Florida Flood Insurance: Hurricane Season vs. Every Day (2026)

Hurricane Season vs. Every Day: Why You Need Flood Insurance in Florida

The Quick Answer: In Florida, flooding is a year-round threat that doesn't follow the hurricane calendar. While 2026 data shows that hurricanes like Helene and Milton caused massive storm surges, nearly 30% of all flood claims in Florida occur outside of high-risk zones and away from major storms. A standard homeowners policy never covers rising water. Whether it's a summer downpour, a broken water main, or a seasonal high tide, you need a separate flood insurance policy to protect your home 365 days a year.

To achieve total visibility over your property's safety, you must understand that "water damage" is not a single category in insurance. In the 2026 Florida market, the gap between wind and water coverage is the most common reason for financial disaster after a storm.

The "Flood Gap": Why Your Homeowners Policy Isn't Enough

The most dangerous misconception in Florida is believing that a "full coverage" homeowners policy includes flood protection.

The Strict Insurance Definition:

- Homeowners Insurance: Covers "falling water" (rain coming through a wind-damaged roof) and "internal water" (a burst pipe).

- Flood Insurance: Covers "rising water" (groundwater coming up, storm surge, or overflowing lakes/canals).

If water touches the ground before it enters your home, it is a flood. Without a separate policy from the NFIP or a private carrier, you are 100% responsible for the repairs, which average over $30,000 for just one inch of water.

Hurricane Season: The Surge Risk

During hurricane season (June 1 – Nov 30), the primary threat is storm surge. Even if your home is miles inland, powerful winds can push massive amounts of seawater into coastal tributaries, causing sudden and catastrophic flooding in areas that haven't flooded in decades.

**The 2026 Reality:**As of January 1, 2026, many Florida insurers—including Citizens—now require policyholders in certain zones to maintain flood insurance as a condition of their wind coverage. This ensures that when a hurricane hits, there is no "finger-pointing" between adjusters about whether the wind or the water caused the damage.

Every Day Risks: The 30% You Don't See Coming

You don't need a named storm to experience a total loss. In Florida, everyday flooding is driven by:

- Summer Thunderstorms: Tropical downpours can dump 5+ inches of rain in an hour, overwhelming local drainage systems and sending water into garages and living rooms.

- Rapid Urban Development: New construction in cities like Stuart and Orlando changes how the ground absorbs water, often pushing runoff into older neighborhoods that previously stayed dry.

- Tidal Flooding: "King Tides" can cause saltwater to back up through storm drains, flooding streets and homes even on a perfectly sunny day.

Comparing Your Options: NFIP vs. Private Flood Insurance

In 2026, Florida homeowners have more choices than ever. You no longer have to rely solely on the federal government for protection.

| Feature | NFIP (FEMA) | Private Flood Insurance |

|---|---|---|

| Building Limit | Max $250,000 | Up to $1 Million+ |

| Contents Limit | Max $100,000 | Customizable |

| Living Expenses | Not Covered | Often Covered |

| Waiting Period | 30 Days | 0 - 14 Days |

2026 Mandates: Do You Legally Need It?

The rules for Florida flood insurance have become stricter in 2026.

- Citizens Policyholders: If you have Citizens homeowners insurance, you are likely now required to have flood insurance, regardless of your flood zone.

- Mortgage Requirements: If you live in a Special Flood Hazard Area (SFHA) and have a federally backed mortgage, flood insurance is a legal requirement.

- High-Value Homes: As of 2026, homes with a replacement cost over $400,000 are under increased scrutiny to maintain flood protection to avoid "underinsurance" penalties.

Why Working with an Independent Agency is the Best Move

At Walker Insurance Agency, we provide the visibility needed to navigate Florida's complex water laws. We don't just sell you a policy; we analyze your specific elevation and "Daily Flood Risk" to find the best value.

The Walker Advantage:

- Instant Market Access: We compare the NFIP with top-rated private flood carriers in 2026 to find the lowest premiums.

- Waiting Period Guidance: We ensure your policy is active before the next tropical wave develops.

- Local Expertise: Based in Stuart, we understand the local water tables and drainage patterns of the Treasure Coast.

FAQ

1. Does my homeowners insurance cover storm surge? No. Storm surge is classified as rising water and is strictly excluded from standard homeowners and windstorm policies. You must have flood insurance to cover surge damage.

2. Why do I need flood insurance if I'm not in a "high-risk" zone? Nearly 30% of flood claims in Florida come from low-to-moderate risk zones (Zones X or B). In Florida, "low risk" does not mean "no risk."

