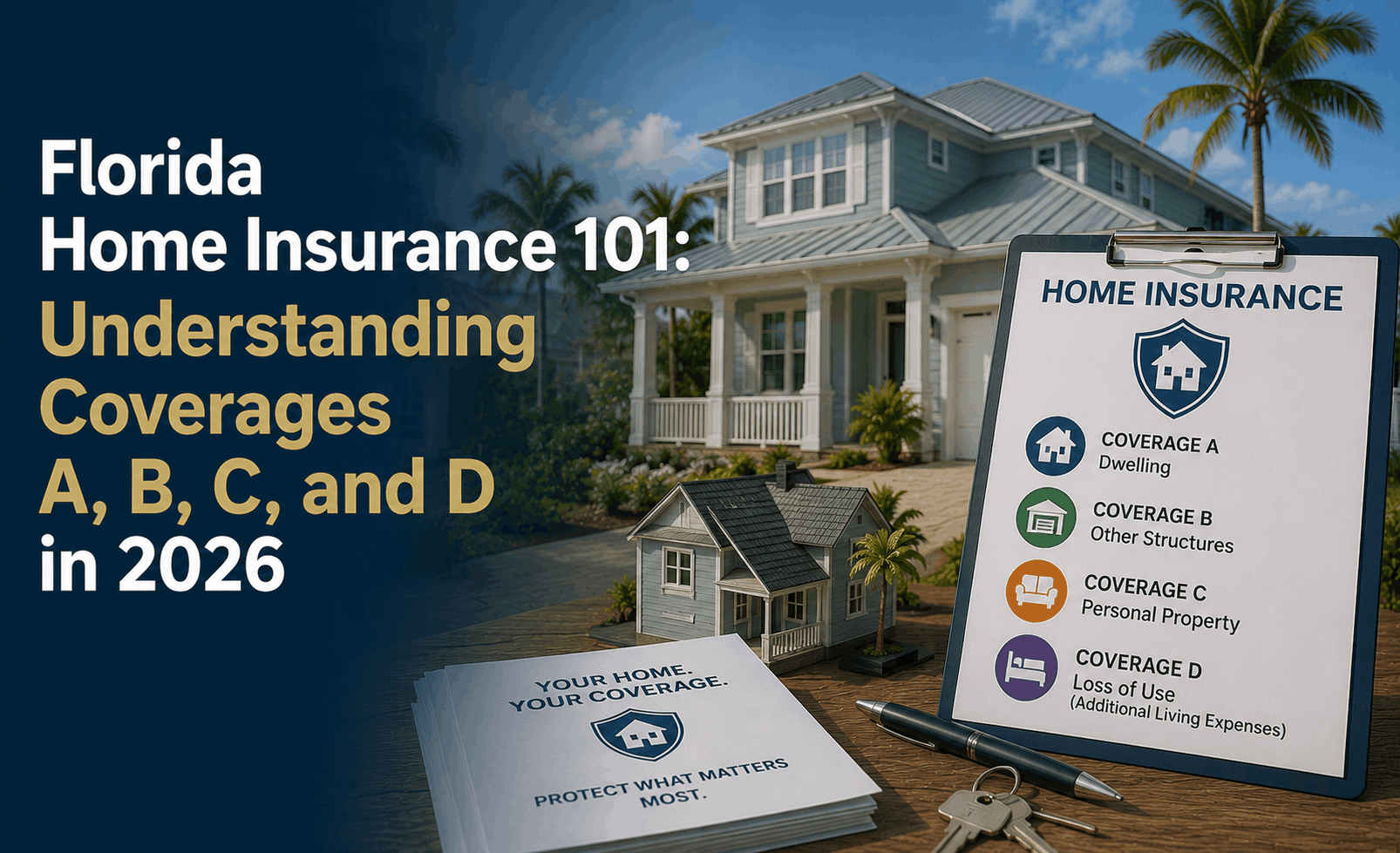

Florida Home Insurance 101: Understanding Coverages A, B, C, & D (2026)

Florida Home Insurance 101: Understanding Coverages A, B, C, and D in 2026

The Direct Answer: A standard Florida homeowners policy (HO-3) is divided into four primary sections: Coverage A (Dwelling) protects the main house; Coverage B (Other Structures) covers detached items like fences or sheds; Coverage C (Personal Property) replaces your belongings; and Coverage D (Loss of Use) pays for extra living expenses if you're displaced. In May 2026, Florida’s insurance market is stabilizing, with average premiums at $3,815, but new laws like HB 815 (protecting older roofs) and updated replacement costs ($150–$220/sq. ft.) mean you must adjust these limits to avoid being underinsured.

To achieve total visibility over your financial safety net, you must understand how these four buckets work together to protect your largest asset in 2026’s unique risk landscape.

