Does Florida Home Insurance Pay Guest Medical Bills? (2026)

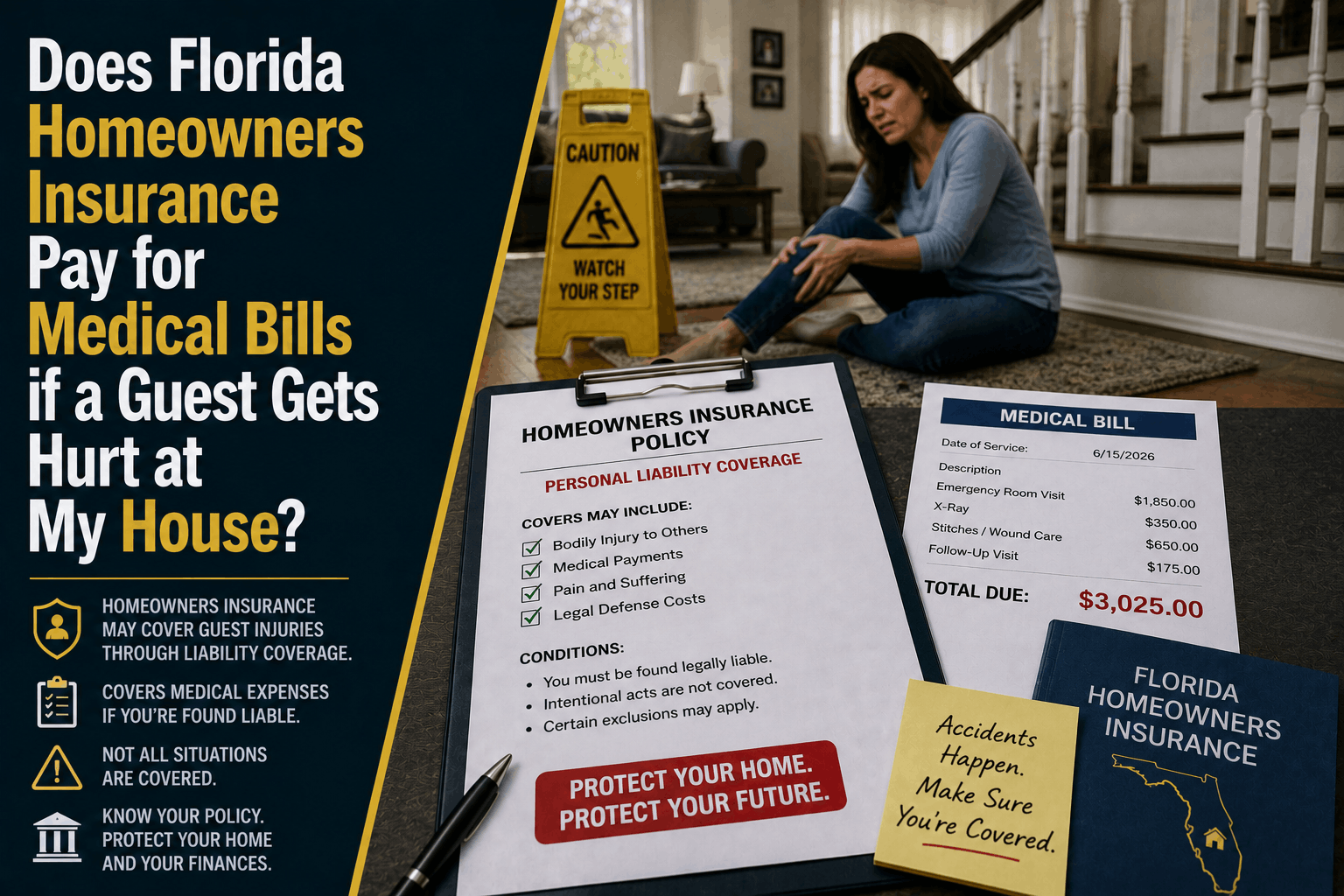

Does Florida Homeowners Insurance Pay for Medical Bills if a Guest Gets Hurt at My House?

