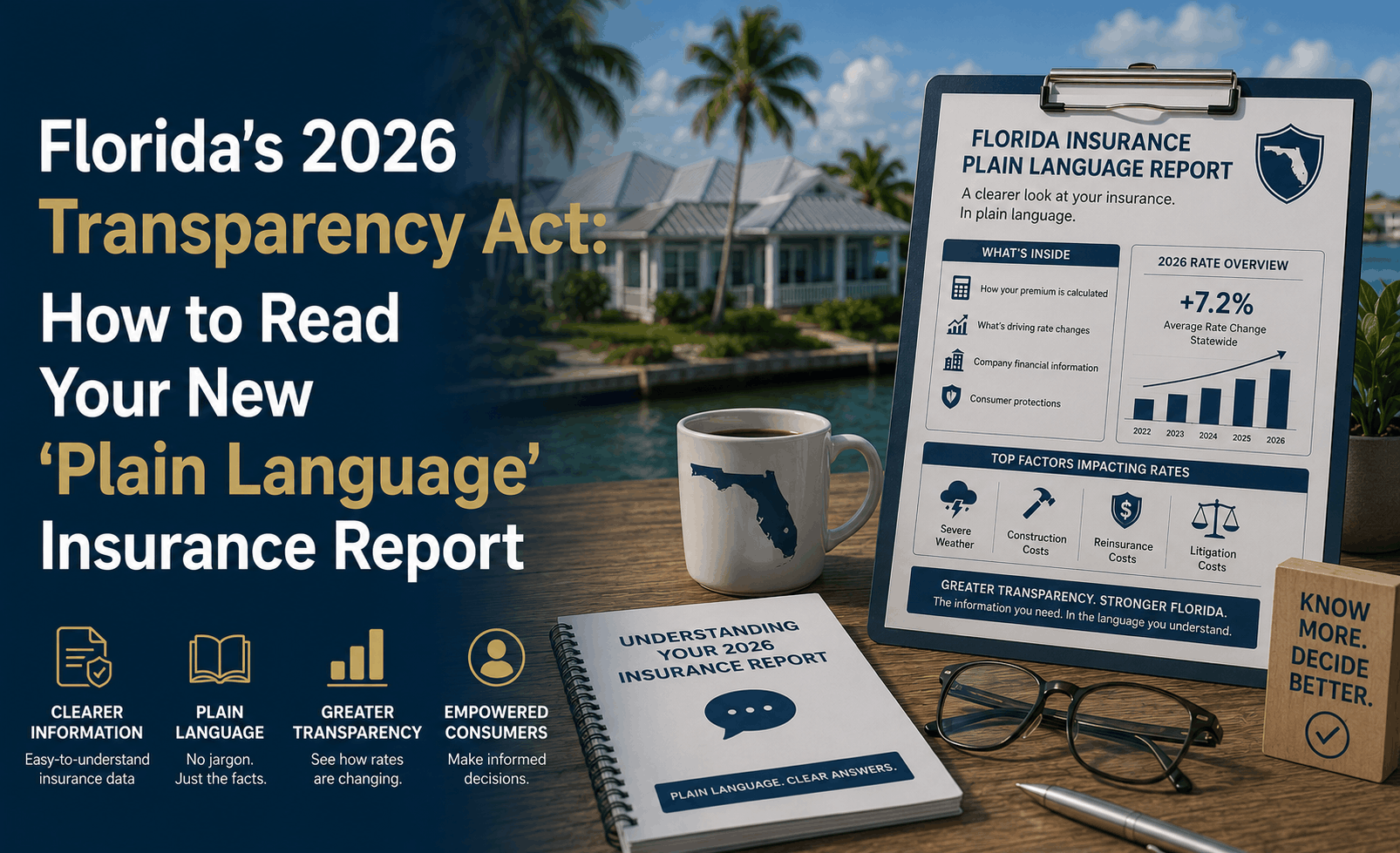

Florida’s 2026 Transparency Act: How to Read Your 'Plain Language' Report

Florida’s 2026 Transparency Act: How to Read Your New 'Plain Language' Insurance Report

The Direct Answer: Effective October 1, 2026, Florida law requires all residential property insurers to provide a "Plain Language" Rate Transparency Report with every new offer and policy renewal. Under the 2026 Transparency Act (HB 767/SB 832), insurance companies can no longer hide behind complex "trade secret" algorithms. Your renewal must now include a graphic breakdown showing exactly what percentage of your premium goes toward reinsurance, claims, agent commissions, and company profit. If the Florida Office of Insurance Regulation (OIR) finds the report misleading or too technical, they are legally mandated to reject the insurer’s rate filing.

