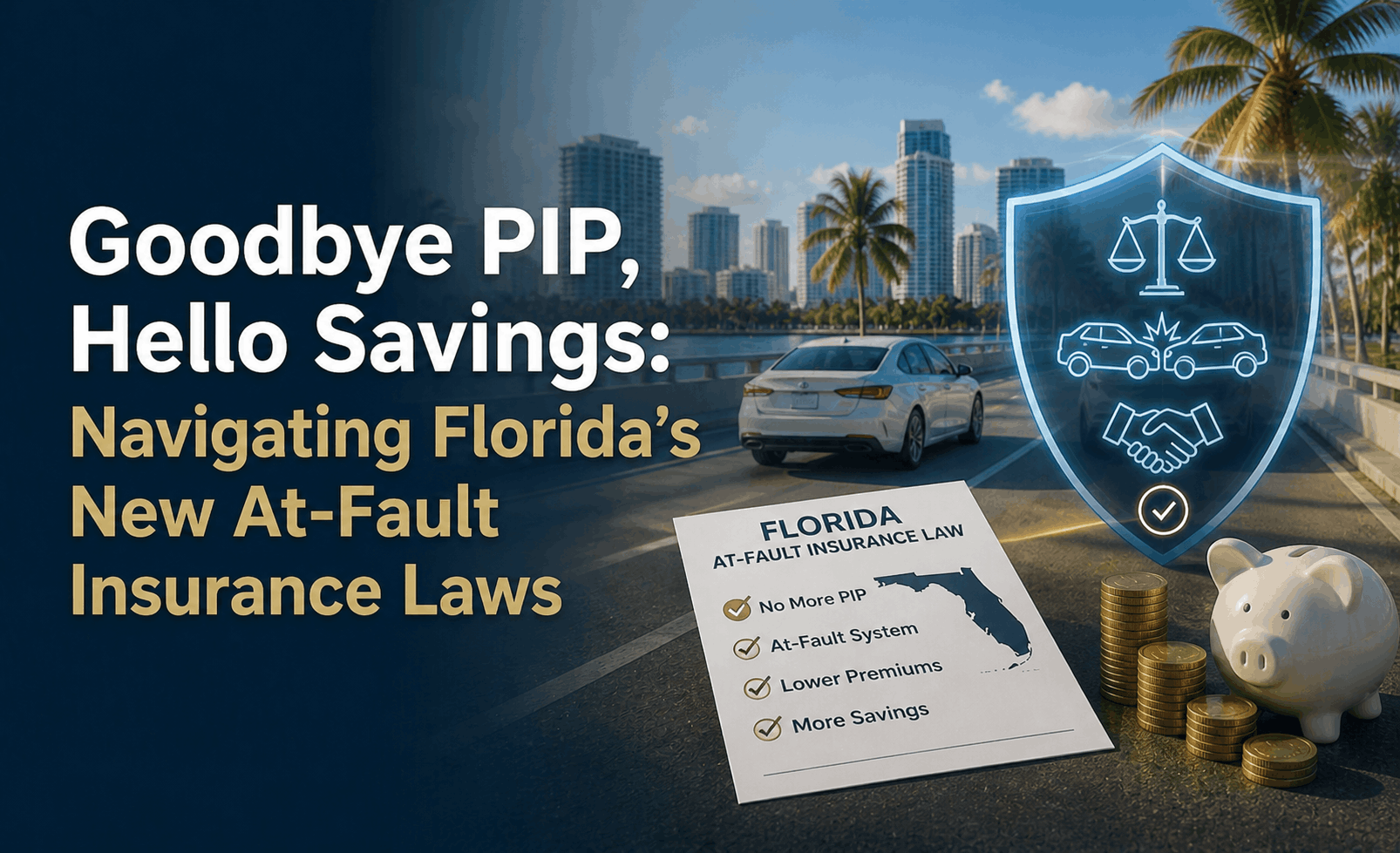

Florida’s New At-Fault Auto Insurance Laws 2026: Goodbye PIP

Goodbye PIP, Hello Savings: Navigating Florida’s New At-Fault Insurance Laws

The Direct Answer: As of July 1, 2026, Florida has officially repealed its No-Fault insurance system. Personal Injury Protection (PIP) is no longer required or available. It has been replaced by a mandatory at-fault (tort) system, requiring all drivers to carry Bodily Injury Liability (BIL) limits of at least $25,000 per person and $50,000 per accident, alongside $10,000 in Property Damage. While coverage mandates have increased, 2026 market reforms are already driving average premium savings of $300–$500 annually for many Florida households.

To achieve total visibility in this new era, you must understand that your financial protection now depends on your ability to prove the other driver was negligent. In 2026, Florida is no longer about "who pays first," but about "who is at fault."