The Direct Answer

Yes, but only up to a dangerously low, pre-set financial limit. In 2026, standard Florida homeowners insurance includes a specific component known as Coverage F (Medical Payments to Others) designed to handle a visitor's medical bills on a "no-fault" basis. This means if a guest trips on your rug or slips on your patio, the policy pays for their immediate treatment without requiring them to sue you or prove you were negligent. However, the critical catch in today's tight Florida insurance market is that standard Coverage F limits are default-capped at a baseline of just $1,000 to $5,000. With modern healthcare overhead, a single ambulance ride or emergency room evaluation in Martin County will completely wipe out that cap. Once that tiny threshold is shattered, your policy will pay nothing further unless your guest takes legal action against you to trigger your separate Coverage E (Personal Liability) protection, exposing you to severe out-of-pocket gaps.

For Stuart families who regularly host weekend gatherings, pool days, or family barbecues, this hidden ceiling represents a massive administrative blind spot. Private property carriers operating in Florida utilize these strict low limits to quickly cap their financial risk, shifting the escalating burden of local medical inflation straight back onto the property owner's personal savings.

1. The Multi-Tiered Reality of Guest Injury Expenses

When a casual accident occurs on your property, your home insurance doesn't write an open-ended check to the hospital. Instead, the claim is immediately split into two entirely separate legal structures, each carrying strict limitations:

- Phase 1: Coverage F (Medical Payments): This acts as immediate, no-fault "goodwill" coverage. It handles base emergency costs smoothly, but it is explicitly designed only for minor, low-cost incidents.

- Phase 2: Coverage E (Personal Liability): This features much higher limits (typically starting at $300,000), but it completely freezes until your guest formally alleges or proves that your physical property negligence—such as a rotten stair or a broken walkway—directly caused their injury.

The out-of-pocket trajectory of a typical backyard accident quickly bypasses standard baseline protections:

- Minor Sprains and Localized Stitches: If a friend trips on an uneven patio stone and requires simple stitches or diagnostic X-rays at a local urgent care clinic, the final bill generally ranges from $1,200 to $2,500. This minor incident cleanly fits within a standard $5,000 Coverage F limit, allowing you to settle the medical debt quickly and preserve personal relationships without corporate friction.

- Moderate Fractures and Ambulance Transport: If a visitor slips on a wet pool deck, resulting in a severe fracture that requires emergency EMT transport and an ER evaluation, local medical overhead instantly escalates to $8,000 to $15,000. Because this event completely shatters your $5,000 no-fault cap, your insurer stops paying. To recover the remaining balance, your guest's private health insurance provider may legally pressure them to file a formal liability claim against you to unlock your policy's liability limits.

- Catastrophic Fractures or Concussions: For serious joint dislocations, deep concussions, or ligament tears requiring specialized surgical intervention and months of physical rehab, medical bills routinely climb to $45,000 to $90,000. If your carrier uncovers a common backyard exclusion in your policy booklet, they can deny the personal liability claim entirely, leaving your home and personal investments completely exposed to a direct civil lawsuit.

The Structural Exclusion List: To manage high-risk exposures, typical 2026 Florida policy forms features strict exclusions. Bodily injury claims resulting from "high-risk trampoline use," "un-permitted swimming pool diving boards," or "un-notified temporary inflatable rentals" like party bounce houses are frequently barred from both medical payments and liability protections.

2. Navigating Florida's Strict Liability Constraints

Protecting your hard-earned wealth requires understanding how specific Florida statutes alter your risk profile the moment a guest crosses your property line. Two major factors dominate medical liability across our coastal region today:

The Strict Dog Bite Liability Framework (Fla. Stat. § 767.04)

Florida operates under a strict statutory framework for domestic animal behavior. Under state law, you are held automatically liable if your dog bites or injures a guest lawfully on your premises, regardless of whether your pet has ever shown a single aggressive tendency in the past. However, a significant gap exists between your statutory legal liability and your insurance policy text. The vast majority of private carriers in the state now attach complete Animal Liability Exclusions or rigid breed blacklists to standard forms. If your pet knocks over an elderly guest or bites a visitor, your policy will frequently refuse to pay a single dollar of their medical bills or your legal defense.

