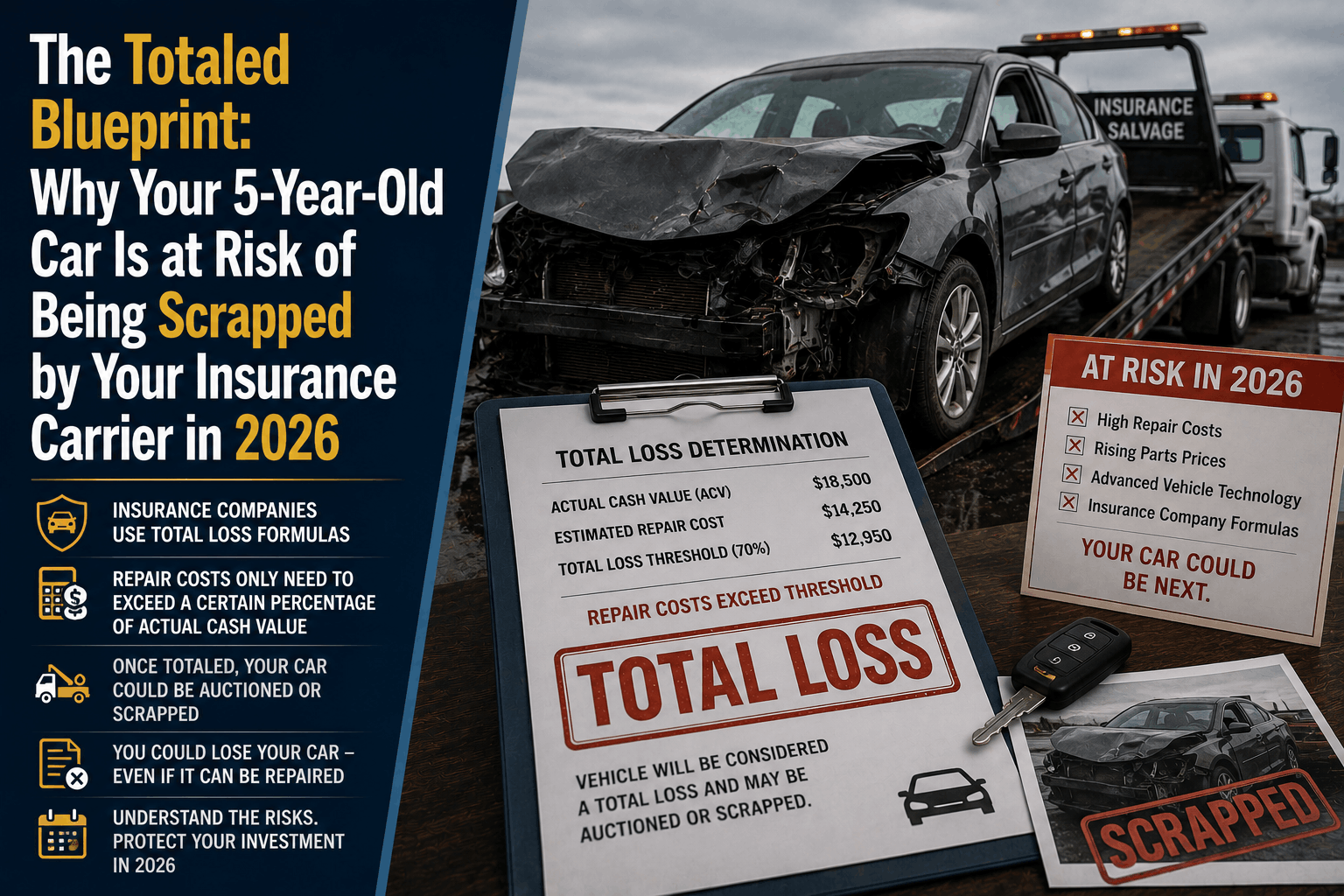

The Totaled Blueprint: Why Insurers Are Scrapping 5-Year-Old Cars in 2026

Discover why insurance companies are declaring 5-year-old cars a total loss in 2026\. Learn how ADAS technology and high salvage values trigger the "Totaled Blueprint."