1. The Core Shift: 25/50/10 is the New Standard

The transition from No-Fault to At-Fault means you are now legally responsible for the medical bills of anyone you injure in a crash. To register a vehicle in Florida after July 1, 2026, you must meet the 25/50/10 requirement:

- $25,000 Bodily Injury Liability per person.

- $50,000 Bodily Injury Liability per accident.

- $10,000 Property Damage Liability.

The MedPay Alternative: Since PIP no longer exists to pay your own initial medical bills, insurers now offer Medical Payments (MedPay). While optional, it is highly recommended to cover immediate hospital costs regardless of who is determined to be at fault.

2. The "51% Rule": Florida’s New Comparative Negligence

A critical part of the 2026 landscape is the Modified Comparative Negligence standard. This rule drastically changes your right to collect damages:

The 51% Bar: If you are found to be more than 50% responsible for an accident, you are legally prohibited from recovering any money from the other driver.

In the old PIP system, you could collect benefits even if you were 100% at fault. In 2026, if you are the majority contributor to the crash, you receive zero compensation from the other party.

3. Why Rates are Dropping in 2026

Counter-intuitively, adding mandatory Bodily Injury hasn't caused a massive price spike. Instead, Florida's 2026 insurance market is stabilizing due to:

- Tort Reform Dividend: 2023 legislative changes have finally reduced the "litigation tax" that plagued Florida for decades.

- End of PIP Fraud: The elimination of PIP has removed the primary target for organized insurance fraud rings.

- Carrier Re-Entry: More than 10 new national carriers have re-entered the Florida market in the last 12 months, creating fierce price competition.

4. Uninsured Motorist (UM): More Important Than Ever

Despite the new mandates, Florida still has one of the highest rates of uninsured drivers in the U.S. in 2026.

- Your Only Protection: If an uninsured driver hits you, your Bodily Injury coverage won't help you—it only helps the people you hit.

- The Recommendation: We strongly advise matching your Uninsured Motorist (UM) coverage to your new 25/50/10 (or higher) liability limits.

Why Working with an Independent Agency is Vital

In an at-fault system, a "cheap" policy can lead to an expensive lawsuit. At Walker Insurance Agency, we provide the visibility you need to protect your assets under the new tort laws.

The Walker Advantage:

- 2026 Transition Audit: We verify that your policy automatically shifted from PIP to the new BIL mandates without any "coverage gaps."

- Asset Shielding: We help you determine if the new $25,000 minimum is enough to protect your home and savings from 2026 legal judgments.

- Multi-Carrier Shopping: We compare the new 2026 entrants to ensure you are getting the "Reform Discount" you deserve.

FAQ

1. Is PIP completely gone in Florida as of 2026? Yes. As of July 1, 2026, PIP is no longer a part of the Florida insurance landscape. All new and renewal policies must follow the Bodily Injury (At-Fault) model.

2. Will my car registration be suspended if I don't update my policy? Yes. The Florida DHSMV will automatically flag policies that don't meet the new 25/50/10 BIL requirements. You must show proof of the new limits to maintain valid registration.

3. What is the difference between PIP and MedPay? PIP was a mandatory $10,000 "No-Fault" benefit. MedPay is an optional 2026 benefit that pays your medical bills quickly, but it does not include the wage loss or death benefits PIP once provided.

4. Can I still sue for pain and suffering in 2026? Yes. With the repeal of PIP, the "permanent injury threshold" has been removed. You can now pursue the at-fault driver for non-economic damages, provided you are 50% or less at fault.

Local Business Schema

Don't Get Stuck in the No-Fault Past

Florida's insurance laws have seen their biggest change in 50 years. Navigating the shift from "No-Fault" to "At-Fault" requires an expert who understands the 2026 mandates.

Audit your liability today. Contact Walker Insurance Agency for a 2026 Compliance Review. We provide the visibility you need to ensure you’re legally covered and saving money in the new Florida market.

[GET A FREE QUOTE TODAY] Call us at +1-407-977-7100 or visit our office in Stuart, FL. Let us help you navigate the new road ahead.

Related Articles

Does Florida Home Insurance Cover Roof Replacement Cost in 2026?

Think your Florida home insurance covers 100% of a new roof after wind damage? Learn how new 2026 guidelines leave Stuart homeowners paying out of pocket.

Read More →

The Florida Roof Depreciation Trap: Why RCV Policies Fail in 2026

Think your Florida home insurance covers 100% of a new roof after a hurricane? Discover the "Roof Surface Payment Schedule" trap leaving Stuart homeowners exposed.

Read More →

The Frame-Only Trick: Why Pool Enclosure Insurance Fails in 2026

Think your Florida screen enclosure rider covers everything? Discover "The Frame-Only Trick" that leaves homeowners paying 100% out of pocket for torn mesh this hurricane season.

Read More →