The Commercial Worker Boundary

Property owners frequently assume that if a local landscaper, independent pool technician, or cleaning professional is injured while working on their home lot, the residential policy will step in to pay the medical costs. It will not. Standard residential forms explicitly exclude any bodily injury claims for individuals who are on the premises to perform a commercial service, business pursuit, or are eligible for statutory workers' compensation benefits. If a hired contractor lacks their own corporate coverage, they can pursue your personal assets directly for workplace injuries sustained on your roof or in your yard.

3. How to Secure Your Personal Assets Against Backyard Risks

If your home and social lifestyle are currently resting on an un-audited property contract, your financial stability is completely unprotected from a casual mistake. At Walker Insurance Agency, we advise Stuart property owners to insulate their portfolios using a clear, three-step defensive layout:

- Step 1: Endorse Coverage F to the Absolute Maximum Ceiling. Request your independent agent to manually scale your standard no-fault medical payments limit from the basic $1,000 mark up to $5,000 or $10,000. This minor contract adjustment costs pennies a year in premium but completely handles small guest accidents cleanly before they can escalate into complex legal disputes.

- Step 2: Dissect and Buy Back Animal Liability Endorsements. Thoroughly review your policy rider jackets for dog or animal exclusions. If your current provider enforces an absolute animal exclusion, work with a broker to bind a specialized animal liability rider or shift your primary property line to a carrier that offers robust pet protections.

- Step 3: Deploy an Isolated Personal Umbrella Shield. For complete financial security, isolate your household wealth under a separate $1 Million or $2 Million Personal Umbrella Policy. This high-limit liability shield sits cleanly above your home and auto lines, stepping in to absorb massive medical judgements, costly legal defense fees, and catastrophic injury claims that easily blow past standard baseline limits.

Why Working with an Independent Agency is Vital

Attempting to manage complex personal liability exposures through a generic smartphone app or an automated corporate online form ensures you will miss the fine-print exclusions that cause devastating claims denials. At Walker Insurance Agency, we provide the personalized, data-driven visibility you need to defend your property line.

The Walker Advantage:

- Exclusion Text Analysis: We thoroughly analyze your carrier’s underlying endorsement forms to expose hidden restrictions regarding pools, trampolines, pet breeds, and recreational equipment before an accident occurs.

- Medical Volume Scaling: We align your personal liability limits with the actual reality of active South Florida medical overhead, ensuring you are never left underinsured after an unexpected event.

- Carrier Market Access: As the stabilizing Florida market introduces 20 brand-new private insurance companies to the state, we continuously shop your profile to locate providers that offer robust guest protections at competitive premium floors.

FAQ

1. Does my medical payments coverage pay for injuries to my own family members living in the house?

No. Personal liability and medical payments to others (Coverage F) are strictly third-party protections. They are contractually written to cover guests, visitors, and individuals who do not permanently reside inside your household. Any injuries sustained by you, your spouse, or your dependent children must be filed through your private medical health insurance policy, never your homeowners property contract.

2. If a guest is injured after leaving my home, can I still be held liable for their medical bills?

Yes, potentially. Under Florida’s complex social host liability concepts, if you provide alcohol or host a gathering that directly contributes to an off-premises incident, you can face significant legal challenges. While your home insurance personal liability line may provide legal defense, standard exclusions regarding commercial activities or illegal alcohol distribution to minors can instantly invalidate your coverage.

3. Will my insurance company pay my legal defense fees if a guest sues me for an accident?

Only if the cause of the injury is a fully covered peril under your policy. If a guest sues you for a slip and fall caused by a rotten deck stair, your carrier is contractually obligated to provide and fund your legal defense team. However, if the lawsuit stems from an excluded item—such as an un-notified bounce house or an excluded dog breed—the carrier will issue an immediate denial, leaving you to pay local defense attorneys hundreds of dollars an hour out of pocket.

Insulate Your Personal Wealth Before the Weekend Begins

Your backyard is a place for relaxation and family memories, but leaving your personal asset protection to a basic, un-vetted insurance rider is an administrative gamble that can instantly compromise your family's budget. True peace of mind requires pulling back the curtain on your policy’s exclusions and ensuring your written contract matches the physical reality of your lifestyle.

Take control of your liability protection today. Contact Walker Insurance Agency for a comprehensive portfolio evaluation. We provide the visibility you need to eliminate hidden liability loopholes, deploy high-limit comprehensive asset shields, and protect your family's hard-earned wealth safely in Stuart.

