Coverage A vs. Coverage C: Florida Home Insurance Explained (2026)

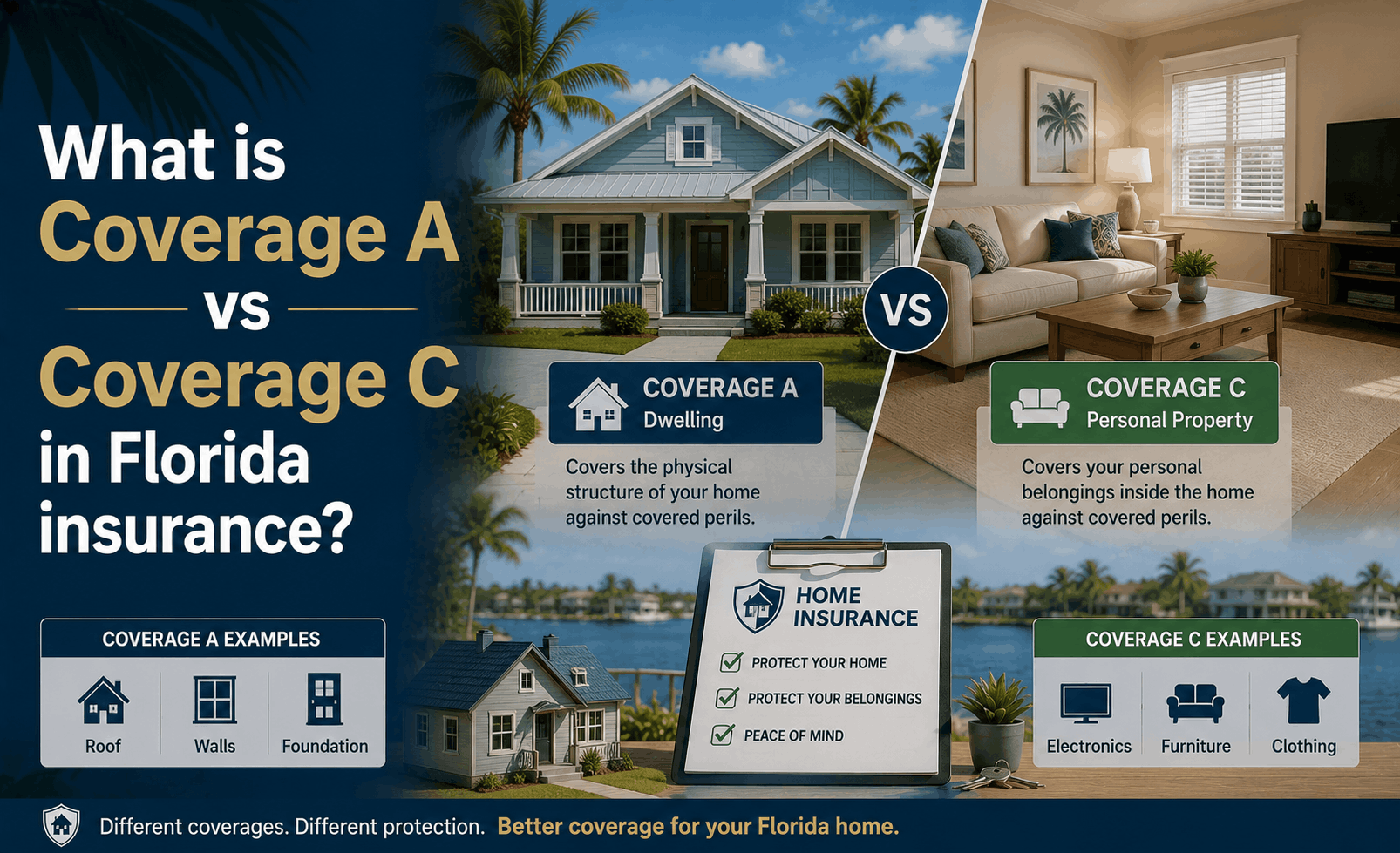

What is Coverage A vs. Coverage C in Florida Insurance?

The Direct Answer: In Florida, Coverage A (Dwelling) protects the physical structure of your home (walls, roof, foundation), while Coverage C (Personal Property) protects the contents inside (furniture, clothes, electronics). In 2026, Florida insurers typically set Coverage C at a default of 50% to 70% of your Coverage A limit. However, with the current 2026 rebuild costs averaging $180 to $250 per square foot due to specialized labor shortages, getting your Coverage A "Dwelling" number wrong will automatically leave you underinsured for your "Personal Property" as well.

To achieve total visibility over your financial protection, you must understand that while Coverage A is based on construction math, Coverage C is based on your lifestyle inventory. In 2026, the gap between the two is where most Florida homeowners lose money during a claim.

1. Coverage A: The Shell (Dwelling)

Coverage A is the "anchor" of your policy. It covers the house itself and any structure attached to it, like a garage or a screened-in porch.

- Basis for Limit: In 2026, this is strictly based on Replacement Cost Value (RCV)—what it costs to build your exact home from scratch today. It has nothing to do with market value or what you paid for the house.