3. Is there a waiting period for flood insurance? Yes. The NFIP typically has a 30-day waiting period. Private insurers may offer shorter periods, but you cannot buy a policy once a storm is already approaching.

4. How much does flood insurance cost in Florida in 2026? While rates vary, the average cost for an NFIP policy in Florida currently ranges from $760 to $865 per year, though homes in low-risk zones can often find private coverage for much less.

Local Business Schema

Don’t Wait for the Water to Rise

In Florida, it’s not a matter of if it will rain, but where the water will go. Don’t let a single summer storm or an unpredicted surge erase your home equity.

Secure your home today. Contact Walker Insurance Agency for a comprehensive flood risk assessment. We provide the visibility you need to choose the best protection at the lowest possible rate in Stuart.

[GET A FREE QUOTE TODAY] Call us at +1-407-977-7100 or visit our office in Stuart, FL. Let us help you keep your head above water.

Related Articles

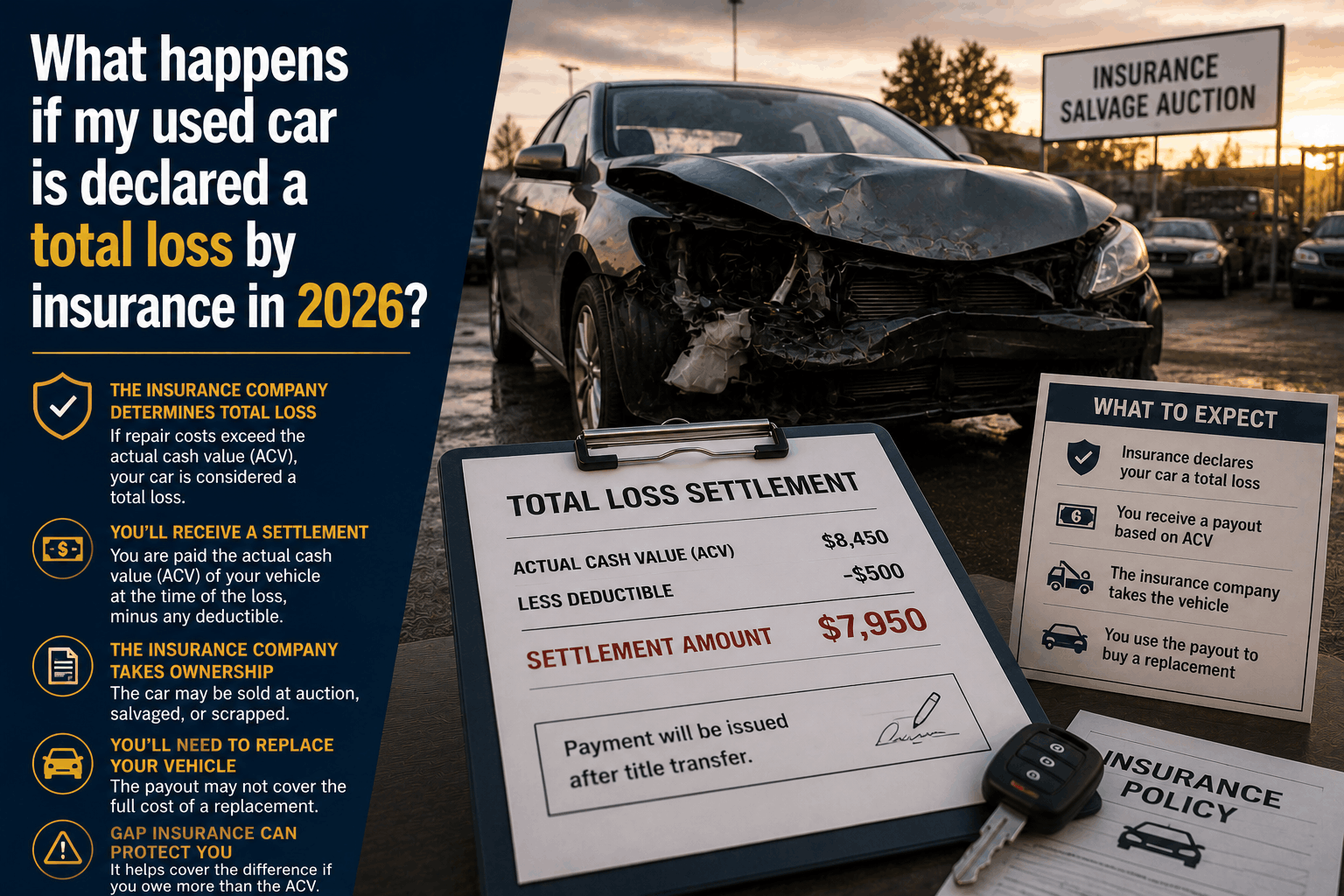

What Happens If Your Used Car Is Totaled by Insurance in 2026?