[GET A FREE QUOTE TODAY]

Call our personal lines division at +1-407-977-7100 or visit our office in Stuart, FL. Let us safeguard your property boundaries today.

Related Articles

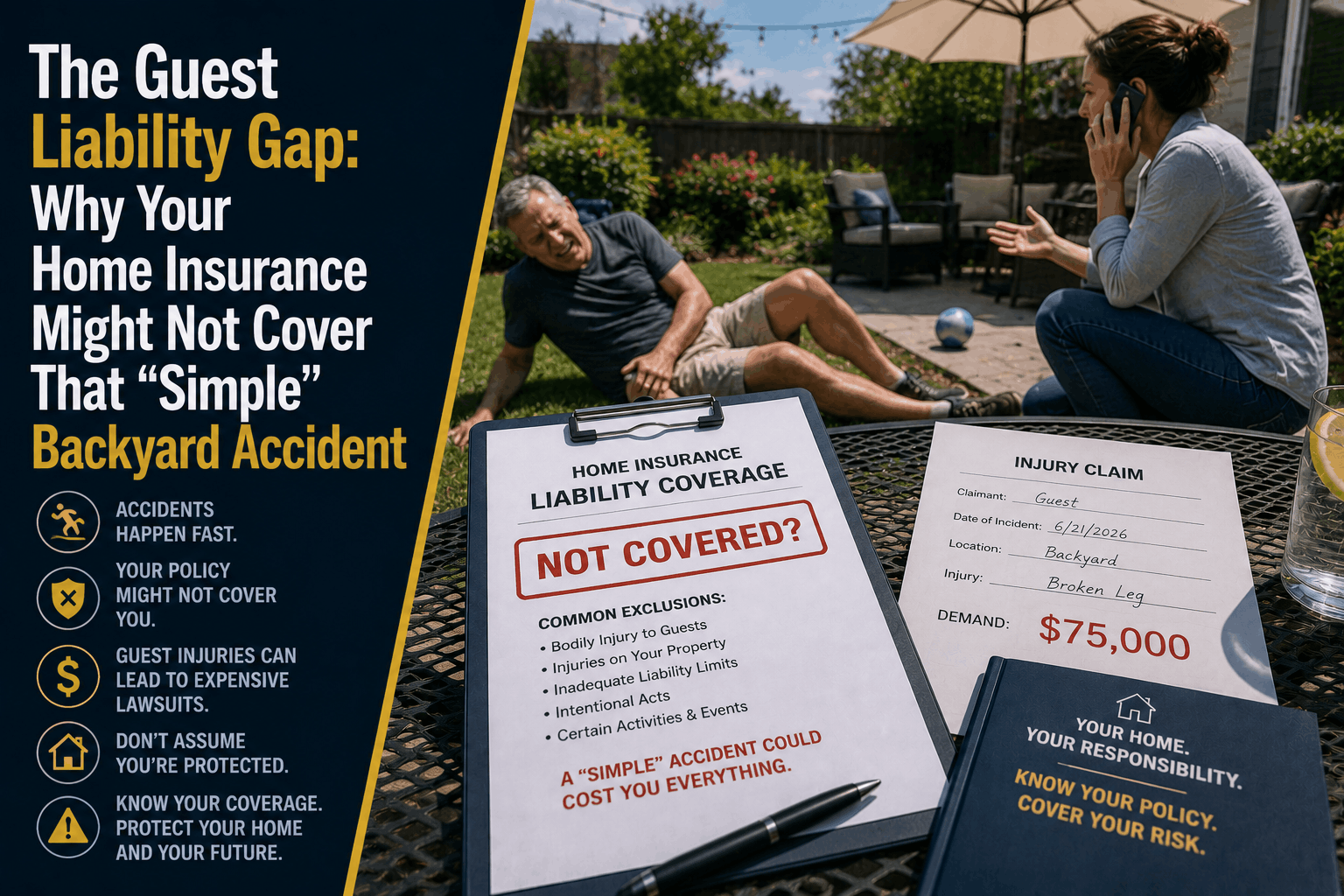

The Guest Liability Gap: Why Home Insurance Fails in 2026

Think your Florida "full coverage" home insurance protects you when friends gather in the backyard? Discover the hidden guest liability loopholes leaving Stuart families exposed.