- 2026 Florida Factor: Following the 2025-2026 legislative reforms, insurers are using more aggressive aerial imaging to verify the "health" of your structure. If your Coverage A is too low, you may face a coinsurance penalty, meaning the insurer only pays a percentage of your claim.

- What it Covers: The roof, flooring, built-in appliances, water heaters, and the foundation.

2. Coverage C: The Stuff (Personal Property)

Coverage C follows you. It covers your belongings whether they are inside your home, in your car, or with you while traveling in Europe.

- Basis for Limit: Usually calculated as a percentage of Coverage A. If your home is insured for $500,000 (A), your belongings are typically covered for $250,000 (C).

- Replacement Cost vs. ACV: Crucial for 2026: Ensure your Coverage C is set to Replacement Cost. Without this endorsement, a claim for a stolen 5-year-old laptop will only pay "Actual Cash Value" (pennies on the dollar) rather than what it costs to buy a new one today.

- Special Limits (Sub-limits): Standard Coverage C has "caps" on high-value items. In 2026, most policies limit jewelry to $1,500 and firearms to $2,500. For anything more, you need a "Scheduled Personal Property" floater.

3. Side-by-Side: The "Inside-Out" Rule

A simple way to remember the difference is the "Dollhouse Test": If you took your house, removed the roof, and turned it upside down, everything that stays attached is Coverage A. Everything that falls out is Coverage C.

| Feature | Coverage A (Dwelling) | Coverage C (Personal Property) |

|---|---|---|

| Primary Focus | The structure & fixtures | Your movable belongings |

| Calculation | Local construction costs/sq. ft. | % of Coverage A (usually 50-70%) |

| Deductible | Subject to AOP or Hurricane | Subject to AOP (All Other Perils) |

| Off-Premises | Only covers the home site | Covers your items worldwide |

4. Why the Ratio Matters in 2026

In 2026, many Florida homeowners are finding that the "default" 50% for Coverage C is actually too much insurance for their needs, or dangerously too little if they have upgraded to high-end smart home furniture or designer collections.

- The TARGET Strategy: At Walker Insurance Agency, we recommend a "Room-by-Room" video inventory. In 2026, AI-powered inventory apps can scan your video and give you a precise Coverage C number in minutes.

- The Inflation Gap: If you increase your Coverage A to match the 2026 construction spike, your Coverage C will rise automatically. We help you "dial back" that percentage if you don't need the extra contents coverage, which can save you 5% to 8% on your annual premium.

Why Working with an Independent Agency is Vital

Understanding the "A vs. C" dynamic is the difference between a check that covers your loss and a check that only covers your frustration. At Walker Insurance Agency, we provide the visibility you need to ensure these numbers work for you.

The Walker Advantage:

- Local Cost Benchmarking: We use Stuart-specific 2026 building data to set your Coverage A accurately.

- Scheduled Property Audit: We identify "hidden" sub-limits in your Coverage C that could leave your valuables exposed.

- Policy Bundling: We look for carriers that offer "enhanced" Coverage C packages, often including identity theft and refrigerator spoilage as a bonus in 2026.

FAQ

1. Does Coverage A cover my detached shed or fence?

No. Detached structures fall under Coverage B. Coverage A is only for the main house and anything physically attached to it.

2. Is my high-end kitchen island Coverage A or C?

Since it is a permanent fixture attached to the floor and plumbing, it is Coverage A. Your standalone air fryer sitting on top of it is Coverage C.

3. Does Coverage C cover my car?

No. Motor vehicles are specifically excluded from Coverage C. You need an Auto Insurance policy for that.

4. What happens if I have $10,000 in jewelry but only $1,500 in Coverage C sub-limits?

In the event of a theft, the insurance company will only pay you $1,500. To protect the full $10,000, you must "schedule" the jewelry separately on your policy.

Don't Guess Your Home's Value

In the 2026 Florida market, being "mostly" insured is the same as being uninsured for the remainder. One error in your A vs. C ratio can lead to thousands in out-of-pocket costs.

Get a Coverage Audit today. Contact Walker Insurance Agency for a 2026 Policy Review. We provide the visibility you need to ensure your home and your "stuff" are protected at the mathematically fair price in Stuart.

[GET A FREE QUOTE TODAY]

Call us at +1-407-977-7100 or visit our office in Stuart, FL. Let us help you protect your peace of mind.

Related Articles

Does Florida Full Coverage Pay Medical Bills in a Hit-and-Run?

Relying on Florida "full coverage" auto insurance to pay your medical bills after a hit-and-run in 2026? Discover why it fails and leaves you broke.

Read More →

Why Florida Full Coverage Auto Insurance Fails in Hit-and-Runs

Think you're safe with Florida "full coverage" auto insurance? Discover the hidden blind spot that leaves hit-and-run victims broke and unprotected in 2026.

Read More →

Is a Business Liable If an Employee Crashes a Personal Car for Work?

Discover your corporate liability if an employee causes a car accident while driving their own vehicle for work in 2026\. Learn about the HNOA loophole.

Read More →