To achieve total visibility over your 2026 renewal, you must know how to decode this new report to ensure you aren't paying for "hidden" costs or land value that shouldn't be insured.

1. What is the "Plain Language" Mandate?

For decades, Florida insurance bills were intentionally vague. In 2026, the state has "broken the barrier" of technical jargon.

- Concise Definitions: The OIR now provides standardized, simple definitions for terms like "Reinsurance" and "Loss Adjustment Expense" that must be used in the report.

- Graphic Breakdown: Every report must include a pie chart or bar graph totaling 100% of your rate factor.

- No "Land Value" Inclusion: In a major win for homeowners, the 2026 Act prohibits insurers from including the value of the land when calculating your Coverage A. This prevents "premium bloating" on high-value Florida lots.

2. Key Sections of Your 2026 Transparency Report

When you open your 2026 renewal, look for these three critical transparency pillars:

- The Cost Factor Breakdown: This chart reveals if your rate increase is due to global reinsurance costs (which have stabilized in 2026) or the insurer’s own internal profits and administrative expenses.

- Adverse Findings Disclosure: Insurers must now disclose any major adverse findings by the OIR from the previous three years. If your company has been flagged for poor claims handling, it will be right there in plain English.

- Affiliate Transactions: The report must state if the insurer uses "affiliated entities" (sister companies) to perform functions. This prevents companies from "hiding" profits by overpaying their own subsidiaries for services.

3. How to Use the Report to Negotiate Your Rate

The Transparency Report isn't just a reading exercise—it's a shopping tool.

- Compare the Reinsurance Slice: If Carrier A’s report shows 40% of your rate goes to reinsurance but Carrier B’s shows 25%, Carrier A may be over-hedging or using an inefficient strategy.

- Verify Mitigation Impact: The 2026 report must show the specific dollar impact of your Wind Mitigation credits. If you added a new roof but the "credits" slice of the graph is tiny, your agent needs to investigate.

- Check for "Trade Secret" Flags: In 2026, statewide average requested rate changes are no longer trade secrets. You can now see if your specific renewal is significantly higher than the company's statewide average.

4. The New OIR Resource Center

As part of the 2026 Act, the state has launched a Comprehensive Resource Center. If your "Plain Language" report still feels like Greek, you can visit the OIR website to find:

- Market Trend Graphics: Real-time data on whether rates are rising or falling in your specific county.

- Financial Stability Ratings: A simplified look at the "financial conduct" of your insurance company.

Why Working with an Independent Agency is Vital

In 2026, transparency is great, but action is better. At Walker Insurance Agency, we take your "Plain Language" report and cross-reference it with the entire Florida market.

The Walker Advantage:

- Affiliate Audit: We check if your carrier is using "shell companies" to inflate your bill—a practice the 2026 Act finally brings to light.

- Land Value Deduction: we ensure your Coverage A doesn't accidentally include your Florida dirt, potentially saving you 10% to 15% on your premium immediately.

- Market Comparison: If your report shows your carrier’s profit margin is significantly higher than the 2026 average, we use that data to find you a more efficient competitor.

FAQ

1. When will I see the new Plain Language report? Insurers are required to include the report with all residential property offers and renewals issued on or after October 1, 2026.

2. What if my insurer doesn't provide the report? Failure to provide the report is a violation of the 2026 Transparency Act. Your agent can help you report this to the Division of Consumer Services for immediate action.

3. Does the report tell me if my company is going to go bankrupt? While it doesn't predict the future, it must disclose "major adverse findings" and their current financial condition, giving you much higher visibility into their stability.

4. Will this report make my insurance cheaper? Transparency itself doesn't lower rates, but it forces competition. When homeowners can see exactly how much profit a company is making, it pushes insurers to price more aggressively to keep your business.

See Your Savings Clearly in 2026

The era of the "confusing insurance bill" is over. With the 2026 Transparency Act, the power has shifted back to the Florida homeowner.