Read More →

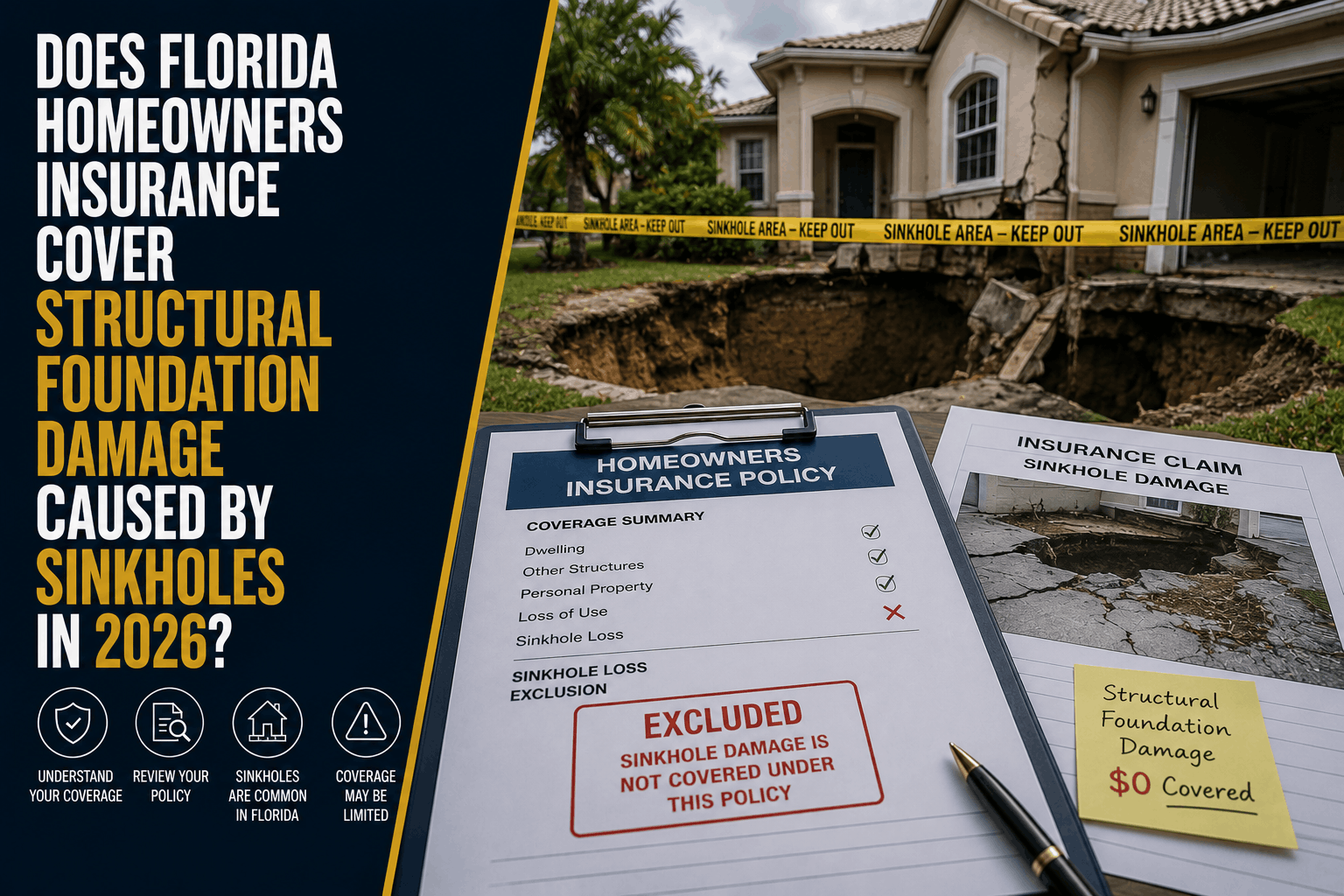

Does Florida Home Insurance Cover Sinkhole Foundation Damage? (2026)

Think your Florida home insurance handles sinkhole foundation damage? Discover the hidden legal gaps leaving Stuart property owners exposed this storm season.