Coverage A: Dwelling (The House Itself)

This is the most critical number on your policy. It covers the structure of your home, including attached garages and permanent fixtures like cabinets and flooring.

- 2026 Replacement Cost Reality: In 2026, Florida construction costs have leveled but remain high. Expect to insure your home for $150 to $180 per square foot for inland areas, and $180 to $220+ for coastal regions like Miami or Stuart.

- The "Gap" Alert: Coverage A is not based on your home's market value (what you could sell it for), but on what it costs to rebuild from scratch today.

- HB 815 Protection: Under new 2026 laws, insurers can no longer drop your Coverage A just because your roof is 15 years old if an inspection proves it is still functional.

Coverage B: Other Structures

This covers detached structures on your property.

- Standard Limit: Usually set at 10% of Coverage A. If your home is insured for $400k, you have $40k for other structures.

- What it covers: Fences, detached sheds, guest houses, gazebos, and even pool enclosures (screen porches).

- 2026 Wildfire Risk: With Florida facing a severe 2026 drought, detached structures near brush lines are at higher risk. Ensure your Coverage B limit actually reflects the cost of high-grade fencing and custom sheds.

Coverage C: Personal Property

This is for everything inside the house—your furniture, clothes, electronics, and appliances.

- Standard Limit: Typically 50% of Coverage A.

- Replacement Cost vs. ACV: In 2026, always choose Replacement Cost for Coverage C. If your 5-year-old TV is stolen, "Actual Cash Value" (ACV) only gives you its depreciated worth ($50), whereas Replacement Cost buys you a new equivalent TV.

- Special Limits: Standard policies cap payouts for jewelry, firearms, and art (often at $1,500–$2,500). If you have high-value items, you need a "Scheduled Personal Property" endorsement.

Coverage D: Loss of Use

If a hurricane or wildfire makes your home uninhabitable, Coverage D pays for the additional costs of living elsewhere.

- Standard Limit: Usually 20% of Coverage A.

- What it covers: Hotel bills, temporary rental homes, and even the increase in your grocery/dining bills while you don't have a kitchen.

- 2026 Rebuild Timelines: Because Florida labor shortages persist in 2026, rebuilds take longer. Ensure your Coverage D provides enough funds for at least 12 to 18 months of displacement.

Why Working with an Independent Agency is Vital in 2026

Florida's market is finally turning a corner, but "set it and forget it" is a recipe for disaster. At Walker Insurance Agency, we provide the visibility you need to navigate these four categories.

The Walker Advantage:

- 2026 Valuation Audit: We use real-time local construction data to ensure your Coverage A is accurate, preventing the "coinsurance penalty."

- Law & Ordinance Review: Per Florida Statute 627.7011, we ensure you have at least 25% to 50% in Law & Ordinance coverage to handle mandatory 2026 building code upgrades during a rebuild.

- Market Transparency: With 18 new carriers entering Florida in the last two years, we shop the entire market to find the best balance of A, B, C, and D for your specific zip code.

FAQ

1. Is flood insurance included in Coverages A or C? No. Standard Florida homeowners policies exclude flood damage. You must purchase a separate policy through the NFIP or a private 2026 flood insurer.

2. Does Coverage B cover my pool? In-ground pools are usually part of Coverage A (attached), while above-ground pools or detached pool houses fall under Coverage B. Always verify with your agent.

3. What is the "10% Rule" for Personal Property in 2026? Many policies limit Coverage C to 10% of the limit for items kept at a secondary residence or a storage unit.

4. Can I lower Coverage B to save money? If you don't have a fence or shed, some 2026 Florida carriers allow you to reduce Coverage B to 2% or 5% to lower your premium slightly.

Don’t Leave Your Home to Chance

Understanding the "Alphabet" of insurance is the first step toward true financial security. In 2026, a small error in your Coverage A or D can cost you tens of thousands of dollars out of pocket.

Get a Coverage Audit today. Contact Walker Insurance Agency for a 2026 Policy Review. We provide the visibility you need to ensure your home is protected from every angle in Stuart.

[GET A FREE QUOTE TODAY] Call us at +1-407-977-7100 or visit our office in Stuart, FL.

Related Articles

Does Florida Full Coverage Pay Medical Bills in a Hit-and-Run?

Relying on Florida "full coverage" auto insurance to pay your medical bills after a hit-and-run in 2026? Discover why it fails and leaves you broke.

Read More →

Why Florida Full Coverage Auto Insurance Fails in Hit-and-Runs

Think you're safe with Florida "full coverage" auto insurance? Discover the hidden blind spot that leaves hit-and-run victims broke and unprotected in 2026.

Read More →

Is a Business Liable If an Employee Crashes a Personal Car for Work?

Discover your corporate liability if an employee causes a car accident while driving their own vehicle for work in 2026\. Learn about the HNOA loophole.

Read More →