Audit your renewal today. Contact Walker Insurance Agency for a "Plain Language" deep dive. We provide the visibility you need to ensure every dollar of your premium is working to protect your home, not just pad a corporate bottom line.

[GET A FREE QUOTE TODAY] Call us at +1-407-977-7100 or visit our office in Stuart, FL. Let us help you see the truth in your insurance.

Related Articles

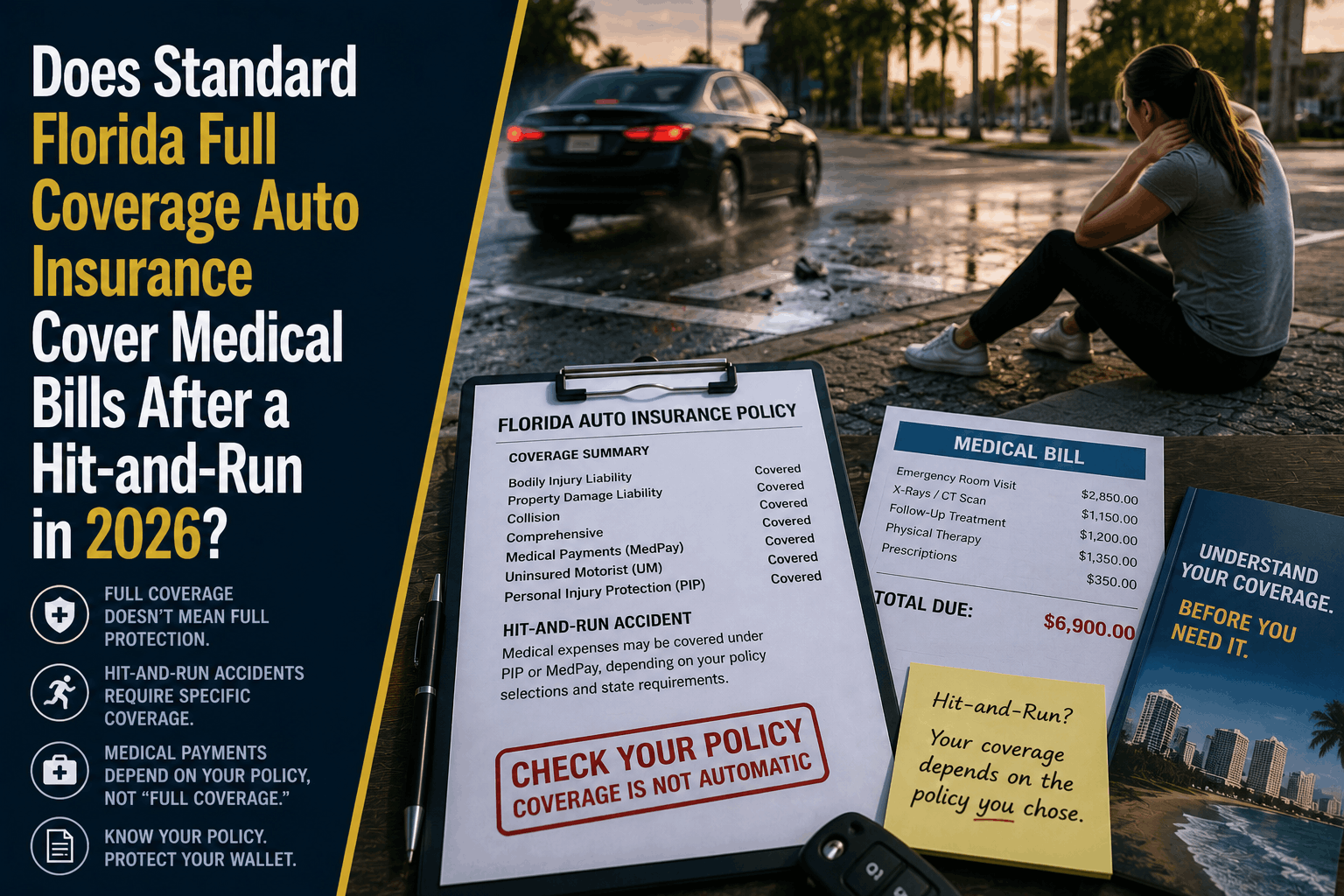

Does Florida Full Coverage Pay Medical Bills in a Hit-and-Run?