Read More →

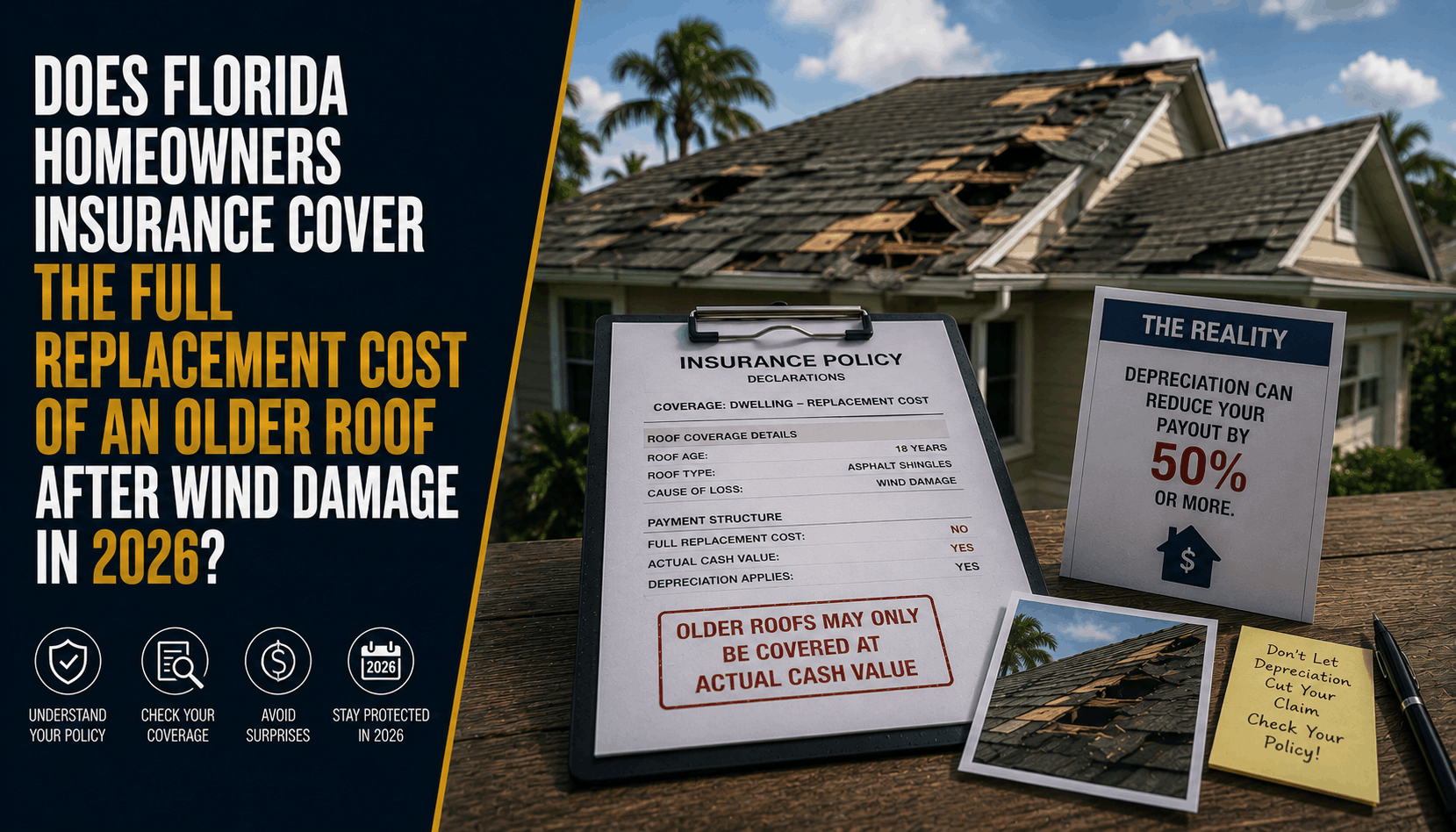

Does Florida Home Insurance Cover Roof Replacement Cost in 2026?

Think your Florida home insurance covers 100% of a new roof after wind damage? Learn how new 2026 guidelines leave Stuart homeowners paying out of pocket.

Read More →