Navigating a totaled used car claim? Discover the step-by-step insurance process, how Actual Cash Value (ACV) is calculated, and how to dispute a low valuation.

Read More →

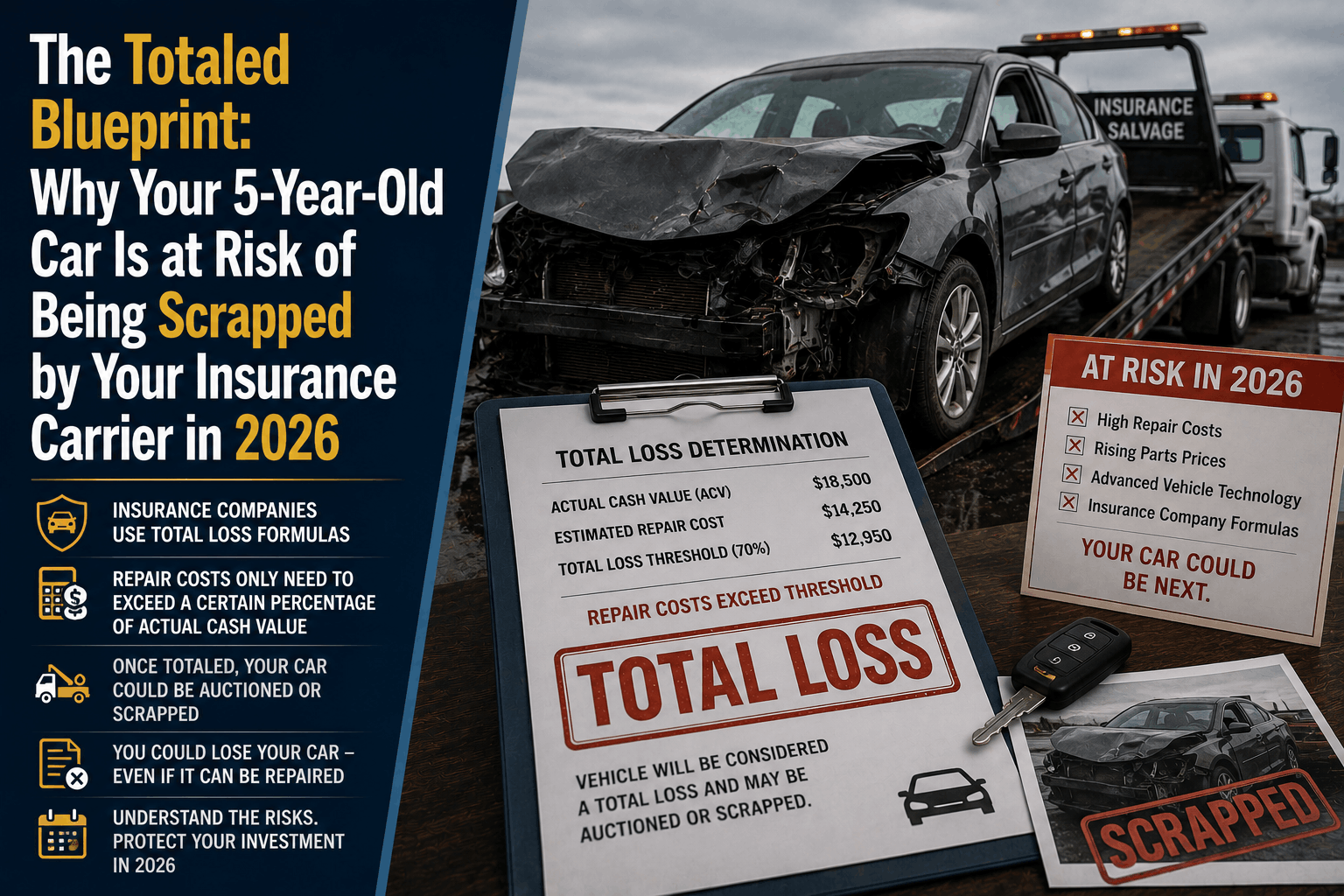

The Totaled Blueprint: Why Insurers Are Scrapping 5-Year-Old Cars in 2026

Discover why insurance companies are declaring 5-year-old cars a total loss in 2026\. Learn how ADAS technology and high salvage values trigger the "Totaled Blueprint."