Relying on Florida "full coverage" auto insurance to pay your medical bills after a hit-and-run in 2026? Discover why it fails and leaves you broke.

Read More →

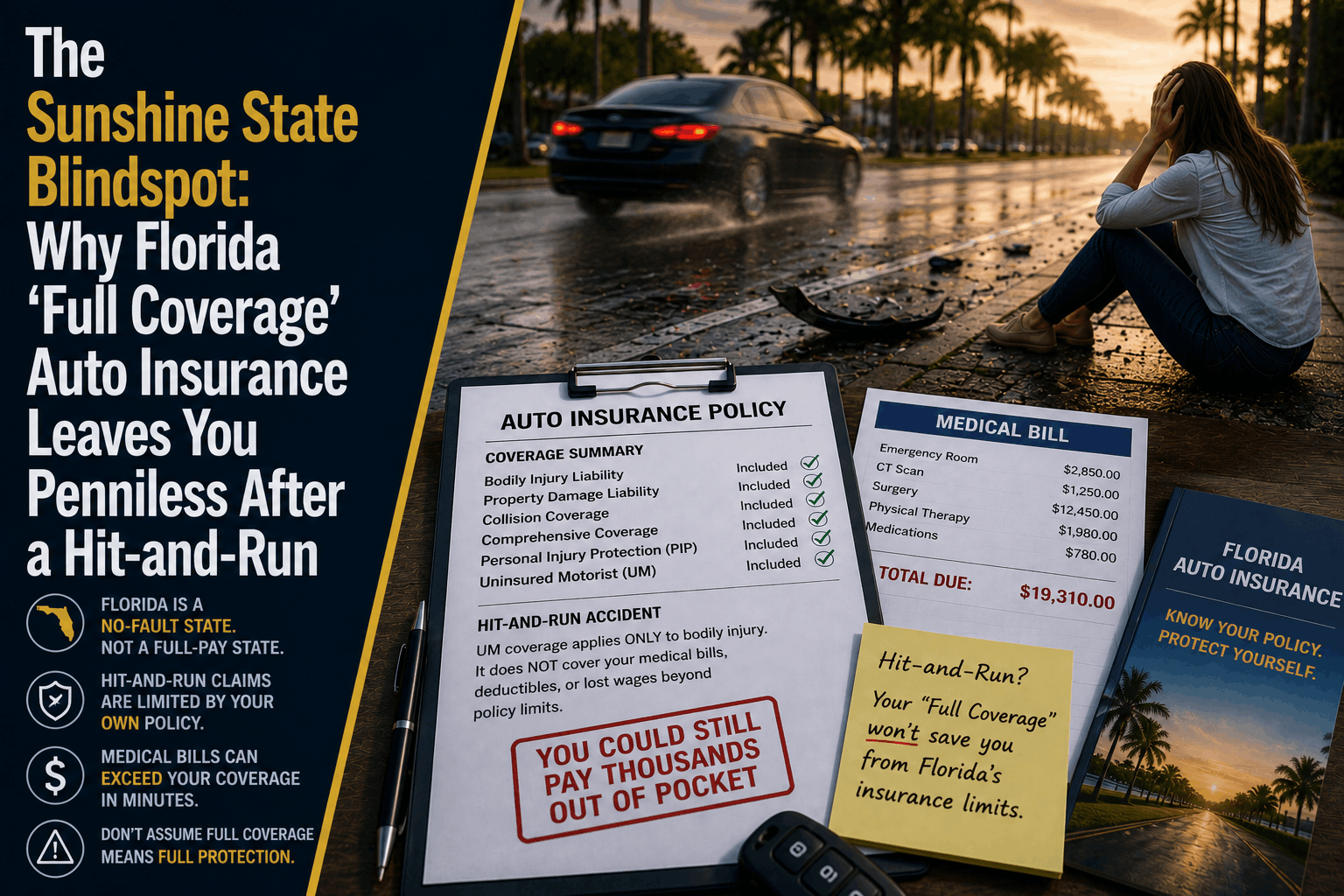

Why Florida Full Coverage Auto Insurance Fails in Hit-and-Runs

Think you're safe with Florida "full coverage" auto insurance? Discover the hidden blind spot that leaves hit-and-run victims broke and unprotected in 2026.