Read More →

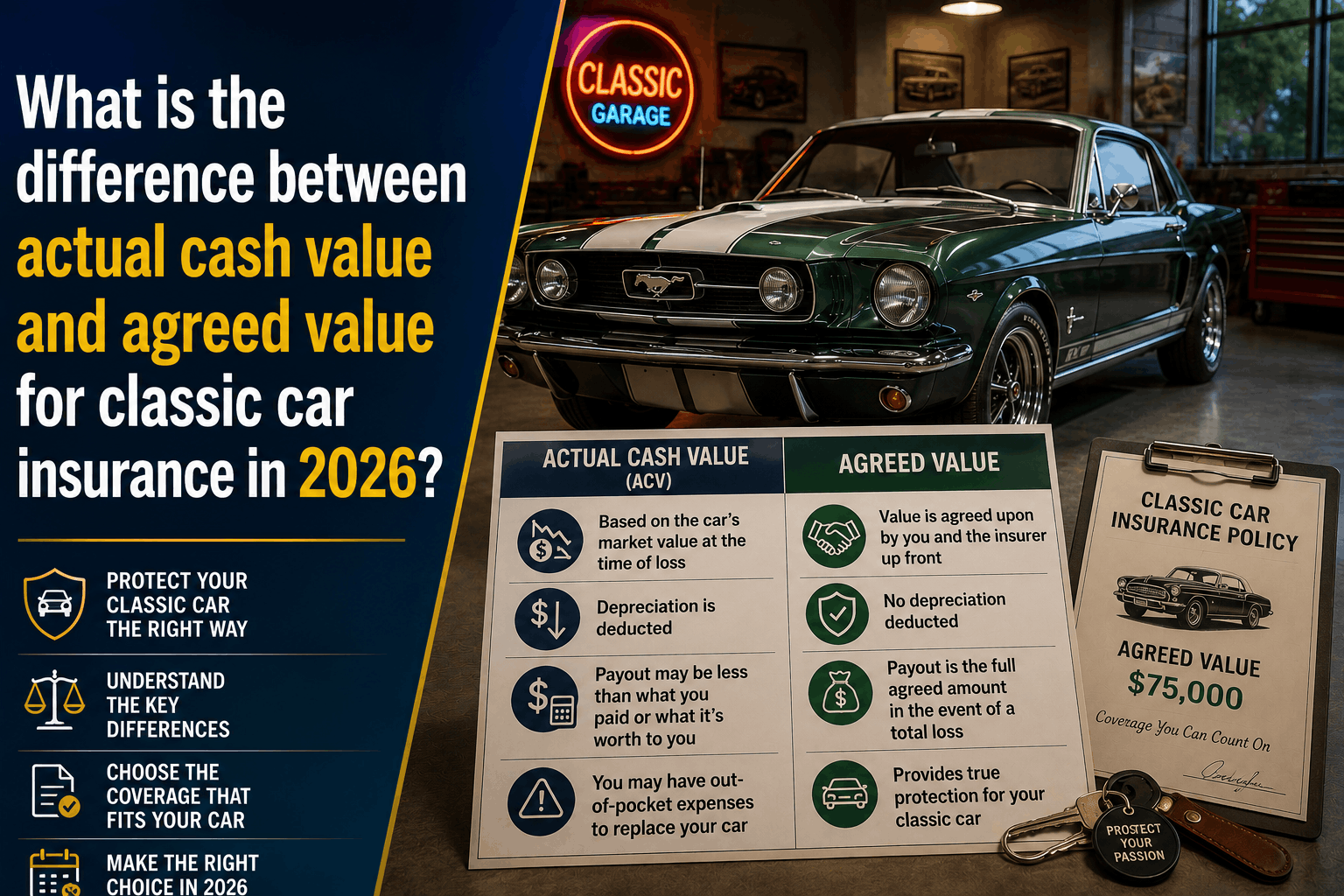

ACV vs. Agreed Value: Classic Car Insurance Guide (2026)

What is the difference between Actual Cash Value and Agreed Value for classic cars? Discover why 2026 market trends make traditional policies highly risky.

Read More →