Read More →

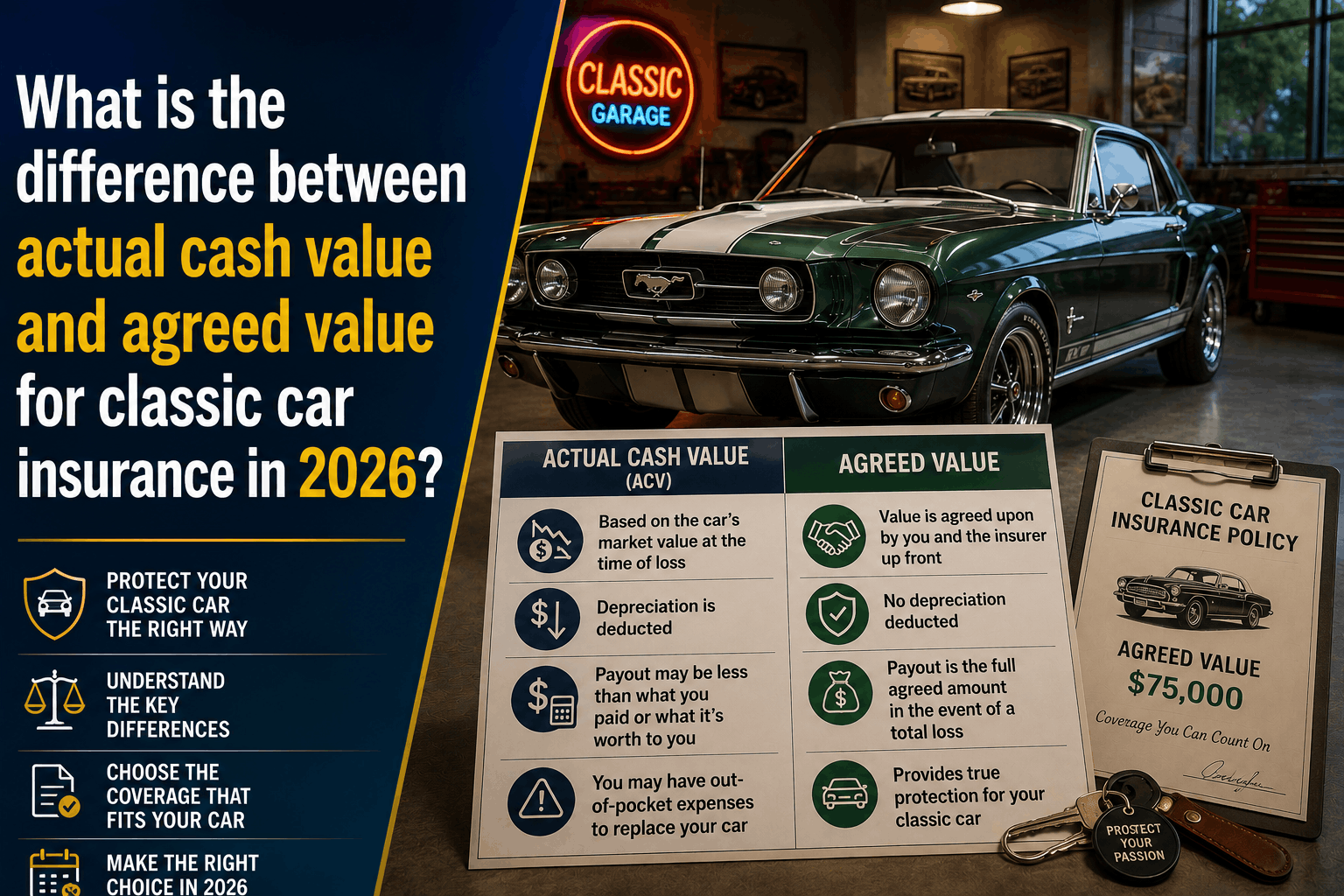

ACV vs. Agreed Value: Classic Car Insurance Guide (2026)

What is the difference between Actual Cash Value and Agreed Value for classic cars? Discover why 2026 market trends make traditional policies highly risky.

Read More →