Read More →

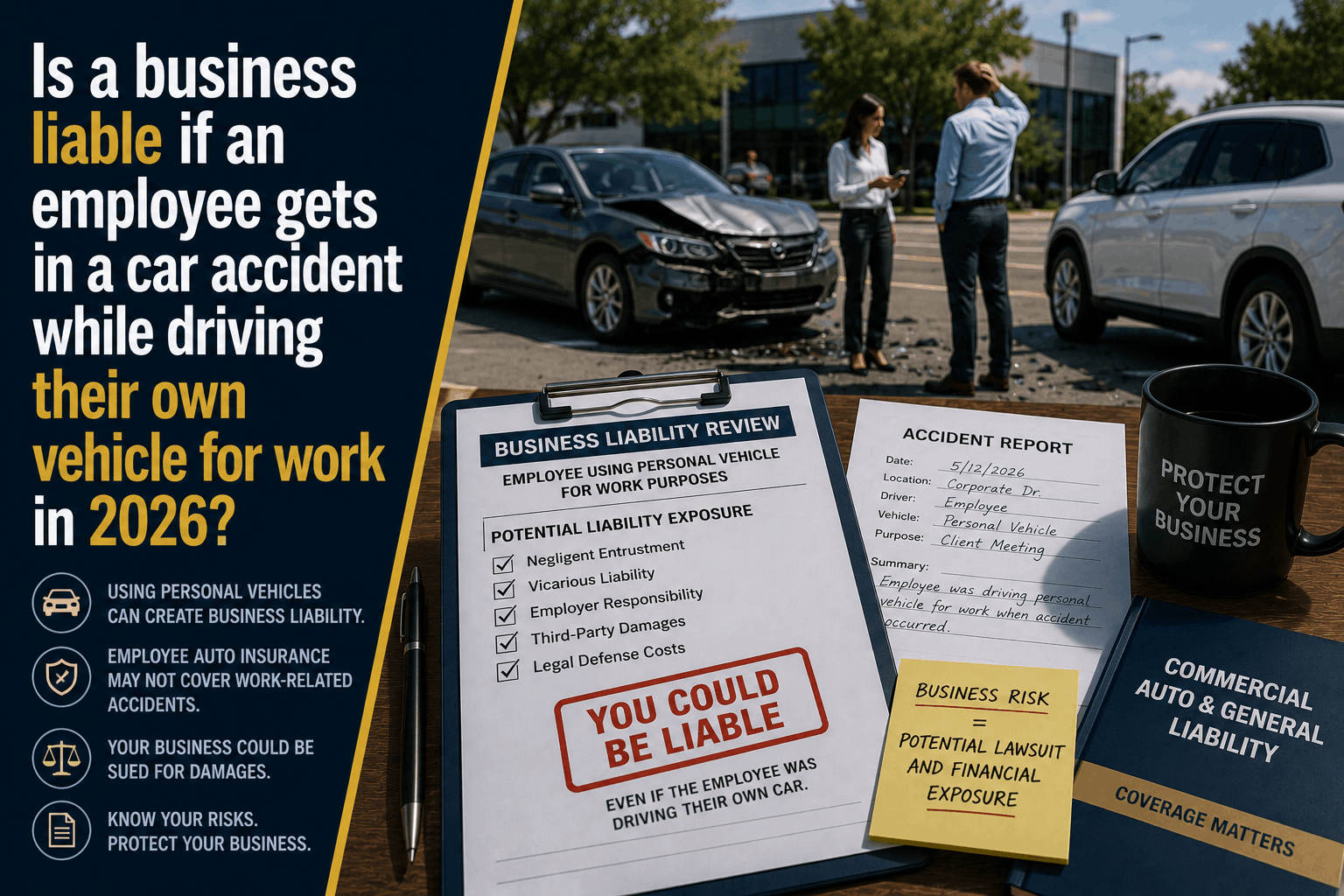

Is a Business Liable If an Employee Crashes a Personal Car for Work?

Discover your corporate liability if an employee causes a car accident while driving their own vehicle for work in 2026\. Learn about the HNOA loophole.

Read More →